We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Actively Managed Pension Charges.

Comments

-

Try Albermarle's list here:Many of those will accept employer/director contributions. I think that's what you're looking for?N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Ripple Kirk Hill Coop member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.0 -

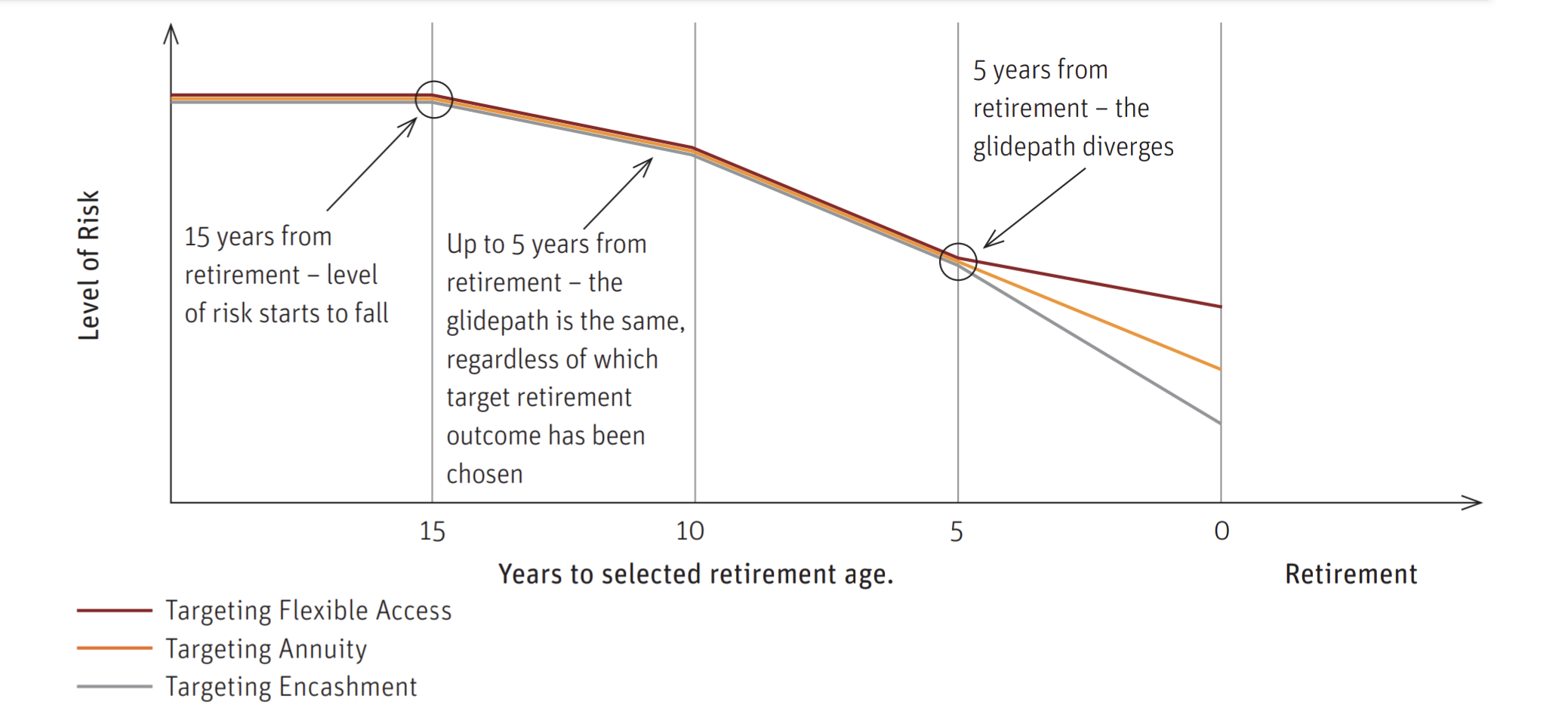

Tired of pensions now. It's draining. Turns out one of my workplace pensions can be used, it's possible to change employer to my company and pay net pay via direct debit. Over the last few years, it's performed pretty much the same as the pension policy I was being sold and it's invested in similar markets.

The pension advisor made a big point about lifestyling and how that's likely to limit gains in the final years, however the risk category I'm in, I'm hoping it will have a limited effect. Along with that, the retirement age is set 5 years higher then when I plan to retire, so lifestyling will be delayed.

0 -

Are you intending to buy an annuity when you retire? Thats the point of Lifestyling - it might limit absolute gains, but what it does do is align your pension pot value to the value of an annuity you can buy.Bod_1234 said:Tired of pensions now. It's draining. Turns out one of my workplace pensions can be used, it's possible to change employer to my company and pay net pay via direct debit. Over the last few years, it's performed pretty much the same as the pension policy I was being sold and it's invested in similar markets.

The pension advisor made a big point about lifestyling and how that's likely to limit gains in the final years, however the risk category I'm in, I'm hoping it will have a limited effect. Along with that, the retirement age is set 5 years higher then when I plan to retire, so lifestyling will be delayed.

if you are intending to stay invested and draw down your pension when you retire, then a fund that includes Lifestyling is unlikely to be appropriate for you.0 -

That the thing, I don't know. I live in the moment, font think about the future too much. I don't have a large expenditures, my monthly outgoings in total, all in are less that £1k. So I expect I will take the 25% lump sum and then draw the rest as and when in as most tax efficient way as possible, at the time.artyboy said:

Are you intending to buy an annuity when you retire? Thats the point of Lifestyling - it might limit absolute gains, but what it does do is align your pension pot value to the value of an annuity you can buy.Bod_1234 said:Tired of pensions now. It's draining. Turns out one of my workplace pensions can be used, it's possible to change employer to my company and pay net pay via direct debit. Over the last few years, it's performed pretty much the same as the pension policy I was being sold and it's invested in similar markets.

The pension advisor made a big point about lifestyling and how that's likely to limit gains in the final years, however the risk category I'm in, I'm hoping it will have a limited effect. Along with that, the retirement age is set 5 years higher then when I plan to retire, so lifestyling will be delayed.

if you are intending to stay invested and draw down your pension when you retire, then a fund that includes Lifestyling is unlikely to be appropriate for you.

The pension I have sort of caters for this by applying different amounts of lifestyling, depending on risk profile and how I plan to take money, mine is currently set to adventurous risk and to draw from it, as and when, flexible access. My retirement date on the policy is also left at default, and is likely 5 years further out than reality, so would also limit lifestyling, that's my assumption. 0

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.6K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards