We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Is now a good time to take an annuity ?

Comments

-

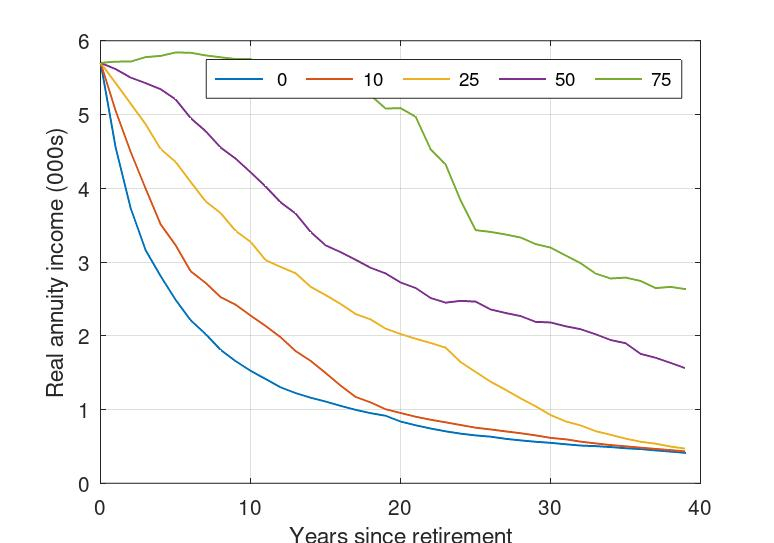

The real income (i.e., after adjusting for historical UK inflation - taken from macrohistory.net ) from a level annuity generating £5.7k per year at purchase is given at the 0th (i.e. worst case), 10th, 25th, 50th (i.e., median), and 75th percentiles in the following figure.

In the median case, the instantaneous real income fell below that for an RPI annuity (i.e., £3.3k) after about 17 years, while in the worst case (towards the end of WWI), the real value of the income from the level annuity only took about 4 years to drop below £3.3k (it recovered a bit during the deflation that occurred at the beginning of the 1920s). However, in 25% of historical retirements, the income from the level annuity exceeded that of the RPI annuity for up to about 30 years. I note that this is instantaneous income NOT accumulated income.

Choosing whether to get a level or an RPI annuity then comes down to how it fits in with your retirement plan. If you want it to provide longevity insurance (i.e., to provide a known real income even if you live a long time), then the RPI annuity is more certain to do so. However, if the purpose of the annuity is to provide an income boost early on in the retirement, then a level one may be more appropriate. However, it is worth noting that in 25% of historical cases, that income boost lasted less than 10 years.

Of course, which was the best choice will only be known with hindsight since future levels of inflation are unknown and unknowable.

3 -

From a political and Bank of England policy viewpoint I think it's fair to assume at least one Parliamentary term of extreme aversion to inflation much above 2-3%.0

-

It’s a complicated scenario but I will be taking a 10 year fixed Annuity at the start of the new tax year with some of my excess LTA pots in light of the change of legislation. Gone through everything in detail with my IFA and in light of the good rates, change of LTA rules it’s a bit of a no brainer as I really want some form of guarantee rather than live totally on drawdown in a world of volatility. For c£250k I will get £30k p/a for 10 years, exhausting that pot. I’ll top up using drawdown and that pot should still gain nicely. State Pension will also kick in before annuity ends.1

-

For comparison here's what using nothing but FSCS protected savings would deliver on £250,000 starting capital over ten years:

5% £31,824

4% £30,372

3.74% £30,000

3% £28,968

2% £27,612

Not quite perfect but I used a mortgage calculator for the pretty pictures https://www.moneysavingexpert.com/mortgages/mortgage-rate-calculator/ You probably can't get these rates within a pension.

A gilt ladder could do it for £250,552, level commencing payment in April. https://lategenxer.streamlit.app/Gilt_Ladder Some SIPPs do allow gilt buying.

The annuity is clearly far simpler and less work, though.

Savings or gilt ladder are probably better if you die during the term, in part because they are inherently 100% dual/unlimited life options with capital value until the end.

1 -

Yes, my (rough) calculations were based on the diminishing value of each payment. 18 annual payments of £5700, when inflation is reducing their value, don't really give me back the value of my initial £100K.westv said:

That's where I disagree with the calcs though. The buying power may diminish but the actual amount doesn't so 100,000/5700 = 17.54TJ666 said:

It's easiest to see if you think about periods of very high / hyper inflation. If I'd spent 100K Zimbabwe dollars buying a level $5700 annuity in 2008, the first payment (and all subsequent payments) would have been worth much less than a cent. I wouldn't consider that as 'getting my money back' even once they'd paid me a nominal 100K that was worth basically nothing.

("Zimbabwe's peak month of inflation is estimated at 79.6 billion percent month-on-month in mid-November 2008."

https://en.wikipedia.org/wiki/Hyperinflation_in_Zimbabwe )

0 -

With interest rates higher than they've been for a while the payout rate on an annuity will look attractive. However, the key is to make sure an annuity fits in with your retirement plans. If you have a DB pension an annuity might not be your best option and maybe the flexibility of DC drawdown is a better solution. If you want guaranteed income an annuity will do that and then you need to decide on whether or not you buy one with index linking. So whatever the payout rate you should only buy an annuity if it's right for your circumstances.

I just got a lifetime annuity quote from an old teachers pension firm in the USA. I have a balance of $60k that I can turn into a lifetime annuity at age 63 and the lifetime income quote is for $5996/year without indexing. So that's a payout rate of 10%, and that looks good to me - with the usual caveats that I live long enough and inflation doesn't stay high during that time.

OldScientst's comments are spot on about the reasons for whether or not to pay for an indexed annuity. In my case it's just to get a bit more no hassle, guaranteed income to help with a potential move back to the UK. It's for convenience more than anything else, but I will have to deal with exchange rate risk as well as inflation.And so we beat on, boats against the current, borne back ceaselessly into the past.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards