We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Sorting the debt:income ratio!

kaylog2915

Posts: 9 Forumite

Hello! Adding my own diary to keep me accountable!

My story - I'm a single (separated) mum to a little boy with disabilities. I work 30 hours in a decent job and just want to get us our own place that will suit us! (Currently private letting, not ideal! No shower, expensive storage heaters etc etc)

Have a small deposit of just under £6000 saved, but looking into mortgages and I keep getting told the same thing - my debt is too high compared to my income. So rather than trying to scrape by and afford something, I'd rather attempt to fire everything towards the debt just now so I am in a better position for applying for THE big debt aka mortgage, oh the irony haha.

I've been a big CC spender, buy now worry later, then wonder why i have no money at the end of each month. So starting to reign it in. I have issues with spending a lot on food, clothes, random little treats for me and my son. But it all adds up.

I have attempted an SOA and included below!

Statement of Affairs and Personal Balance Sheet

So credit cards, MBNA, Barclaycard, Tesco and Virgin are not 0%, they are charging interest. Actual percentages I am not sure, some of the cards have multiple 0% offers on them that have ran out at different times. The virgin balance - £1100 of that is actually my mums debt that she is giving me money for each month (the other £600 is my balance and is currently 0%). I'm thinking of clearing the tesco first as it's the smallest and will make me feel better to clear it fast.

Car PCP, guessing the amount, car was about £11000, im paying £205/month for the next 35 months and then assume there will be a balance at the end of roughly £4000 if i want to keep the car. I'll probably not keep it that long. I've only had it 13 months or i would think about getting rid for something cheaper.

During winter I can be paying up to £500 to heat my home (hence my urgency to move into my own place with GCH!), but summer I'm around £40. So I've calculated an average for the year.

Other issue, I pay for mines and my ex husbands life insurance (for my sons benefit, hence i'm still paying for ex!). I'm thinking from looking at others that i'm paying a ridiculous amount for two reasonably healthy mid 30s! The thought of changing it gives me a headache, they don't make these things easy!

Can't think of anything else atm! I just paid off my phone contract early with o2 as they were charging ridiculous amounts, so phone is now mines and I'm now only paying £12/month (last months bill was £73!!!)

Thanks for reading if you've made it here!!

My story - I'm a single (separated) mum to a little boy with disabilities. I work 30 hours in a decent job and just want to get us our own place that will suit us! (Currently private letting, not ideal! No shower, expensive storage heaters etc etc)

Have a small deposit of just under £6000 saved, but looking into mortgages and I keep getting told the same thing - my debt is too high compared to my income. So rather than trying to scrape by and afford something, I'd rather attempt to fire everything towards the debt just now so I am in a better position for applying for THE big debt aka mortgage, oh the irony haha.

I've been a big CC spender, buy now worry later, then wonder why i have no money at the end of each month. So starting to reign it in. I have issues with spending a lot on food, clothes, random little treats for me and my son. But it all adds up.

I have attempted an SOA and included below!

Statement of Affairs and Personal Balance Sheet

Household Information

Number of adults in household........... 1

Number of children in household......... 1

Number of cars owned.................... 1 (well, don't technically own it obv)

Monthly Income Details[/b]

Monthly income after tax................ 1700

Partners monthly income after tax....... 0

Benefits................................ 696

Other income............................ 500[b]

Total monthly income.................... 2896[/b][b]

Monthly Expense Details[/b]

Mortgage................................ 0

Secured/HP loan repayments.............. 0

Rent.................................... 500

Management charge (leasehold property).. 0

Council tax............................. 100

Electricity............................. 167

Gas..................................... 0

Oil..................................... 0

Water rates............................. 0

Telephone (land line)................... 0

Mobile phone............................ 12

TV Licence.............................. 13

Satellite/Cable TV...................... 14

Internet Services....................... 30

Groceries etc. ......................... 300

Clothing................................ 50

Petrol/diesel........................... 150

Road tax................................ 14

Car Insurance........................... 33

Car maintenance (including MOT)......... 20

Car parking............................. 0

Other travel............................ 0

Childcare/nursery....................... 0

Other child related expenses............ 0

Medical (prescriptions, dentist etc).... 0

Pet insurance/vet bills................. 0

Buildings insurance..................... 0

Contents insurance...................... 0

Life assurance ......................... 83

Other insurance......................... 0

Presents (birthday, christmas etc)...... 50

Haircuts................................ 17

Entertainment........................... 60

Holiday................................. 20

Emergency fund.......................... 10

Spotify................................. 9.99[b]

Total monthly expenses.................. 1652.99[/b]

[b]

Assets[/b]

Cash.................................... 0

House value (Gross)..................... 0

Shares and bonds........................ 0

Car(s).................................. 0

Other assets............................ 0[b]

Total Assets............................ 0[/b]

[b]

No Secured nor Hire Purchase Debts[/b]

[b]Unsecured Debts[/b]

Description....................Debt......Monthly...APR

Car PCP........................10000.....205.4.....0

HSBC...........................2925......75........0

Tesco..........................1105......95........0

Virgin.........................1700......35........0

MBNA...........................1790......50........0

Barclaycard....................2333......80........0[b]

Total unsecured debts..........19853.....540.4.....- [/b]

[b]

Monthly Budget Summary[/b]

Total monthly income.................... 2,896

Expenses (including HP & secured debts). 1,652.99

Available for debt repayments........... 1,243.01

Monthly UNsecured debt repayments....... 540.4[b]

Amount left after debt repayments....... 702.61[/b]

[b]Personal Balance Sheet Summary[/b]

Total assets (things you own)........... 0

Total HP & Secured debt................. -0

Total Unsecured debt.................... -19,853[b]

Net Assets.............................. -19,853[/b]

[i]Created using the SOA calculator at www.LemonFool.co.uk.

Reproduced on Moneysavingexpert with permission, using other browser.[/i][/font]

So credit cards, MBNA, Barclaycard, Tesco and Virgin are not 0%, they are charging interest. Actual percentages I am not sure, some of the cards have multiple 0% offers on them that have ran out at different times. The virgin balance - £1100 of that is actually my mums debt that she is giving me money for each month (the other £600 is my balance and is currently 0%). I'm thinking of clearing the tesco first as it's the smallest and will make me feel better to clear it fast.

Car PCP, guessing the amount, car was about £11000, im paying £205/month for the next 35 months and then assume there will be a balance at the end of roughly £4000 if i want to keep the car. I'll probably not keep it that long. I've only had it 13 months or i would think about getting rid for something cheaper.

During winter I can be paying up to £500 to heat my home (hence my urgency to move into my own place with GCH!), but summer I'm around £40. So I've calculated an average for the year.

Other issue, I pay for mines and my ex husbands life insurance (for my sons benefit, hence i'm still paying for ex!). I'm thinking from looking at others that i'm paying a ridiculous amount for two reasonably healthy mid 30s! The thought of changing it gives me a headache, they don't make these things easy!

Can't think of anything else atm! I just paid off my phone contract early with o2 as they were charging ridiculous amounts, so phone is now mines and I'm now only paying £12/month (last months bill was £73!!!)

Thanks for reading if you've made it here!!

0

Comments

-

Why isn't the deposit showing under assets? If you are paying interest on debts it makes more sense to get those paid off. The life assurance is expensive so I would definitely change that and you could probably reduce the groceries expenditure if just you and 1 child.I’m a Forum Ambassador and I support the Forum Team on the Debt free Wannabe, Budgeting and Banking and Savings and Investment boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.

Save £12k in 2026 Challenge £12000/£2000

365 day 1p Challenge 2026 £667.95/£165

Click on this link for a Statement of Accounts that can be posted on the DebtFree Wannabe board: https://lemonfool.co.uk/financecalculators/soa.php1 -

Oh true, I think because it’s in my ISA for my house deposit I just forgot about it as part of the calculation.

Yes food cost is definitely a big issue with me, lots of ready meals and branded food. I’ve made the switch to Lidl this month but I think I’ll still need to work on it!0 -

Have you done a few months on this soa yet, as in have you done one that you think is doable in the future or you have been doing this budget already. First step of not is a pending diary then its to find out interest rates. Then there's a thing called what's the cost (website) that you can use to forecast what to pay and what happens if you send extra to different cards.ive no idea about car finance so I'll leave that to someone else to advise you but potentially you could pay off 2.5 k in debts if you can keep to the soa or save 2.5 k by Xmas to swap to a car that's bought outright.

Contents insurance is probably a good idea to get as well as potentially you have specific equipment belongings that are not cheaply replaced.

Jan 18 Joint debts 35,213

Mortgage Jan 18- 77224 Jan 26- just under 64k

June 25 Debts in my name were £5170. Now 5178 (Jan 26)

DH debts ?? at a guess £15k1 -

No this is the first month of it! Thank you, I’ll have a look at that website. I definitely think it’s doable to clear a big chunk of my debt like you say. Yes the car is far too expensive, really don’t know why I bought it, it’s eating into my budget big time!NeverendingDMP said:Have you done a few months on this soa yet, as in have you done one that you think is doable in the future or you have been doing this budget already. First step of not is a pending diary then its to find out interest rates. Then there's a thing called what's the cost (website) that you can use to forecast what to pay and what happens if you send extra to different cards.ive no idea about car finance so I'll leave that to someone else to advise you but potentially you could pay off 2.5 k in debts if you can keep to the soa or save 2.5 k by Xmas to swap to a car that's bought outright.

Contents insurance is probably a good idea to get as well as potentially you have specific equipment belongings that are not cheaply replaced.0 -

Sorry it should say spending diary!

The car is dear and is half your debt. Getting rid might cut the debt down really quick. Car finance isn't my area though as I've never had it so see what others can advise ! Presumably you don't get back everything you owe.Jan 18 Joint debts 35,213

Mortgage Jan 18- 77224 Jan 26- just under 64k

June 25 Debts in my name were £5170. Now 5178 (Jan 26)

DH debts ?? at a guess £15k1 -

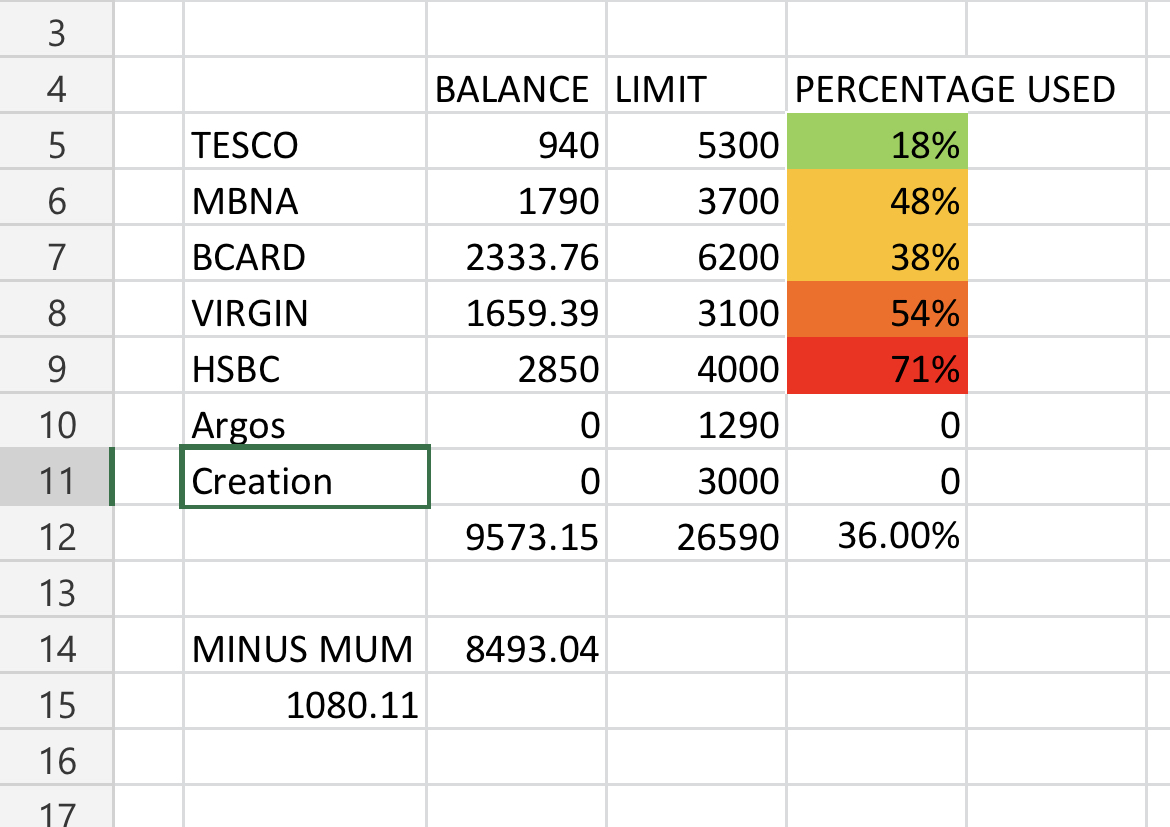

Made some colourful charts on excel to fill in as it definitely helps with the motivation! Once I hit each milestone I colour it in! Next milestone being £8400 balance. Quite happy I’ve got it down from £12500!

Made some colourful charts on excel to fill in as it definitely helps with the motivation! Once I hit each milestone I colour it in! Next milestone being £8400 balance. Quite happy I’ve got it down from £12500! This also shows the balance and limits for each account. I’ve been reading that keeping accounts open with no balance helps keep my credit utilisation number low (36% overall for my cards). But I was also told by a mortgage advisor to close down unused accounts (think I also have a very and PayPal credit account about 2 grand each unused 😑🙄) Not sure what the best advice is, interested to hear thoughts?

This also shows the balance and limits for each account. I’ve been reading that keeping accounts open with no balance helps keep my credit utilisation number low (36% overall for my cards). But I was also told by a mortgage advisor to close down unused accounts (think I also have a very and PayPal credit account about 2 grand each unused 😑🙄) Not sure what the best advice is, interested to hear thoughts? Also finally figured out the exact car balance! 😅 not great but I’m sure if I clear all the credit cards it won’t be so bad to have that alone to worry about!Anyway that’s my little diary update for July. First month this year I haven’t used my credit card on spends or had to borrow money off people to get to next pay day. And I’ve paid a massive chunk into my debts. So feeing good, like I can actually do this!2

Also finally figured out the exact car balance! 😅 not great but I’m sure if I clear all the credit cards it won’t be so bad to have that alone to worry about!Anyway that’s my little diary update for July. First month this year I haven’t used my credit card on spends or had to borrow money off people to get to next pay day. And I’ve paid a massive chunk into my debts. So feeing good, like I can actually do this!2 -

Well done on no cards. Huge achievement on doing that whilst reducing the debt.Jan 18 Joint debts 35,213

Mortgage Jan 18- 77224 Jan 26- just under 64k

June 25 Debts in my name were £5170. Now 5178 (Jan 26)

DH debts ?? at a guess £15k1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.8K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.8K Work, Benefits & Business

- 603.4K Mortgages, Homes & Bills

- 178.2K Life & Family

- 260.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards