We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

First Time DIY Portfolio

Comments

-

The lesson for investors - sock picking would not be any easier, even if we knew the future.’

If I have 3 pairs of UK socks and 3 pairs of US socks in a bag, how many will I have to pick out to be sure of a matching pair......? (Sorry

)0

)0 -

Very well with many multi-asset portfolio/funds with underlying passives. e.g. HSBC GS vs VLS.Fair enough. We should look at the methods Morningstar used for their analysis; it might be a flawed study. But we should also quantify how well ‘very well’ is for the GS-types compared to a two fund portfolio we might hold, although they don’t have a very long representative (of time) history.0

-

You might also need to drill down on the "this outperforms that 80% of the time"......it might but the level of that outperformance also needs to be quantified.......ie if fund A makes 4% a year for 5 years, and fund B makes 3% a year for 4 years, and 10% one year, then fund A has indeed outperformed fund B 80% of the time, but a fund A investor would still end up with less money than a fund B investor, assuming they invested the same amount on the same day.1

-

Although the OP hasn't indicated placing the pension into ETF's it's worth reading about FSCS investment protection. This forum is split in opinion about ETF's and some won't buy them . I hold them at times but only the main ETF's UK domiciled and with large market capitalisation. Eg..VWRL, ISF etc where funds have billions in them.

Article is decent and reading the comments I came across a post about the IE platform. Scroll down near the bottom to post 53 by S M dated March 13th, 2023 ,8.29pm. Perhaps other posters can add to this ?

FSCS investment protection: are you covered by the investor compensation scheme? - Monevator

2 -

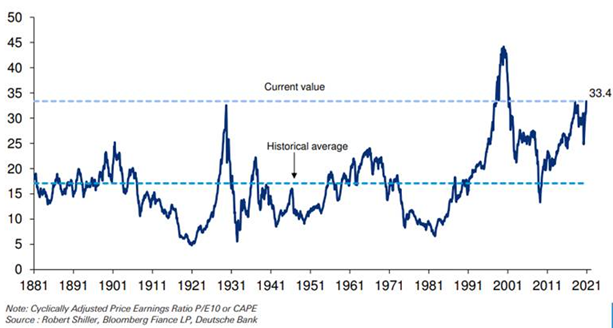

The idea holding cash when markets are so called overvalued doesn't pay off at all. Markets can stay overvalued for years and SP 500 is a perfect example. There's only been a few genuine cases in history where the P/E ratio was way too high. The last one was the dotcom boom where every share in the world became overbought. UK shares were over P/E 20 and never heard of. The recent pandemic crash sent valuations high due to one off hits to companies but they recovered. So how do you value the market ? If you decided P/E near 20 was too high you'd never have been invested in the US last 30 years.JohnWinder said:‘buying and holding, come what may, still generated better returns over the past 21 years, albeit by a narrow margin of around 0.76% per year.’ https://www.morningstar.com/portfolios/staying-invested-beats-timing-marketheres-proof

Unknown.png (613×328) (ritholtz.com)

S&P 500 PE Ratio - How the Price Earnings Ratio Helps You to Valuate the Companies in the Standard and Poor 500 - UndervaluedEquity.com

EZ_91bOXQAAp1Zo (1400×1169) (twimg.com)

When FED rates are high P/E's tend to be low and nearer 10. Recently P/E's have been high which has discouraged some from investing in the US. Wil it pay off ?

F9Mw2ZhWEAACG-C (900×501) (twimg.com)

Here's a chart I bookmarked recently showing a 6% FED rate which keeps the lid on equities . 100 years of data so if inflation doesn't fall then the markets mightn't hold up.

EybIWfVW8AMazW4 (680×470) (twimg.com)

0 -

Whilst the risk is low if you know what you are doing, it is worth noting that PI insurers increase their premiums to IFAs if ETFs are used in the recommendations because they are considered higher risk relative to the OEIC/UT. That may be more regulatory risk as the FOS is a bit nanny state in that respect.coastline said:Although the OP hasn't indicated placing the pension into ETF's it's worth reading about FSCS investment protection. This forum is split in opinion about ETF's and some won't buy them . I hold them at times but only the main ETF's UK domiciled and with large market capitalisation. Eg..VWRL, ISF etc where funds have billions in them.

Article is decent and reading the comments I came across a post about the IE platform. Scroll down near the bottom to post 53 by S M dated March 13th, 2023 ,8.29pm. Perhaps other posters can add to this ?

FSCS investment protection: are you covered by the investor compensation scheme? - MonevatorI am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

Thanks for this. There’s a lot to read in there and lots of things I do not understand. I saw the response from IE - comment 72 I think but that didn’t help me much either. So what’s the bottom line - where can I passively invest and be 100% covered (let’s say I have a £26k ISA and a £200k pension). Which types of funds and which platforms? Would I have to stay away from ETFs all together or if not how do I know which ones are safest?coastline said:Although the OP hasn't indicated placing the pension into ETF's it's worth reading about FSCS investment protection. This forum is split in opinion about ETF's and some won't buy them . I hold them at times but only the main ETF's UK domiciled and with large market capitalisation. Eg..VWRL, ISF etc where funds have billions in them.

Article is decent and reading the comments I came across a post about the IE platform. Scroll down near the bottom to post 53 by S M dated March 13th, 2023 ,8.29pm. Perhaps other posters can add to this ?

FSCS investment protection: are you covered by the investor compensation scheme? - Monevator1 -

Either stick to pension funds (which have 100% FSCS protection with no upper limit) or use UT/OEIC funds which have £85k per fund house (not per fund).RichardS said:

Thanks for this. There’s a lot to read in there and lots of things I do not understand. I saw the response from IE - comment 72 I think but that didn’t help me much either. So what’s the bottom line - where can I passively invest and be 100% covered (let’s say I have a £26k ISA and a £200k pension). Which types of funds and which platforms? Would I have to stay away from ETFs all together or if not how do I know which ones are safest?coastline said:Although the OP hasn't indicated placing the pension into ETF's it's worth reading about FSCS investment protection. This forum is split in opinion about ETF's and some won't buy them . I hold them at times but only the main ETF's UK domiciled and with large market capitalisation. Eg..VWRL, ISF etc where funds have billions in them.

Article is decent and reading the comments I came across a post about the IE platform. Scroll down near the bottom to post 53 by S M dated March 13th, 2023 ,8.29pm. Perhaps other posters can add to this ?

FSCS investment protection: are you covered by the investor compensation scheme? - MonevatorIts a risk based decision that only you can make. Thankfully, since 2013 when unbundling occurred, the difference between OEICs/UTs and ETFs in terms of pricing is minimal. Indeed, in some cases the OEIC/UT is cheaper and in many cases, it is virtually the same.

Would I have to stay away from ETFs all together or if not how do I know which ones are safest?

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

If using big ETF's from the established firms (Vanguard, HSBC, BlackRock, State Street to name a couple that I currently invest in) realistically how significant is the risk?dunstonh said:

Either stick to pension funds (which have 100% FSCS protection with no upper limit) or use UT/OEIC funds which have £85k per fund house (not per fund).RichardS said:

Thanks for this. There’s a lot to read in there and lots of things I do not understand. I saw the response from IE - comment 72 I think but that didn’t help me much either. So what’s the bottom line - where can I passively invest and be 100% covered (let’s say I have a £26k ISA and a £200k pension). Which types of funds and which platforms? Would I have to stay away from ETFs all together or if not how do I know which ones are safest?coastline said:Although the OP hasn't indicated placing the pension into ETF's it's worth reading about FSCS investment protection. This forum is split in opinion about ETF's and some won't buy them . I hold them at times but only the main ETF's UK domiciled and with large market capitalisation. Eg..VWRL, ISF etc where funds have billions in them.

Article is decent and reading the comments I came across a post about the IE platform. Scroll down near the bottom to post 53 by S M dated March 13th, 2023 ,8.29pm. Perhaps other posters can add to this ?

FSCS investment protection: are you covered by the investor compensation scheme? - MonevatorIts a risk based decision that only you can make. Thankfully, since 2013 when unbundling occurred, the difference between OEICs/UTs and ETFs in terms of pricing is minimal. Indeed, in some cases the OEIC/UT is cheaper and in many cases, it is virtually the same.

Would I have to stay away from ETFs all together or if not how do I know which ones are safest?0

{kind=link}

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards