We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Investment choices…..

Leigh-Anne_60

Posts: 521 Forumite

Whilst I’ve realised the importance of pensions for some time now, never really got in to the nitty gritty of individual investments beyond provider fact sheet ratings. So whilst I’m putting around 35% of my monthly salary in, not doing much to it after this

However, with my main pot, I did meddle one bored afternoon in work probably 10 years ago…. And never amended since.

However, with my main pot, I did meddle one bored afternoon in work probably 10 years ago…. And never amended since.

I see people on here reel off all sorts of insights to different funds and associated risks/factors, and honestly I am clueless.

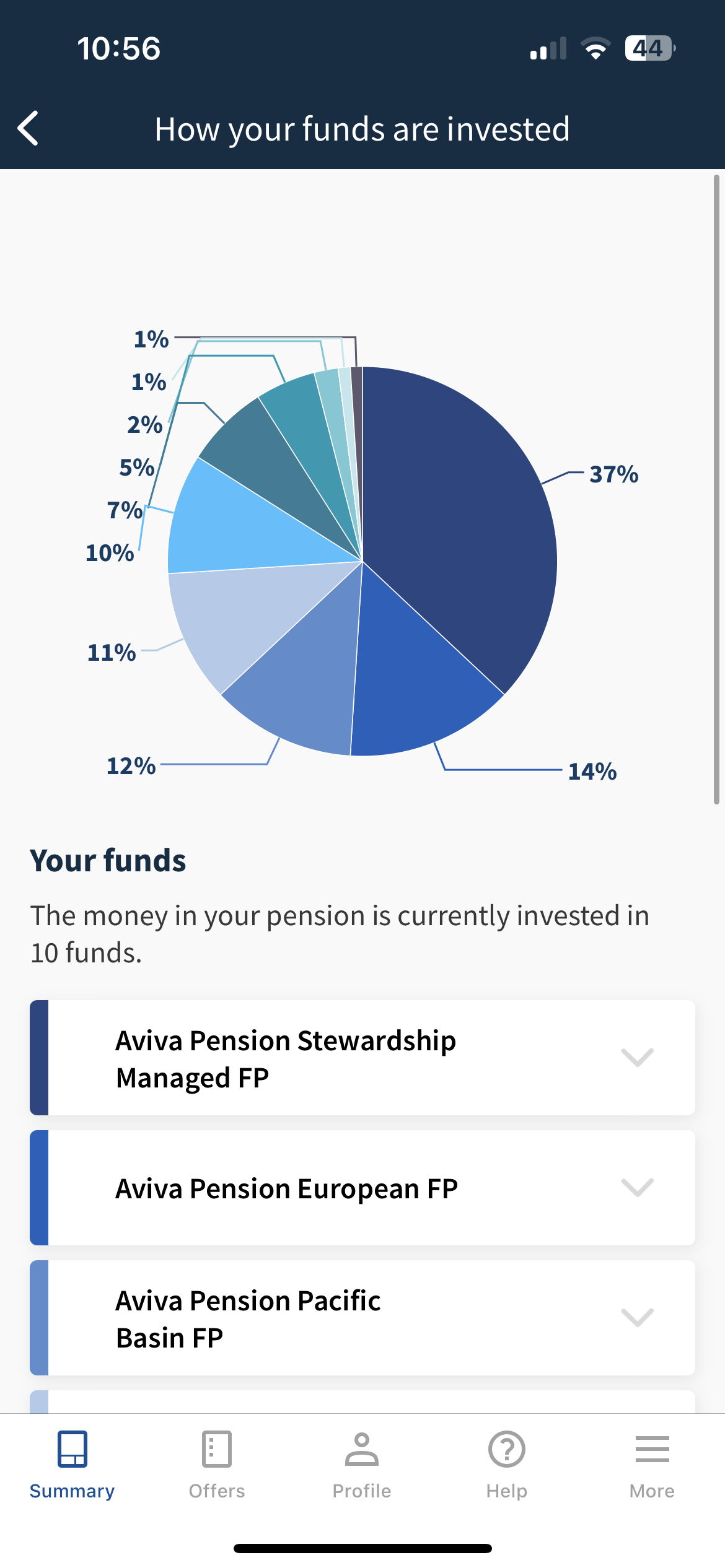

Have screenshotted my choices below and thinking I maybe should just put it all back in the stewardship fund, thoughts?

FYI, not too risk adverse….. happy to ride a few storms for at least the next 5 years when I’ll probably reign it in quite a bit

Have screenshotted my choices below and thinking I maybe should just put it all back in the stewardship fund, thoughts?

FYI, not too risk adverse….. happy to ride a few storms for at least the next 5 years when I’ll probably reign it in quite a bit

0

Comments

-

I have an Aviva Pension with access to a lot of those various funds. Some of which I’m invested in. I track them weekly and am happy to review, but the long and short of it is that the North American and Global funds above are allocated about 60% of my assets and future contributions. They have performed brilliantly in my view and I’ve done very nicely out of them.Leigh-Anne_60 said:Whilst I’ve realised the importance of pensions for some time now, never really got in to the nitty gritty of individual investments beyond provider fact sheet ratings. So whilst I’m putting around 35% of my monthly salary in, not doing much to it after this

However, with my main pot, I did meddle one bored afternoon in work probably 10 years ago…. And never amended since.I see people on here reel off all sorts of insights to different funds and associated risks/factors, and honestly I am clueless.

Have screenshotted my choices below and thinking I maybe should just put it all back in the stewardship fund, thoughts?

FYI, not too risk adverse….. happy to ride a few storms for at least the next 5 years when I’ll probably reign it in quite a bit

I’ll review in the morn and get back to you.1 -

You maybe need to look at at least some of the factsheets, the pie chart shows some 1%'s, which probably aren't doing much. You could start by looking into the Global fund, and see to what extent it covers eg Japan, and if Japan is also in the Pacific Basin fund. If so, do you need the Japan Index?I don't know these funds, but unless your pension is very large, it does seem rather a lot to keep track of.1

-

If I'm honest, the whole thing seems like a mess.

Various regional funds - e.g. North America, Dev Europe, Japan, but then the inclusion of a Global Equity Fund that covers all of these (Aviva Pen Global Equity FP Pn is 55.6% NA, 21.8% Dev Europe and 6.1% Japan). You then have things like the 'My Future Growth' fund, which are comprised of North America, Dev Europe and Japan Index trackers... A lot of funds all investing in exactly the same things.

To be honest, I got a headache just looking at this, so much overlap, you could probably achieve a very similar allocation by just holding one global fund.

I think you need to do some research and start again with this. If it was me, I would not consider any 'Managed' funds (that typically carry higher TER's) and would think about investing in one reputable global equity index tracker. If I wanted to hold bonds, I'd probably consider a global bond fund to complement it. I'd lose all the other noise in your portfolio.Know what you don't2 -

That’s why I like geographical trackers so it’s clear there is no overlap, which you certainly will have. Also agree the 1 and 2 % ones are just getting in the way. Overall no howlers so depends how much you want to get involved with it. Good luck1

-

You’re young enough to make it worthwhile reading Tim Hale’s book Smarter Investing. It’ll give you an idea how good or less good your current investment choices are, as well as a good sense of how different assets behave over time which might make your worries like now never re-appear. I’m sorry I missed your post twelve months ago when you agonised over the same issues; you could have been a year ahead in getting the understanding you need and will serve you well.

1 -

Who knows? how old are you and when are you planning to start needed the money?1

-

I concur with the above that it’s quite a spread of funds and depending on the value it may be far too many.It comes across as a bit of a scatter gun approach to cover all bases and we can all be a bit guilty of that at times!

I can comment on a few of the funds as I either hold them or did hold them.North America has served me very well. In the past 2.5yrs it has offered a 29% increase. I have about 30% of my pension invested there. North America is usually always a solid investment in good and challenging times.

Global Equity also has about 30% of my funds in it. It has returned 23% in the past 2.5yrs so again a good performer. To me it’s a solid global fund that you should be in.A lot of the rest I’ve considered, bought and sold out of or ignored. pacific Basin and Japan funds have all struggled of late so I cut my losses and for out. The Euro fund I did consider but was concerned about all that’s going on in the euro zone, the war in Ukraine etc and I ignored. Property and Multi asset are a no go for me, slow movers and just dead wood imho. The International fund is one I hold - it’s meant to be a reasonably safe house alongside a BG Managed fund which Aviva often offer. I first invested in the International fund 3yrs ago and it delivered solid growth of about 30% until about Oct 21 (like most BG funds) where upon it fell off a cliff and it currently sits at about 9% ahead of where it was 3yrs ago which is disappointing given where it was. However, it does appear to be on the rise showing about 6% growth over the past 3 months.

There should be good documents on all the funds, showing their risk rating etc. Previous form doesn’t predict future performance, but you can see there what’s doing well and what’s not. I currently have 6 funds - 3 described as above alongside BG Managed, Av UK small cos and AV UK equity as I felt that the Uk funds were devalued. I’ve shown modest growth in the UK funds that like a lot of funds started to show strain from Sept 21 onwards and dropped as much as 30% in a 12 month period. They’re slowly bouncing back and on 3yrs ago I’m about 11% ahead.Do plenty of reading, but also be mindful of the fees. The Aviva funds compare favourably to a lot of the Investment house funds that they often offer and are cheaper. Over the course of decades that does add up. Depending on the size of your pot I think you should streamline and focus your investment based on age, risk profile, your aspirations etc.etc.etc.

Please note all above is my views and not to be considered as any level of educated advice!1 -

Whilst tinkering too much with funds isn't always beneficial, would suggest to keep it as simple as possible....for the best part of this year I was using 5 regional equity funds in my work pension but the allocations move around which means at minimum an annual rebalance.....it became too much of a faff so i switched to two global equity funds albeit one is overweighted to US growth stocks so more volatile but hoping it works out with a long game approach. The two global equity funds will still need a periodic rebalance if I want to keep the allocations at 50% each but far less headache than managing 5 regional funds. My SIPP is also two funds, well ETF's....Dev world and EM...simple works just fine for me!

I think you will need to do some more research, look under the 'hood'of those funds then determine which funds will achieve your desired exposure/mix/risk etc2 -

The first one "Stewardship" is supposed to be an ethical fund, the others aren't. Nothing specifically wrong but I'd expect you'd either want them all ethical, or wouldn't care.1

-

Many thanks for all of your responses, and sorry for the headaches🤣. I shamefully admit to the gung ho selection processAfter my post last year, I did buy Tim Hales book, but again, shamefully it has laid downstairs unopened and gathering dust since.

I have made a few tweaks, getting rid of the smaller/duplicates ones. Going from 10 to 6. However will have further in depth change when I can put more time to it

For info the pot is worth £185k and all new contributions are going elsewhere. 47 years old and aspirations to retire sooner rather than later !! 0

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.8K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.4K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards