We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Is now a good time to keep the Bonds you’ve got?

Comments

-

Altior said:Linton said:

My point was that people may have got the impression that something different steadily happens to returns as new bonds replace old bonds which have reached maturity. This impression would be incorrect with respect to the value of the investment because at the current low price the "old" bonds are already the equivalent of the same value of new bonds. The arithmetic changed increasing the ongoing % total returns immediately the market price of the underlying bonds changed.JohnWinder said:‘new bonds will have exactly the same total return as old bonds with the same maturity date now have. ’Agree.

‘So new bonds replacing old wont of itself help.’Disagree. We’ve already established that the old bonds in the fund are now (after the wipe-out) yielding more than before ‘which will help’ as you said in the second para of your first post. Plus, as the new bonds now have the same yield as the old post wipe-out bonds, as you just said, both sets of bonds, old and new, are now ‘winners’. What am I missing?

If interest rates fall it will be the inverse of what has just happened. Yes the trading value of 'legacy' bonds already in the fund will recover, but the fund will also now contain recently purchased bonds, and their theoretical market value will increase if interest rates drop. It would be similar as shorting these funds if you knew or predicted that they would be rapidly beaten up, the long term known hard maths is largely irrelevant, just playing the short term swing.

The 'bet' element of it, of course, is that interest rates will fall again, but not for a reasonable period of time, allowing the fund to 'stock up/rotate' into more favourable gilts. We won't see near zero rates again, so I don't anticipate that it will be quite so rapid or dramatic.

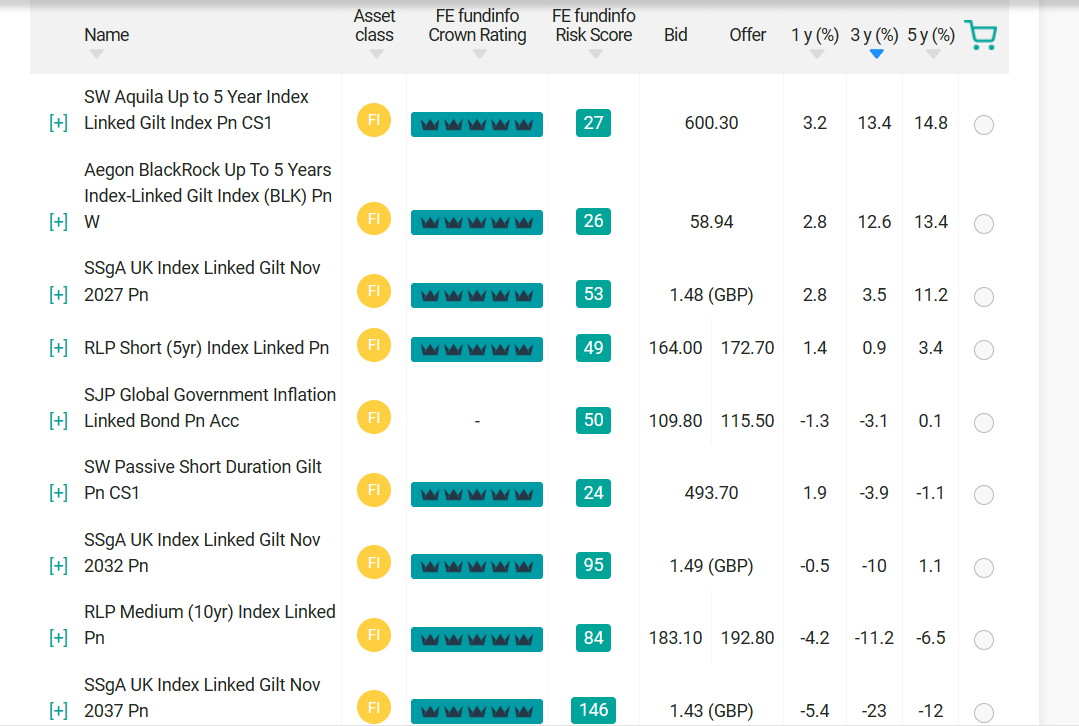

A linker fund I have been betting on for a good while is RLP Short (5 Years) Index Linked. Better people than me might be able to explain why the value does not appear to have especially suffered like other linker gilt funds (other than it is a short fund, ergo lower risk), but it can be seen from the holdings that it is already rotating into linkers with a stronger rate (and yes, the fund is still down significantly compared to the risk free rate). [This is not the only gvnt bond fund I am buying]

I might not be a better person than you but I hope I can explain why short dated inflation linked bonds have not suffered in the same way as longer dated ones....

Index linked bonds are priced similarly to fixed rate bonds of the same duration that return the market's expectation of inflation between now and maturity. The price above or below par (£100) represents the difference in overall return between the two.

So for example before interest rates rose fixed rate bonds may have been returning say 1 % whereas expected long term inflation is fairly constant around perhaps 2.5%. Clearly a bond returning 2.5% is far more desirable than one returning 1.0% and so will be priced much higher. if fixed interest rates then quickly rise to 5% the effectively 2.5% index linked fund suddenly becomes very undesirable and the price collapses.

However time to maturity is important. If maturity is 30 years away then difference of 1.5%/year return will be very large whereas if it is just 1 year away the difference in return would be small compared with the face value of £100 (or in the case of IL bonds £100 increased by inflation).

I disagree with your analysis of the difference between new bonds and old ones. but wont go into details now beyond saying that immediately the interest rates rose the value of the old bonds fell by exactly the right amount to make £100's worth of old bonds provide the equivalent overall return (adding subsequent interest to subsequent capital gains) as £100 of new bonds.

1 -

Thanks Linton. I understand the difference in the duration, ie that the longer the duration the fund is, the more it will be sensitive to base rate changes. I suppose I was referencing that particular short linker fund. To be fair I have not investigated thoroughly how it compared to similar funds.

An example I can specifically point to is the Vanguard UK Inflation-Linked Gilt Index Acc fund. We won't get into the politics of it but I bought it right at the bottom, when it was peak attack Truss time back in Oct 2022. I sold the following month when the panic was over. Clearly those moves were not rational calculations by people buying and selling, this was fear in the market and panic selling/dumping (more than one reason). I am after timing here, only to provide a tangible example (off the top of my head I made circa 20% gain in a month on the 'trade').0 -

Out of 160 funds in the entire class on TN it is showing 4th (over 3 years). With two outliers right at the top. I assume the differential for the top two is/was their holdings at the time of interest rate carnage. There are however significant disparities between the fund performances in this category.0 -

My amateur thoughts are...Altior said:

Out of 160 funds in the entire class on TN it is showing 4th (over 3 years). With two outliers right at the top. I assume the differential for the top two is/was their holdings at the time of interest rate carnage. There are however significant disparities between the fund performances in this category.

The top 2 funds are both very short duration ("up to 5 years") index funds. You would expect them to hold much the same assets and to have performed broadly in line with index rates. I dont know the cause of the difference in performance, it may be something artificial like when in the year the interest is paid.

The 3rd fund is "5 years" which I means an average of 5 years. I think the figures can all be correlated with time to maturity. Charges may have had an impact as well, especially if some have bundled charges and some dont. TN tells me that the RLP fund has a TER of 1% whereas the SW Aquila fund is 0.08%. I cannot believe that this is just greed on the part of RLP.

My belief is that gilts are mainly held and traded by professionals in large institutions seeking to meet their financial needs, or playing the market, as directed by computer optimisation.. Not by frightened or over-enthuisiastic members of the public. I guess but dont know that the short term blips such as the Truss event are more to do with people delaying buying until the outcome was clear rather than selling in a panic.0 -

The market turmoil just over a year ago was a self fulfilling spiral to a degree. The gilt market rightly reacted negatively to the Truss/Kwarteng budget proposals and this was compounded by collateral calls on pension funds which had used leverage to hedge their liabilities. All at the same time as QT was happening.....pension funds sold liquid assets, sometimes gilts, to meet the collateral calls....essentially we had market moves in gilts that might have taken a year or so play out compressed into a week. That's a very short and not particularly comprehensive summary of it, but it was a disorderly market essentially triggered by irresponsible government behaviour.

A perfect storm......compounded by market liquidity drying up. The blame game followed......

The bigger issue now is probably the inflation outlook...UK inflation has remained stubbornly higher than other countries on the whole, and the cost of this in debt servicing for ILGs is not trivial. Tax cuts and/or public spending increases are not likely to go down well with the bond market. That said, many UK institutions (DB pension schemes and insurers) are now channelled towards gilts by various forms of regulatory constraint.0 -

Not sure the fog of uncertainty ever really lifts in the financial markets.Hoenir said:

All dated bonds will eventually return to par nominal value upon maturity. Any maturity proceeds received and income generated will be reinvested into stock at the prevailing prices. Bonds have undergone a short sharp correction in response to the change in interest rate environment.theblueflash said:The question is, and I’ve tried to read up on this, do I keep my money invested and hope for recovery at some point, given I don’t really know the duration of the bonds/gilts in these funds, or is there no-way they can “recover” unless some kind of economic shift in interest rates / markets dictate?

Worth remembering that interest rate changes take around 18 months to feed through to the real economy. On a broad level equities are far from being out of the woods. Companies , like mortgage borrowers, face the challenge of refinancing borrowings at far higher cost. Increased interest costs are a straight hit to the bottom line of company profitability. Constraining investment in projects that require up front capital outlay.

If you are not concerned with the potential volatility. Maintaining an 80/20 stance across your portfolio. Might well be a good course of action for the time being. Going to take time for the fog of uncertainty to lift.0 -

I did consider this, the Scottish Widows one labelled up to 5 years for example. The fund objective states that it effectively targets tracking the FTSE UK Gilts Index-Linked Up To 5 Years Index. RL stated objective is to provide returns which are linked to the rate of inflation for investors with a five year investment term.Linton said:

My amateur thoughts are...Altior said:

Out of 160 funds in the entire class on TN it is showing 4th (over 3 years). With two outliers right at the top. I assume the differential for the top two is/was their holdings at the time of interest rate carnage. There are however significant disparities between the fund performances in this category.

The top 2 funds are both very short duration ("up to 5 years") index funds. You would expect them to hold much the same assets and to have performed broadly in line with index rates. I dont know the cause of the difference in performance, it may be something artificial like when in the year the interest is paid.

The 3rd fund is "5 years" which I means an average of 5 years. I think the figures can all be correlated with time to maturity. Charges may have had an impact as well, especially if some have bundled charges and some dont. TN tells me that the RLP fund has a TER of 1% whereas the SW Aquila fund is 0.08%. I cannot believe that this is just greed on the part of RLP.

My belief is that gilts are mainly held and traded by professionals in large institutions seeking to meet their financial needs, or playing the market, as directed by computer optimisation.. Not by frightened or over-enthuisiastic members of the public. I guess but dont know that the short term blips such as the Truss event are more to do with people delaying buying until the outcome was clear rather than selling in a panic.

The SW holdings don't look particularly exciting to me, compared to others, but only go out to 2028, so shorter duration overall for sure (would be nice to be able to get a snapshot of this from 3 years ago)1 UK I/L GILT RegS 1.25 11/22/2027 23.49 2 UK I/L GILT RegS 2.5 07/17/2024 21.70 3 UK I/L GILT RegS 0.125 08/10/2028 19.60 4 UK I/L GILT RegS 0.125 03/22/2024 19.22 5 UK I/L GILT RegS 0.125 03/22/2026 15.94

Compared to RL 5Y. SW has circa 45% over 0.125%, RL looks to have a little more. If my thin understanding is correct, the 2024 holdings will mature and will rotate into what is available around that time, I'm assuming new issues.1 1¼% Index-linked Treasury Gilt 2027 18.87 2 0 1/8% Index-linked Treasury Gilt 2026 15.71 3 2½% Index-linked Treasury Stock 2024 11.65 4 1¼% Index-linked Treasury Gilt 2032 9.96 5 0 1/8% Index-linked Treasury Gilt 2028 9.81 6 0 1/8% Index-linked Treasury Gilt 2036 5.57 7 0 1/8% Index-linked Treasury Gilt 2029 5.55 8 4 1/8% Index-linked Treasury Stock 2030 4.86 9 2% Index-linked Treasury Stock 2035 4.39 10 1 1/8% Index-linked Treasury Gilt 2037 4.21

My rudimentary understanding is that I want longer dated holdings with the more favourable rates as an entry point, which gives me a little more positivity for the RL fund. This of course ties in with the overall valuation, which is definitely outside the scope of my prevailing capabilities in this area!0 -

A forced sale/fire sale/distress sale/panic, whatever it was, it was very clear to me that assets were being traded below par. It stands that there was an opportunity in this space. Similar to the brief time that oil went negative. Many people assume that the market is uber efficient, but I don't. If the retail player is patient enough, opportunities present themselves, even playing as a tiny fish in a massive pond.MarkCarnage said:The market turmoil just over a year ago was a self fulfilling spiral to a degree. The gilt market rightly reacted negatively to the Truss/Kwarteng budget proposals and this was compounded by collateral calls on pension funds which had used leverage to hedge their liabilities. All at the same time as QT was happening.....pension funds sold liquid assets, sometimes gilts, to meet the collateral calls....essentially we had market moves in gilts that might have taken a year or so play out compressed into a week. That's a very short and not particularly comprehensive summary of it, but it was a disorderly market essentially triggered by irresponsible government behaviour.

A perfect storm......compounded by market liquidity drying up. The blame game followed......

The bigger issue now is probably the inflation outlook...UK inflation has remained stubbornly higher than other countries on the whole, and the cost of this in debt servicing for ILGs is not trivial. Tax cuts and/or public spending increases are not likely to go down well with the bond market. That said, many UK institutions (DB pension schemes and insurers) are now channelled towards gilts by various forms of regulatory constraint.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards