We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

National Insurance Gaps

Lynsey89

Posts: 150 Forumite

I currently have gaps in my national insurance, I am only 34yo, but wondering if it is worth paying for those gaps now whilst I can.

I have 10 years of full contributions and 8 years where I didn’t contribute enough.

The cheapest years to buy are £221.90 of which there are two, one at £412.50 and the others go up to around £700.

I would only pay for the cheaper ones.

Do you think it is worth it?

I have 10 years of full contributions and 8 years where I didn’t contribute enough.

The cheapest years to buy are £221.90 of which there are two, one at £412.50 and the others go up to around £700.

I would only pay for the cheaper ones.

Do you think it is worth it?

0

Comments

-

Do you expect to add enough years from future credits/employment over the next 30-35 years?Lynsey89 said:I currently have gaps in my national insurance, I am only 34yo, but wondering if it is worth paying for those gaps now whilst I can.

I have 10 years of full contributions and 8 years where I didn’t contribute enough.

The cheapest years to buy are £221.90 of which there are two, one at £412.50 and the others go up to around £700.

I would only pay for the cheaper ones.

Do you think it is worth it?

If so then it seems unnecessary to pay for the older years.1 -

What is your current amount at April 2023 ?You have another 34 years to get the around 25 (answer to above question will confirm) more years needed so maybe 9 years spare to fill any needed gaps. If you have the £850 going spare then you may consider it worthwhile, it is a very tempting proposition though not really necessary. Are you currently getting NI credits by working or other means ?1

-

At the end of the day, it's a gamble. I think I would buy the two cheapest years, and trust that I will continue to work or claim a benefit that includes NI credits to give me a state pension. If the pension rules change in future, you could be better off if you have more years already 'banked', but there is a high liklihood that you will get all the full years you need before retirement, so it's not worth spending too much on this.The comments I post are my personal opinion. While I try to check everything is correct before posting, I can and do make mistakes, so always try to check official information sources before relying on my posts.1

-

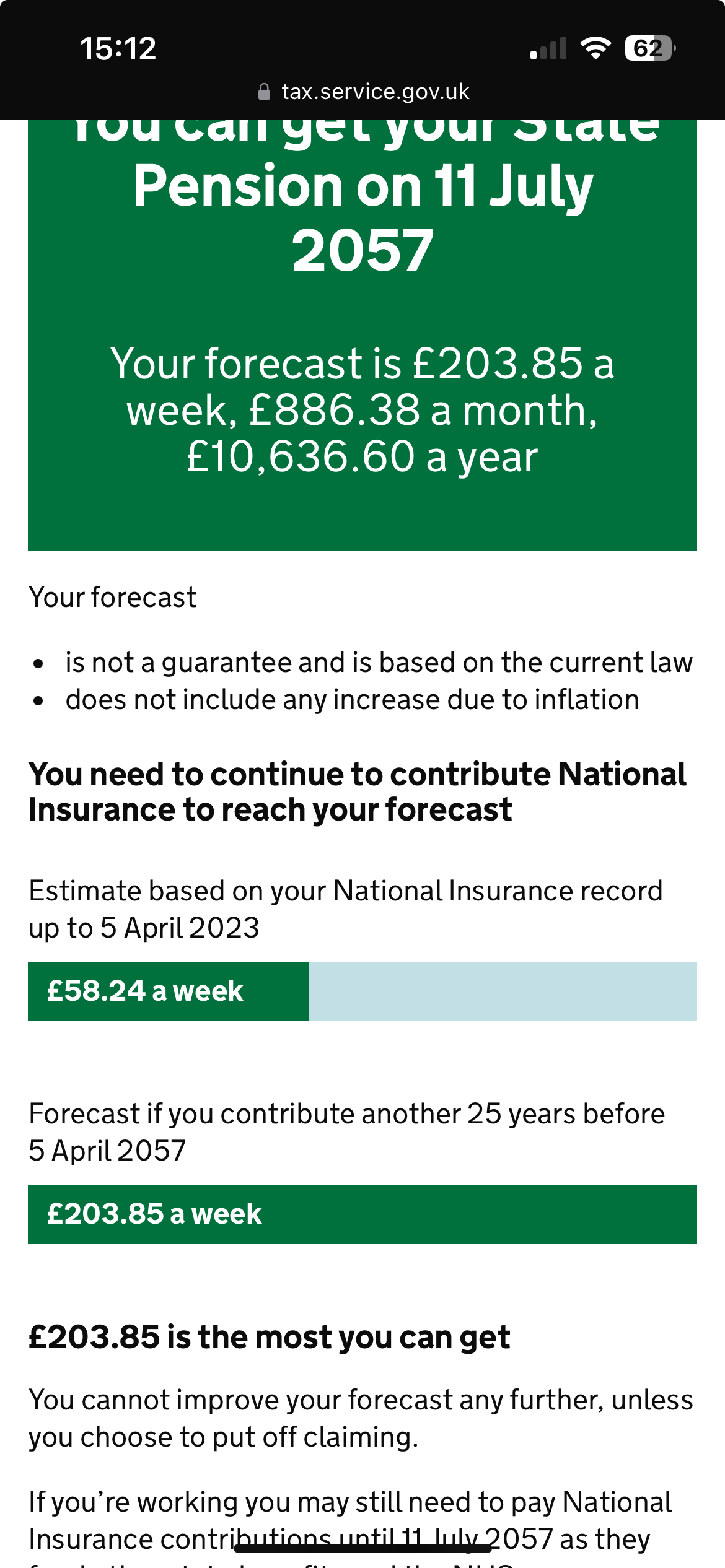

If you mean my forecast it’s £203.85 a month or £10,636.60 a year.molerat said:What is your current amount at April 2023 ?You have another 34 years to get the around 25 (answer to above question will confirm) more years needed so maybe 9 years spare to fill any needed gaps. If you have the £850 going spare then you may consider it worthwhile, it is a very tempting proposition though not really necessary. Are you currently getting NI credits by working or other means ?

I am currently working and don’t see a reason why this would change in the future, apart from maternity leave this year which I’ll get credits for.0 -

If you mean my forecast it’s £203.85 a month or £10,636.60 a year.

No, a bit further down, what you have in the bag so far.

And the one below that tells you how many more years you need to reach that top line amount.

1 -

You need another 25 years with 34 to get there. You are working and will get credits from that, maternity leave and then from child benefit, guaranteed if you become a SAHM, for the next 12 years so half of that 25 already covered. As tacpot12 above stated, maybe take a punt on the 2 cheapest ones if you really want to but beyond that not really worth it as you are not in desperate need of any extra years.

1 -

Early retirement is the main potential reason to buy those two years. Maybe not returning to work after children.

There's also the possibility of a n increase in the number of years needed from the 30 for basic state pension until 2016 to 35 for those starting in 2016 to get the full new state pension. Currently looks unlikely.

I did buy years I didn't strictly need to buy before that change and wouldn't be able to get a full new state pension if I hadn't.1

Thanks, this is mine

Thanks, this is mineConfirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.8K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.8K Work, Benefits & Business

- 603.4K Mortgages, Homes & Bills

- 178.2K Life & Family

- 260.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards