We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Annuity’s Becoming More Attractive?

Comments

-

Also you can pass on any pension pot left after drawdown when you die. Currently the tax regime around passing on these pots is very generous, although there is some slow pressure building to change that.FIREDreamer said:If I used my drawdown pot to buy a JL 50% spouse RPI linked annuity I could retire now (annuity is greater than post Sal sac salary) but unfortunately I am struggling with the concept of giving my pot away whilst drawdown may provide higher lifetime income, obvious not guaranteed. It’s a big problem for me, albeit a first world problem.

Also although the much discussed Safe Withdrawal Rates for drawdown are 3 to 4 %, projected scenarios if markets are reasonably kind are that you can take more than that, and/or die with most of the pot still intact/even bigger than when you started.

However as you say, nothing is guaranteed .....0 -

The annuity rate is 3.3% of the drawdown pot, so a bit less than 4%. It’s worthy of consideration though.Albermarle said:

Also you can pass on any pension pot left after drawdown when you die. Currently the tax regime around passing on these pots is very generous, although there is some slow pressure building to change that.FIREDreamer said:If I used my drawdown pot to buy a JL 50% spouse RPI linked annuity I could retire now (annuity is greater than post Sal sac salary) but unfortunately I am struggling with the concept of giving my pot away whilst drawdown may provide higher lifetime income, obvious not guaranteed. It’s a big problem for me, albeit a first world problem.

Also although the much discussed Safe Withdrawal Rates for drawdown are 3 to 4 %, projected scenarios if markets are reasonably kind are that you can take more than that, and/or die with most of the pot still intact/even bigger than when you started.

However as you say, nothing is guaranteed .....

EDIT: no guarantee period0 -

While safe withdrawal rates are typically quoted for 30 years (and 4% only really applies to the US), they are critically dependent on the planning horizon (i.e., longevity) - current projections suggest there is a 10% chance of a 55 year old living to 97 or 99 (male or female) and at 65 to 96 or 98, i.e. the horizon is about 40-45 years for a single 55 year old and 30-35 years for a single 65 year old. For couples, there is roughly a 10% chance of one or other (or both) reaching 100 yo (i.e., horizons of 45 and 35 years at 55 and 65, respectively)FIREDreamer said:

The annuity rate is 3.3% of the drawdown pot, so a bit less than 4%. It’s worthy of consideration though.Albermarle said:

Also you can pass on any pension pot left after drawdown when you die. Currently the tax regime around passing on these pots is very generous, although there is some slow pressure building to change that.FIREDreamer said:If I used my drawdown pot to buy a JL 50% spouse RPI linked annuity I could retire now (annuity is greater than post Sal sac salary) but unfortunately I am struggling with the concept of giving my pot away whilst drawdown may provide higher lifetime income, obvious not guaranteed. It’s a big problem for me, albeit a first world problem.

Also although the much discussed Safe Withdrawal Rates for drawdown are 3 to 4 %, projected scenarios if markets are reasonably kind are that you can take more than that, and/or die with most of the pot still intact/even bigger than when you started.

However as you say, nothing is guaranteed .....

EDIT: no guarantee period

The UK based historical MSWR (in %) at various stock allocations and horizons (data derived from https://www.2020financial.co.uk/pension-drawdown-calculator/ ) are approximately:Planning horizon (years)Stocks (%) 25 30 35 40 4540 2.8 2.5 2.2 2.1 2.060 3.2 2.9 2.6 2.5 2.380 3.4 3.2 3.0 2.8 2.7100 3.6 3.4 3.1 3.0 2.7

Subtract approx. 10 basis points per 20 basis points of feesAdd approx 20 basis points for holding a global portfolio (the results are for a UK portfolio).

Depending on your age and planning horizon (and I'm guessing a bit under 65 based on the annuity rate you've been quoted), the annuity rate may be more or less attractive compared to the drawdown rate.0 -

I will be 60 next year so getting old for FIRE I guess, more FIRN - retire normally!OldScientist said:

While safe withdrawal rates are typically quoted for 30 years (and 4% only really applies to the US), they are critically dependent on the planning horizon (i.e., longevity) - current projections suggest there is a 10% chance of a 55 year old living to 97 or 99 (male or female) and at 65 to 96 or 98, i.e. the horizon is about 40-45 years for a single 55 year old and 30-35 years for a single 65 year old. For couples, there is roughly a 10% chance of one or other (or both) reaching 100 yo (i.e., horizons of 45 and 35 years at 55 and 65, respectively)FIREDreamer said:

The annuity rate is 3.3% of the drawdown pot, so a bit less than 4%. It’s worthy of consideration though.Albermarle said:

Also you can pass on any pension pot left after drawdown when you die. Currently the tax regime around passing on these pots is very generous, although there is some slow pressure building to change that.FIREDreamer said:If I used my drawdown pot to buy a JL 50% spouse RPI linked annuity I could retire now (annuity is greater than post Sal sac salary) but unfortunately I am struggling with the concept of giving my pot away whilst drawdown may provide higher lifetime income, obvious not guaranteed. It’s a big problem for me, albeit a first world problem.

Also although the much discussed Safe Withdrawal Rates for drawdown are 3 to 4 %, projected scenarios if markets are reasonably kind are that you can take more than that, and/or die with most of the pot still intact/even bigger than when you started.

However as you say, nothing is guaranteed .....

EDIT: no guarantee period

The UK based historical MSWR (in %) at various stock allocations and horizons (data derived from https://www.2020financial.co.uk/pension-drawdown-calculator/ ) are approximately:Planning horizon (years)Stocks (%) 25 30 35 40 4540 2.8 2.5 2.2 2.1 2.060 3.2 2.9 2.6 2.5 2.380 3.4 3.2 3.0 2.8 2.7100 3.6 3.4 3.1 3.0 2.7

Subtract approx. 10 basis points per 20 basis points of feesAdd approx 20 basis points for holding a global portfolio (the results are for a UK portfolio).

Depending on your age and planning horizon (and I'm guessing a bit under 65 based on the annuity rate you've been quoted), the annuity rate may be more or less attractive compared to the drawdown rate.

A slightly enhanced annuity rate due to my own minor health issues - hypertension, asthma. Not sure that makes much difference as neither are particularly life threatening and are well managed.

EDIT: I also have a S&S ISA, so have a lot of equity exposure, but my wife would never be able to manage drawdown.0 -

Assuming a 35-40 year planning horizon then, the annuity payout rate is slightly more than the worst historical drawdown case. As others have said, you can just use part of the pot to building a floor of income which means that drawdown becomes less critical and could be variable withdrawals (e.g., a constant percentage of the pot which is slightly easier to manage than inflation adjusted withdrawals) or, possible only required on an ad-hoc basis.FIREDreamer said:

I will be 60 next year so getting old for FIRE I guess, more FIRN - retire normally!OldScientist said:

While safe withdrawal rates are typically quoted for 30 years (and 4% only really applies to the US), they are critically dependent on the planning horizon (i.e., longevity) - current projections suggest there is a 10% chance of a 55 year old living to 97 or 99 (male or female) and at 65 to 96 or 98, i.e. the horizon is about 40-45 years for a single 55 year old and 30-35 years for a single 65 year old. For couples, there is roughly a 10% chance of one or other (or both) reaching 100 yo (i.e., horizons of 45 and 35 years at 55 and 65, respectively)FIREDreamer said:

The annuity rate is 3.3% of the drawdown pot, so a bit less than 4%. It’s worthy of consideration though.Albermarle said:

Also you can pass on any pension pot left after drawdown when you die. Currently the tax regime around passing on these pots is very generous, although there is some slow pressure building to change that.FIREDreamer said:If I used my drawdown pot to buy a JL 50% spouse RPI linked annuity I could retire now (annuity is greater than post Sal sac salary) but unfortunately I am struggling with the concept of giving my pot away whilst drawdown may provide higher lifetime income, obvious not guaranteed. It’s a big problem for me, albeit a first world problem.

Also although the much discussed Safe Withdrawal Rates for drawdown are 3 to 4 %, projected scenarios if markets are reasonably kind are that you can take more than that, and/or die with most of the pot still intact/even bigger than when you started.

However as you say, nothing is guaranteed .....

EDIT: no guarantee period

The UK based historical MSWR (in %) at various stock allocations and horizons (data derived from https://www.2020financial.co.uk/pension-drawdown-calculator/ ) are approximately:Planning horizon (years)Stocks (%) 25 30 35 40 4540 2.8 2.5 2.2 2.1 2.060 3.2 2.9 2.6 2.5 2.380 3.4 3.2 3.0 2.8 2.7100 3.6 3.4 3.1 3.0 2.7

Subtract approx. 10 basis points per 20 basis points of feesAdd approx 20 basis points for holding a global portfolio (the results are for a UK portfolio).

Depending on your age and planning horizon (and I'm guessing a bit under 65 based on the annuity rate you've been quoted), the annuity rate may be more or less attractive compared to the drawdown rate.

A slightly enhanced annuity rate due to my own minor health issues - hypertension, asthma. Not sure that makes much difference as neither are particularly life threatening and are well managed.

EDIT: I also have a S&S ISA, so have a lot of equity exposure, but my wife would never be able to manage drawdown.

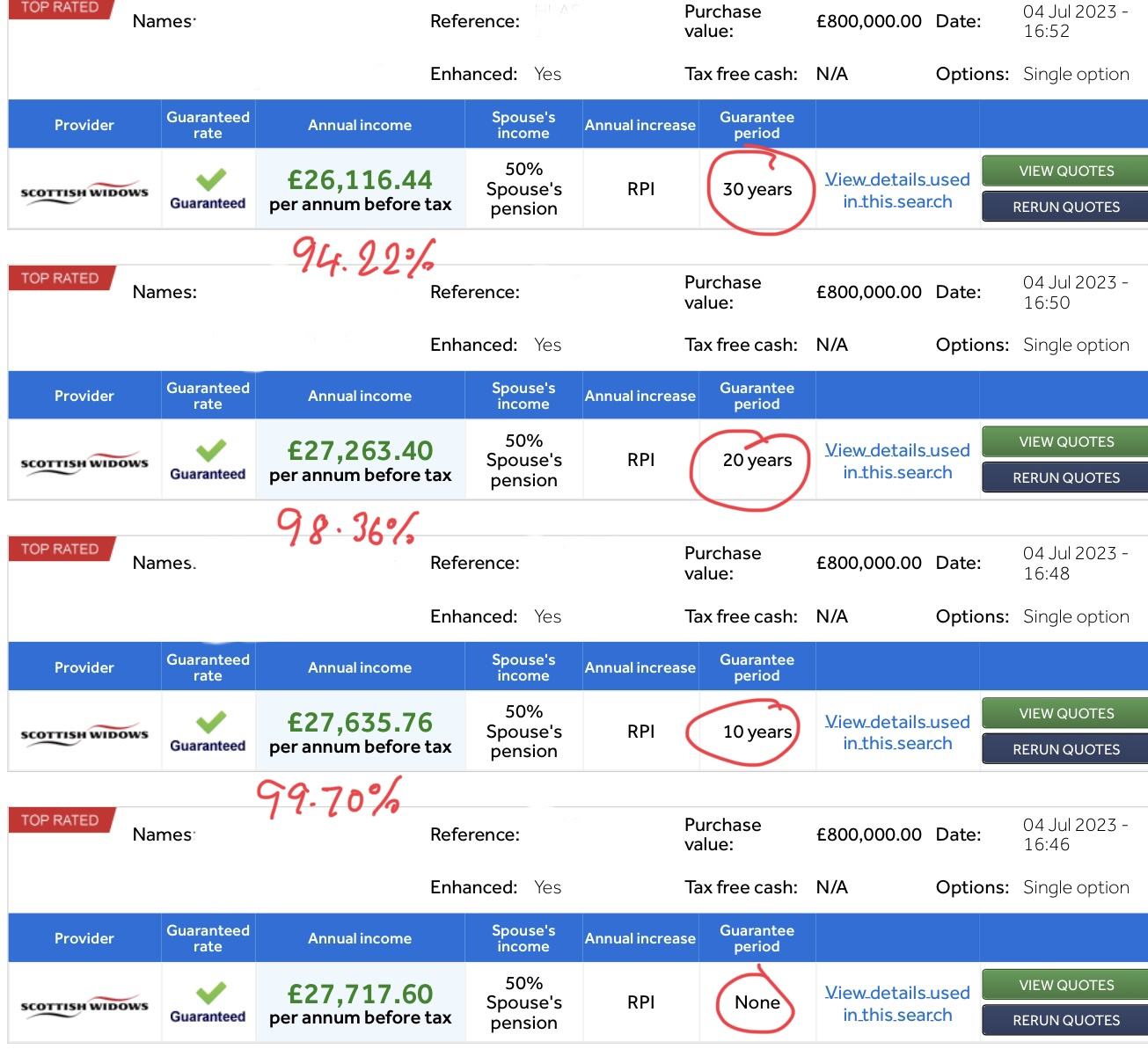

At your age, you might find that adding a 10 (or possibly 15) year guarantee makes very little difference to the payout rate (assuming you have beneficiaries apart from spouse).

0 -

A 20 year guarantee doesn’t cost much, even 30 years only reduces the annuity by 5% obviously my health doesn’t affect my longevity too much.OldScientist said:

Assuming a 35-40 year planning horizon then, the annuity payout rate is slightly more than the worst historical drawdown case. As others have said, you can just use part of the pot to building a floor of income which means that drawdown becomes less critical and could be variable withdrawals (e.g., a constant percentage of the pot which is slightly easier to manage than inflation adjusted withdrawals) or, possible only required on an ad-hoc basis.FIREDreamer said:

I will be 60 next year so getting old for FIRE I guess, more FIRN - retire normally!OldScientist said:

While safe withdrawal rates are typically quoted for 30 years (and 4% only really applies to the US), they are critically dependent on the planning horizon (i.e., longevity) - current projections suggest there is a 10% chance of a 55 year old living to 97 or 99 (male or female) and at 65 to 96 or 98, i.e. the horizon is about 40-45 years for a single 55 year old and 30-35 years for a single 65 year old. For couples, there is roughly a 10% chance of one or other (or both) reaching 100 yo (i.e., horizons of 45 and 35 years at 55 and 65, respectively)FIREDreamer said:

The annuity rate is 3.3% of the drawdown pot, so a bit less than 4%. It’s worthy of consideration though.Albermarle said:

Also you can pass on any pension pot left after drawdown when you die. Currently the tax regime around passing on these pots is very generous, although there is some slow pressure building to change that.FIREDreamer said:If I used my drawdown pot to buy a JL 50% spouse RPI linked annuity I could retire now (annuity is greater than post Sal sac salary) but unfortunately I am struggling with the concept of giving my pot away whilst drawdown may provide higher lifetime income, obvious not guaranteed. It’s a big problem for me, albeit a first world problem.

Also although the much discussed Safe Withdrawal Rates for drawdown are 3 to 4 %, projected scenarios if markets are reasonably kind are that you can take more than that, and/or die with most of the pot still intact/even bigger than when you started.

However as you say, nothing is guaranteed .....

EDIT: no guarantee period

The UK based historical MSWR (in %) at various stock allocations and horizons (data derived from https://www.2020financial.co.uk/pension-drawdown-calculator/ ) are approximately:Planning horizon (years)Stocks (%) 25 30 35 40 4540 2.8 2.5 2.2 2.1 2.060 3.2 2.9 2.6 2.5 2.380 3.4 3.2 3.0 2.8 2.7100 3.6 3.4 3.1 3.0 2.7

Subtract approx. 10 basis points per 20 basis points of feesAdd approx 20 basis points for holding a global portfolio (the results are for a UK portfolio).

Depending on your age and planning horizon (and I'm guessing a bit under 65 based on the annuity rate you've been quoted), the annuity rate may be more or less attractive compared to the drawdown rate.

A slightly enhanced annuity rate due to my own minor health issues - hypertension, asthma. Not sure that makes much difference as neither are particularly life threatening and are well managed.

EDIT: I also have a S&S ISA, so have a lot of equity exposure, but my wife would never be able to manage drawdown.

At your age, you might find that adding a 10 (or possibly 15) year guarantee makes very little difference to the payout rate (assuming you have beneficiaries apart from spouse).

Using a round £800k purchase price … 1

1 -

Rates are quite good.

I'm 60 and the HL calculator shows £27,223 using a £800k pot (my real one is half that), 50% spouse, nil guarantee period. So 3.4%

£24,175 if 100& spouse.0 -

My pot isn’t £800k either, I just put that value in to minimise any fixed policy fees allowed for in the annuity.westv said:Rates are quite good.

I'm 60 and the HL calculator shows £27,223 using a £800k pot (my real one is half that), 50% spouse, nil guarantee period. So 3.4%

£24,175 if 100& spouse.

Using the 4% rule (sic) you get £32,000 pa with no spouse reduction.The annuity option is tempting though.

If the annuity you get from your pot plus any DB is enough for a comfortable retirement, do you leave the table (buy the annuity and relax) or carry on playing (drawdown) and maybe still working and contributing?

How many “one more year”s do you do?0 -

A possibly somewhat trite answer, but one I liked the sound of. Stop playing the game once you've won.FIREDreamer said:

My pot isn’t £800k either, I just put that value in to minimise any fixed policy fees allowed for in the annuity.westv said:Rates are quite good.

I'm 60 and the HL calculator shows £27,223 using a £800k pot (my real one is half that), 50% spouse, nil guarantee period. So 3.4%

£24,175 if 100& spouse.

Using the 4% rule (sic) you get £32,000 pa with no spouse reduction.The annuity option is tempting though.

If the annuity you get from your pot plus any DB is enough for a comfortable retirement, do you leave the table (buy the annuity and relax) or carry on playing (drawdown) and maybe still working and contributing?

How many “one more year”s do you do?"Real knowledge is to know the extent of one's ignorance" - Confucius0 -

As mentioned above, the '4% rule' applied for a 30 year retirement if you were based in the US. Over the last century, the UK has tended to have higher inflation than the US hence, at least partly, why our equivalent 'rule' was more like 3% (for a 30 year horizon) and less than this for longer periods.FIREDreamer said:

My pot isn’t £800k either, I just put that value in to minimise any fixed policy fees allowed for in the annuity.westv said:Rates are quite good.

I'm 60 and the HL calculator shows £27,223 using a £800k pot (my real one is half that), 50% spouse, nil guarantee period. So 3.4%

£24,175 if 100& spouse.

Using the 4% rule (sic) you get £32,000 pa with no spouse reduction.The annuity option is tempting though.

If the annuity you get from your pot plus any DB is enough for a comfortable retirement, do you leave the table (buy the annuity and relax) or carry on playing (drawdown) and maybe still working and contributing?

How many “one more year”s do you do?

If your inflation protected floor, i.e. state pension, DB pensions, and (potentially) annuities is sufficient for your lifestyle requirements, then why not retire?

If you are struggling to purchase an annuity (because it is a large amount of money to potentially 'throw away') in one go there are several alternatives:

1) As discussed above, use a lengthy guarantee period (you or your beneficiaries will get a portion of the money back)

2) Partly annuitise now - if then required, purchase others at later dates (although there are risks with delaying purchase)

One way round the 'only 50%' on death is to purchase two annuities (one each, possibly with different insurance companies) - then the surviving spouse has 75% of the income (assuming purchases of about the same amount) - although a long guarantee period largely obviates the need for this (at least until the guarantee period has expired).

However, complete annuitisation is likely to be unwise too since it leaves nothing for large one-off payments (you might never have to touch the pot, but it is nice to know it is there). FWIW, all our current lifestyle needs are largely satisfied by a DB pension but we still have a drawdown pot for a relatively small amount of discretionary spending together with an emergency fund. Once our state pensions kick in it is unlikely we will need any further drawdown and we can leave the remaining pot to (hopefully) grow for legacy purposes.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards