We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Remortgage or debt consolidation?

Comments

-

We are in a similar position albeit about half your debt and a smaller mortgage (similar value house). We have the same income as you too.

Our debt is from renovations too although I also accept some must be from overspending too.

Our outgoings are less because we know we need to pay this debt off. I haven’t had a cleaner since we did the house because we can’t afford it.

You need to have a lightbulb moment before this can get better. You are in a risky position and I struggle to see how a £600k mortgage is a good idea on your salary and outgoings.When did the debt last increase? When did you finish the build?4 -

I suppose my main question is why do you need to consolidate? Once you’ve paid off AMEX your SOA balances and with most of the debt at 0%, your monthly payments will quickly be bringing the total down.

2 -

No one can tell you what to do.

I'll just say that I once remortgaged, and a few years later took on a secured 2nd loan from Shawbrook - all the while riding the wave of increasing house prices. Each time it bought me a few years of reduced constraints on my finances. But it didn't solve the underlying problem - and in the end I learnt the hard way with payday loans (each one renewed every month).

I'll also say that you are highly exposed to financial misfortune if one income drops for health or redundancy reasons.

All that said, you must take your own path. You may get away with the risk of income drop, or you may end up in the same situation as I was.Leap Day 2024 - the day of freedom. The day my pernicious debts finally died.

Legacy Default dates :

Mr Lender - 31/10/2022

Fund Ourselves - 22/12/2022

Bamboo - 30/3/2023

Likely Loans - 14/4/20233 -

Hi there.Another way of looking at things. If you add 35% to all your non essential expenditure (cleaner, hair, presents, holiday etc) it will be the same as what it is costing you not to use that money to pay back the Amex.That cleaner now becomes £199 a month.1

-

OP have you honestly thought this through in terms of what it will cost you?DonFog said:

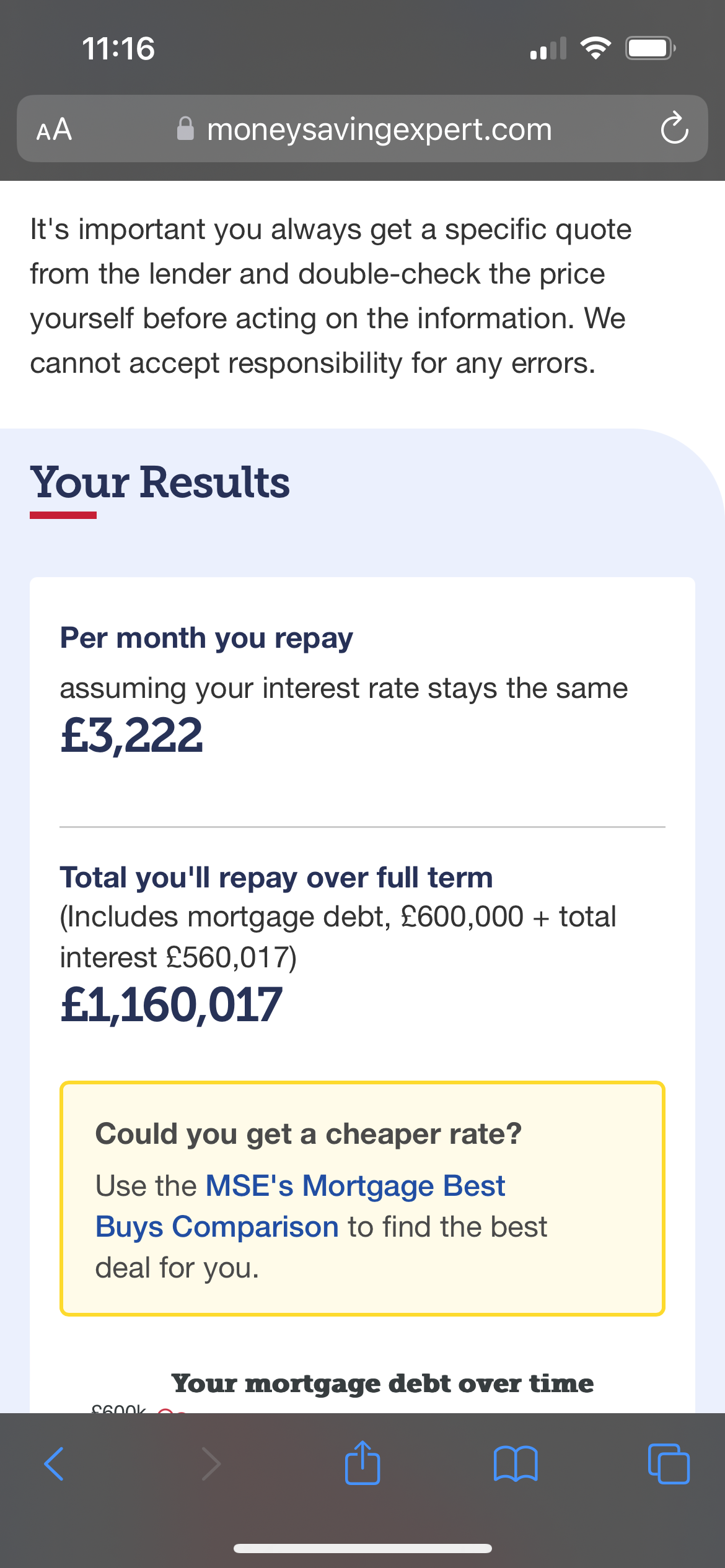

Our income is £151,000 and we want to borrow £600k on a £735,000 house.Veteransaver said:Your current mortgage is at a lowish interest rate and is still 5x your take home. You are talking about making that 6x your income and remortgaging at a far higher interest rate.This is the cost on a 5% mortgage over 30 years

Also if something happens; sickness etc you risk losing your home!

There’s no way your debts will cost you £500k if you cut back and pay them off as soon as you can, There’s definitely room in your budget to do this MFW 2026 #5007/03/25: Mortgage: £67,000.00

MFW 2026 #5007/03/25: Mortgage: £67,000.00

Mortgage:

04/04/26: £33,500

07/03/26: £34,418.15

16/01/26: £56,794.25

02/01/26: £60,223.17

12/08/25: Mortgage: £62,500.00

12/06/25: Mortgage: £65,000.00

18/01/25: Mortgage: £68,500.14

27/12/24: Mortgage: £69,278.38

Savings: £20,0003 -

Alternatively (and this helped me focus to paying off my mortgage), general rule of thumb is that over a 25 year term the amount you actually pay back on a mortgage is around double.Somerset50 said:Hi there.Another way of looking at things. If you add 35% to all your non essential expenditure (cleaner, hair, presents, holiday etc) it will be the same as what it is costing you not to use that money to pay back the Amex.That cleaner now becomes £199 a month.

So every £100 wasted on something now Vs paying it off the mortgage, actually costs you £200.

I found that quite sobering, as suddenly that must have £100 bargain doesn't look such a bargain at £200.

That flash £50k car doesn't look worth it at £100k etc.1 -

Just a word of warning. We have friends with 3 young children, similar income to you. Life all mapped out, skiing holiday next week all booked.

2 weeks ago their youngest daughter was rushed to Alderhay Hospital with a brain tumour. It was operated on but not all could be removed. It is very aggressive and she is to start 9 months of chemo.

Mum has given up her job and Dad has reduced his hours so obviously income has dropped for the foreseeable future.

4 weeks ago their life was completely normal. Now it has changed beyond belief.

Unfortunately life happens and not always how we expect it to.

The last thing anyone would want when faced with this is relentless worrying about how the mortgage will be paid on top of everything else.

A cautionary tale.

2 -

Those who are high earners tend to borrow in equal measure, or more than equal measure in a lot of cases.amanda_p said:Just a word of warning. We have friends with 3 young children, similar income to you. Life all mapped out, skiing holiday next week all booked.

2 weeks ago their youngest daughter was rushed to Alderhay Hospital with a brain tumour. It was operated on but not all could be removed. It is very aggressive and she is to start 9 months of chemo.

Mum has given up her job and Dad has reduced his hours so obviously income has dropped for the foreseeable future.

4 weeks ago their life was completely normal. Now it has changed beyond belief.

Unfortunately life happens and not always how we expect it to.

The last thing anyone would want when faced with this is relentless worrying about how the mortgage will be paid on top of everything else.

A cautionary tale.

They also tend to be asset rich, yet cash poor, as everything is sustained by credit or borrowing of some kind, a lot of those in the 40% plus tax bracket behave in this way.

It`s certainly not up to me to say how they should live their lives, but I would caution extending my credit line even further, as life does have a habit of dropping a clanger now and then.

It certainly has in my life, so yes, a cautionary tale indeed.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter0 -

I don't think you've fully realized you can't borrow your way out of debt, even more so sercuring it to your home, 96k is alot to of built up / not paid back & would scare off almost all lenders.Even if you did manage to go along with your plan, with that many credit cards, you'd be very tempted to spend on them again = more financial trouble / going round in circles.Either some serious life budget changes need to be made, or drastic measures will need to made later down the line, no savings is also huge worry, I agree with the OP's with your dangerous view - 1 unpredictable / avoidable life event & it will come crashing down on you like a house of cards.Why risk your home even further, when you've got cards on 0% & a healthy income, IMHO a reality check is needed for amount you've already borrowed. which to most is a scary amount.My advice would be to concentrate on getting your debt level down, by strict stripping back of finances ASAP.0

-

I must confess, I hadn't realised how much of the debt was at zero percent. It really doesn't make sense to turn 0% unsecured debt into a secured interest charging loan.

I get that you don't want to change your lifestyle, but it really would be short term pain to get you into a situation where you are back leading your lifestyle while being able to afford your debt. Or slightly longer term discomfort - if you said no holidays this year and took £300 out of your £900 spend on beauty treatments, clothing, other child expenses, presents, entertainment and cleaner, you pay off the amex by Christmas. Assuming no changes to interest rates by then, if you really can't go on with such stringencies, you then have £300 a month to add back to your budget.Statement of Affairs (SOA) link: https://www.lemonfool.co.uk/financecalculators/soa.phpFor free, non-judgemental debt advice, try: Stepchange or National Debtline. Beware fee charging companies with similar names.2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards