We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

FIRE Girls Pension Diary - Aim High & Dream Big

Comments

-

Firegirl said:@MallyGirl I really hope my son can get an apprenticeship as that’s what he wants. He’s a lot of confidence and is the most motivated and determined person I know (Other than my husband who he takes after😆). I know once he gets out in the world he’ll be amazing and it’s just getting that first step. If anyone knows of construction apprenticeships/Brick Laying apprenticeships in Edinburgh/Midlothian let me know! How mad would it be if I got a pointer for him on this forum😆

Recently the Government announced 'hubs' to provide the skills required for the construction industry. I don't know the details but I did a very quick AI search but focused on Scotland (and that is pasted at the bottom of this reply to you).

I think if your son wished to work in the construction industry that would be an excellent move. Also try to encourage him to undertake the RICS qualification too (it's not that difficult and nowhere near as difficult as other professional qualifications). Salary wise it all depends on how hard he works and where his career takes him (but avoid becoming an architect as the salaries are notoriously poor).

Over the next 10 years at least I would say (personal but very informed opinion) the construction industry will boom so a great career for your son. If he could also demonstrate he has good finance skills too that would definitely work in his favour.

Wishing you and your son all the very best.

From my AI search:In Scotland, the government’s recent £820 million Youth Guarantee announcement works alongside the existing Young Person’s Guarantee. This ensures that every 16-to-24-year-old has access to a job, apprenticeship, or training.

Specifically for construction, the government is rolling out guaranteed paid work and specialized training hubs in key Scottish regions.

1. The Jobs Guarantee (Central & East Scotland)

A major part of the December 2025 announcement is the Jobs Guarantee scheme.

The Offer: For 18-to-21-year-olds on Universal Credit who have been searching for work for 18 months, the government will provide six months of fully subsidized paid work (25 hours per week at the minimum wage).

Location: This is launching in Central & East Scotland starting in Spring 2026.

How to access: You must speak to your Jobcentre Plus Work Coach, as they are the ones who manage the referrals for these paid roles.

2. Construction Training Hubs & Academies

While England uses "Technical Excellence Colleges," Scotland uses a network of Youth Hubs and specialized academies to deliver the same 6-week intensive construction training.

Youth Hubs: Over 360 locations are being established across Great Britain. In Scotland, these hubs bring together Skills Development Scotland (SDS) and the DWP to offer "one-stop" access to construction training.

Tigers Construction Academy (Glasgow/Bishopbriggs): One of the most prominent hubs, they have a "Next Steps to Construction" intake starting on March 23, 2026. This 6-week course covers brickwork, joinery, and painting, and includes your CSCS card.

Regional Construction Skills Centres: Locations like the East Lothian Construction Skills Centre (at the Wallyford Learning Campus) work with Edinburgh College to provide direct routes into trades for young people.

How to Get Started Now

Your Situation Recommended Step Link / Contact On Universal Credit Message your Work Coach about the "Youth Guarantee Construction Pathway." Universal Credit Login Not on Benefits Contact Skills Development Scotland (SDS) for a referral to a local hub. My World of Work Looking for a Trade Register for a Construction Skills Bootcamp or the Tigers Academy intake. Tigers Academy Info Key Benefits of These Hubs

Practical Training: Most courses focus on hands-on skills (joinery, bricklaying, plumbing).

Essential Qualifications: They usually cover the cost of your CSCS Green Card, which you need to set foot on a site.

Guaranteed Interview: Completion of the 6-week course almost always leads to a guaranteed interview with a local construction firm.

4 -

Thanks so much @sarahb16 I really appreciate this information ❤️ He has done level 5 construction so that’s a great start for him. I’ll see if he knows about these hubs!Mortgage balance Feb 2015 start of MFW Journey-£245316.06/Aim to be mortgage neutral 2022 — Target for May 2024 14 Year Target Balance MF50 = £89,535 — Mortgage Balance £106, 000—Target for May 2024! £89,535

Retirement Planning

Starting Position (Jan 2024) : Pension 1-£165,000/Pension 2-£50,000/Pension 3-£9,500/ISA-£87,000/Total-£311,5001 -

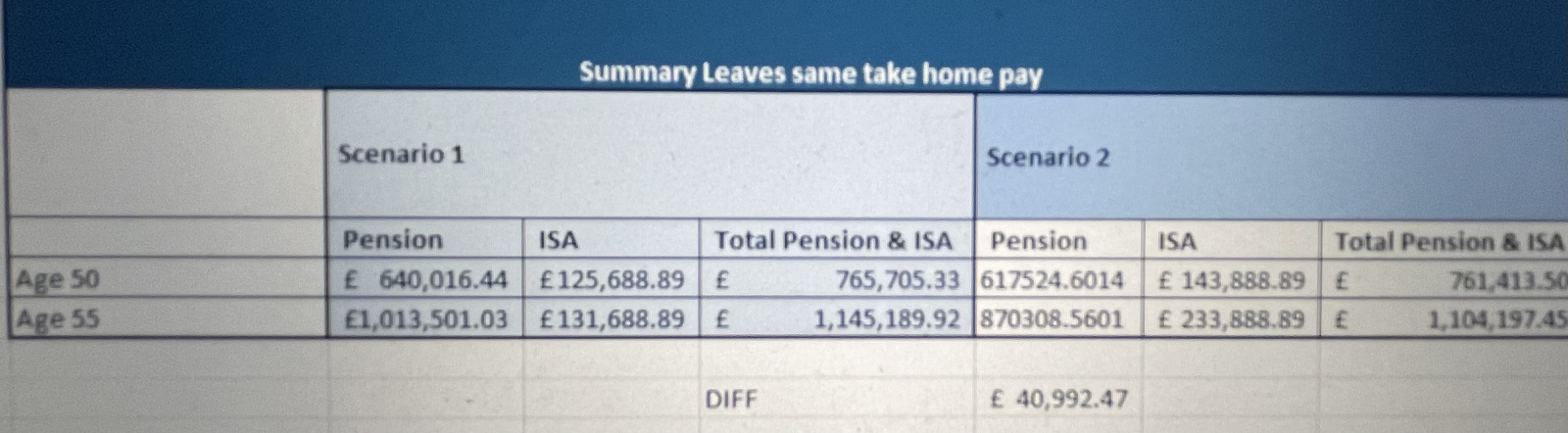

Ready for a very geeky post!!!!

There’s a big spreadsheet behind this summary table.

Both scenarios leave me with same take home pay and in the calcs I have included an estimated 5% APR.

Scenario 1 is high salary sacrifice to pension (to reduce tax) and low contribution to ISA.

Scenario 2 is scenario 1 until pension changes take place and then I would change to much lower salary sacrifice amount up to company match amount and high contribution to ISA. (ISA contributions made after tax.

On the assumption I work until I’m 55, I need to work out estimate which option is best.

My plan is to work it out how much I want to take out each month when I’m retired. Then work out every years estimated inflation. Keeping the tax brackets the same calculate how much tax I would pay for drawing down, and see what it looks like. If I pay tax on my salary and pay the bulk to my ISA I work out I’ll have approx £40k less savings overall. I think psychologically I’d rather have more in my ISA but I’m not sure.

There are so many factors that can change over time so this is far from an exact science but it might help me come to a more informed decision based on today’s circumstances.

Anything I’ve missed that I should take into account?

Mortgage balance Feb 2015 start of MFW Journey-£245316.06/Aim to be mortgage neutral 2022 — Target for May 2024 14 Year Target Balance MF50 = £89,535 — Mortgage Balance £106, 000—Target for May 2024! £89,535

Retirement Planning

Starting Position (Jan 2024) : Pension 1-£165,000/Pension 2-£50,000/Pension 3-£9,500/ISA-£87,000/Total-£311,5001 -

You have £40k extra in scenario 1, but you potentially need to pay tax on an additional £140k to get it out of the pension. If you can take it out at 15% effective tax ( 25% tax free and then 20% tax on the remaining 75%) you'd pay about £21k tax and still be about £20k ahead. If you end up taking it out at a higher tax rate, that advantage would disappear.

0 -

What is the inflation forecast in your scenarios?I think....0

-

@af1963 thanks for that calc because I hadn’t worked that out yet so you saved me a job!

@michaels I haven’t included inflation in the above calcs yet as they are estimating the build up of the pension/ISA pot. I will include inflation when estimating withdrawal for the 2 scenarios to try and work out if I’m likely to hit the higher tax bracket.

Mortgage balance Feb 2015 start of MFW Journey-£245316.06/Aim to be mortgage neutral 2022 — Target for May 2024 14 Year Target Balance MF50 = £89,535 — Mortgage Balance £106, 000—Target for May 2024! £89,535

Retirement Planning

Starting Position (Jan 2024) : Pension 1-£165,000/Pension 2-£50,000/Pension 3-£9,500/ISA-£87,000/Total-£311,5001 -

Won't inflation also impact in the build up, pushing scenario 1 over the TFLS max already?Firegirl said:@af1963 thanks for that calc because I hadn’t worked that out yet so you saved me a job!

@michaels I haven’t included inflation in the above calcs yet as they are estimating the build up of the pension/ISA pot. I will include inflation when estimating withdrawal for the 2 scenarios to try and work out if I’m likely to hit the higher tax bracket.I think....0 -

Oh I hadn’t even considered TFLS yet as was focused on working out what I could build up for each scenario.Goodness this is what people say pensions are complicated. I need to consider potential draw down plan, taking into account inflation, Tax free slump sum limit, estimated growth, Income Tax.

Thats def not a weekend job 😳😆Mortgage balance Feb 2015 start of MFW Journey-£245316.06/Aim to be mortgage neutral 2022 — Target for May 2024 14 Year Target Balance MF50 = £89,535 — Mortgage Balance £106, 000—Target for May 2024! £89,535

Retirement Planning

Starting Position (Jan 2024) : Pension 1-£165,000/Pension 2-£50,000/Pension 3-£9,500/ISA-£87,000/Total-£311,5001 -

Listening to some pretty high profile people recently they expect tax current thresholds to be extended beyond 2031.

If that's the future we are looking at it's probably best to max out the ISAs, cash ladder gilts in GIAs etc after the pension is optimised e.g. max employer conts, sal sac, drop a tax band etc.0 -

@NormalNorman

yes I will base my calculations on the idea that the tax thresholds won’t move.Currently I salary sacrifice to bring my self below the Higher rate tax in Scotland which is £43,663 to £75,000 42%.Im looking forward to seeing how it’s all worked out this tax year end because I’ve changed the salary sacrifice percentage a few times through the year, as I was settling into my new perm salary. Next year I’ll have it worked out to keep it the same all year.

I’m thinking of doing the cash ladder as withdrawal method but again yet to figure out exactly my cash ladder method and funds etc.

Ill be busy in work the next while so ill need to carve out time to have a go at working it all out!Mortgage balance Feb 2015 start of MFW Journey-£245316.06/Aim to be mortgage neutral 2022 — Target for May 2024 14 Year Target Balance MF50 = £89,535 — Mortgage Balance £106, 000—Target for May 2024! £89,535

Retirement Planning

Starting Position (Jan 2024) : Pension 1-£165,000/Pension 2-£50,000/Pension 3-£9,500/ISA-£87,000/Total-£311,5001

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards