We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Contracted out - Never Knew!!

Comments

-

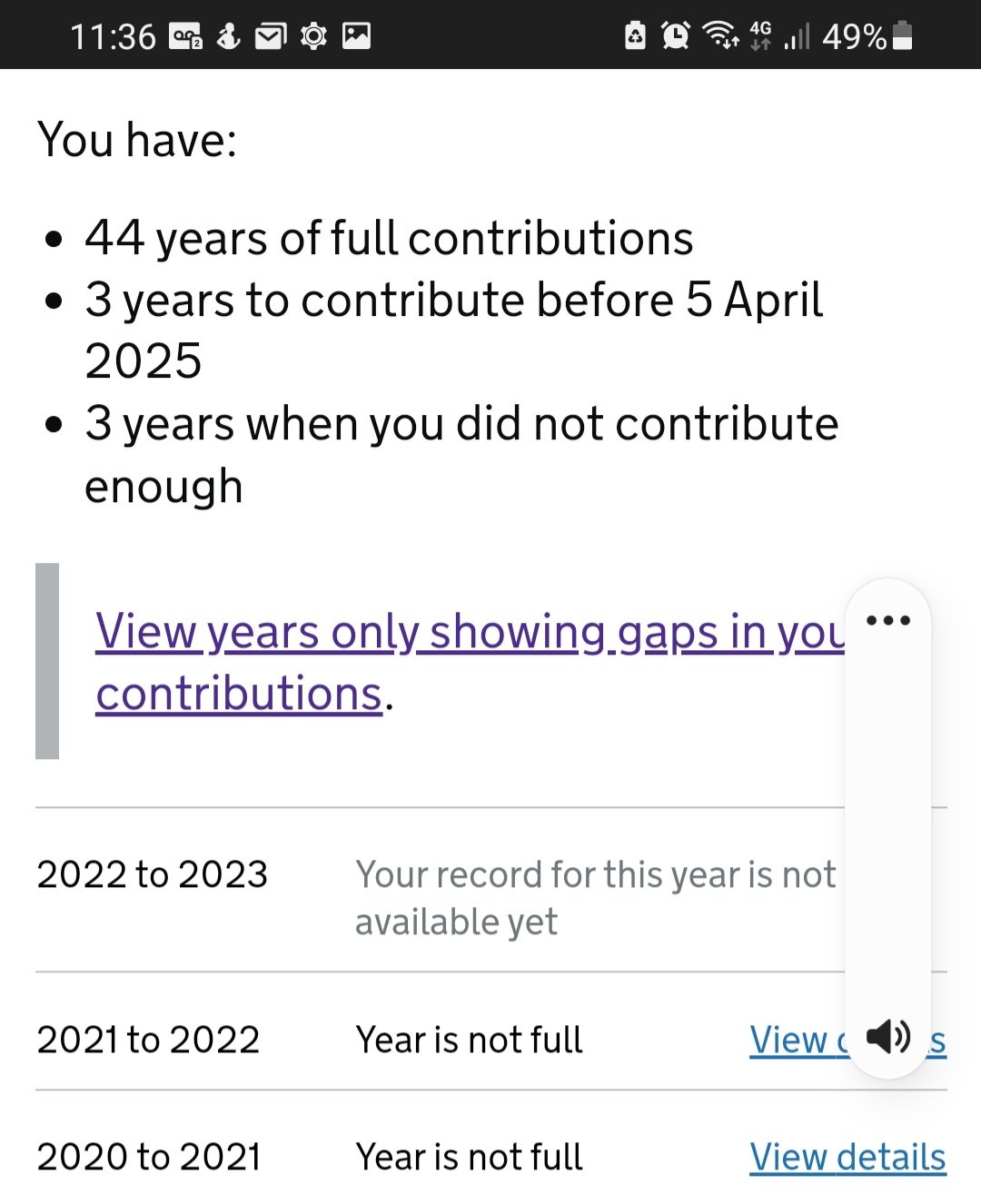

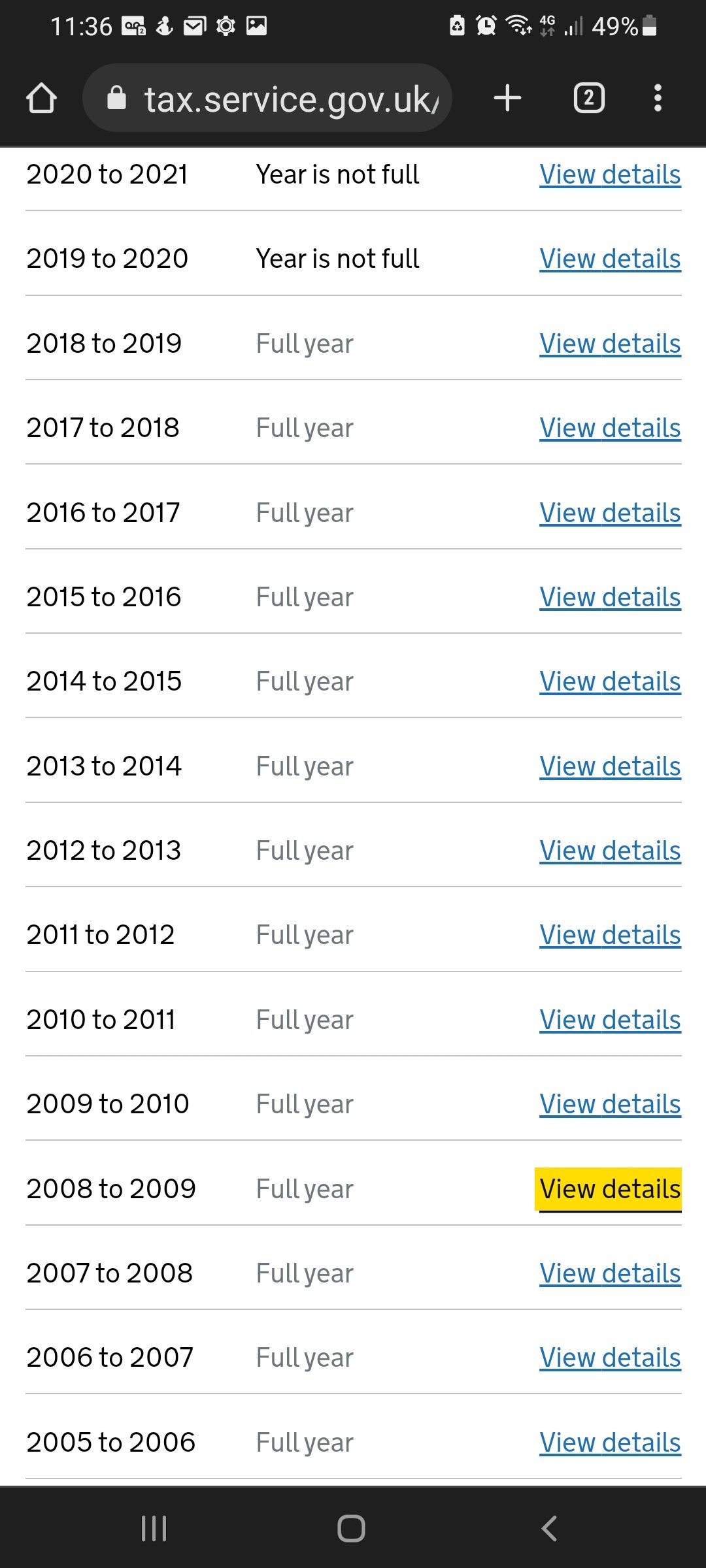

...so just shy of £5000... would that bring me up to full state pension or would it still be short because of contracted out years?pinnks said:As you retired in July 2018, 2017/18 is likely to be partly full, and could be filled for less than the cost of the full year price of, currently £824.20.

You will then be able to fill 2018/19 to 2024/25, though paying 2024/25 will probably not be worth it as it will only add just over £1 per week. 2018/19, 2019/20 and 2022/23 current cost £824.20 per year. 2020/21 costs £795.60 and 2021/22 costs £800.80. 2023/24 costs £907.40. Quite a lot of money but as long as your health (and your pocket!) is good, then payment is just under 3 years into receiving your pension.

If you have grandchildren and care for them, you may qualify for NI credits.0 -

MSE guide - a useful intro.Essentially each new year post 2016 can buy 1/35th of current new state pension.So roughly £6 per week as of Apr. £203.85/35=£5.82 or £302 pa - and that indexed by triple lock most years.For a payment of roughly 3x that amount (c£824 rising to c£907 after Aug 1).It's a really good return - if it buys you that full year. It hasn't always - see the red traffic light warning in avbove link - so do get it confirmed by future pension service etc before parting with cash.Given you have a 10 week forecast to resolve COPE / contracted out corrections - taking you close to end of July deadline - would think you might not want to risk early years (pre 2016).But the retirement years post 2018 - could well be worth it - if it turns out you're still a long way from maximum.Last year I was just c£15pa below max - despite iirc over 12 yrs contracted out in early career - so not a good return on £824 for me - when last checked the forecasts.1

-

I've got 3 yrs contracted out during the time 1987-1990 but I believe that I can't do anything about that so it's just the years on from July 2018 when I retired until 2025 when I receive my SP... therefore I think the deadline date of July 31st doesn't apply to me as that's for pre 2016 I think?0

-

Will have you to wait to hear from dwp and go from there...

0 -

Yes they would all count and might at least give you part credits. Even picking up from school one day a week would count.SINDYGIRL said:I do look after my grandchildren...I have 4 under 6, but only randomly when they're unwell, during school holidays and collecting from school or nursery so I'd imagine that doesn't count.I’d suggest you look into applying for this as it would help you a lot.1 -

If you are looking after the grandchildren whilst the parent is working you can claim for any week where you looked after them for a period of time so well worth doing as that will save you £15 to £17 per week in class 3 contributions reducing your overall outlay.A quick finger in the air calculation shows you should currently have at least £167.82 - £156.18 for 30+ pre 2016 years plus £11.64 for 2 post 2016 years - leaving you £36.03 to make up which is just over 6 more years needed with 6 available - which FY do you retire in ? How many post 2016 years does your record show as full ? Is 18-19 full ?I would also argue that you not buying past years when they were available at their original price was due to the failure of HMRC to accurately maintain your record and you should be allowed to buy them at the original in year price.You may still be a bit short of the max but the payback on VCs is well worth it especially if you can get some granny credits and argue as above.

2 -

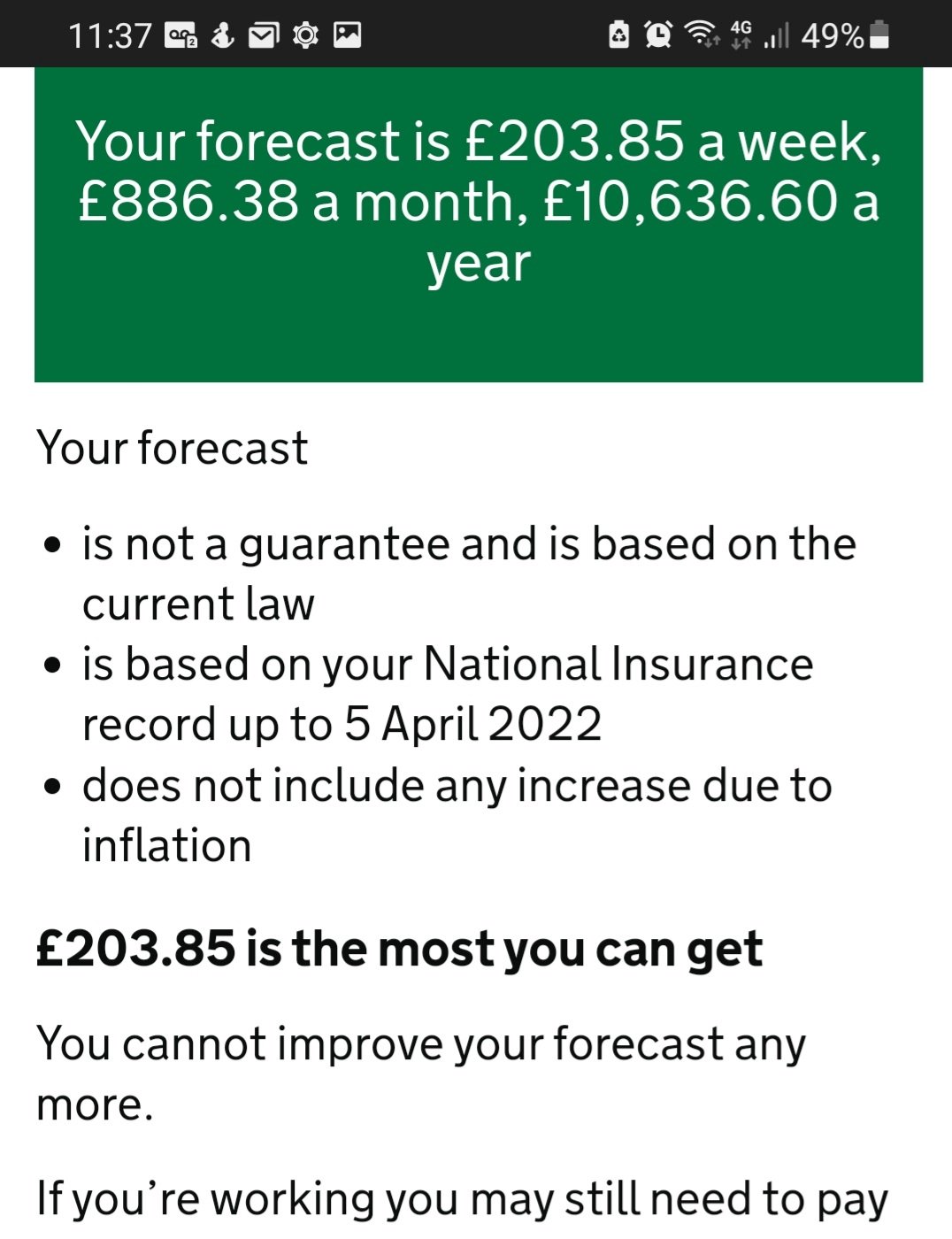

Just done these screenshot from gov.uk... Dwp say the forecast is wrong...

0

0 -

A bit of a bonus then as that should mean you have at least £173.65 leaving £30.20 to go or just over 5 years with 6 years left to get it. You could actually get the max but unlikely the final year would be worth it. You may also have some additional pension pre 2016 which could bring that current amount up - you only need another pound or so to cover the final part year. All you can do now is wait and try to organise the funds to top up when it is all sorted.

1 -

It would bring you up to just shy of the max as paying the final year would add only £1 or so per week, £55 or so per year, meaning the investment of the best part of £1,000 by 2024/25 would never repay itself.SINDYGIRL said:

...so just shy of £5000... would that bring me up to full state pension or would it still be short because of contracted out years?pinnks said:As you retired in July 2018, 2017/18 is likely to be partly full, and could be filled for less than the cost of the full year price of, currently £824.20.

You will then be able to fill 2018/19 to 2024/25, though paying 2024/25 will probably not be worth it as it will only add just over £1 per week. 2018/19, 2019/20 and 2022/23 current cost £824.20 per year. 2020/21 costs £795.60 and 2021/22 costs £800.80. 2023/24 costs £907.40. Quite a lot of money but as long as your health (and your pocket!) is good, then payment is just under 3 years into receiving your pension.

If you have grandchildren and care for them, you may qualify for NI credits.

Your NI record shows that all years 2016/17 to 2018/19 are full, so you would only need to fill (by whatever means) 2019/20 to 2023/24 so that would be just over £4,150 if you have to pay them all and cannot get any credits.

This all assumes that your COPE figure is sufficiently high to mean that your 2016 starting amount is based on the old basic pension amount of £156.20, which is the lowest it can be. Once you have things sorted with DWP it is possible (though I think quite unlikely) that your starting amount is higher than £156.20, meaning one or more of the currently empty years will not need to be filled...1 -

May I ask one last question so I'm right in my head...

Am I going to get a reduced pension because

a) I was contracted out or because

b) I retired in 2018 aged 59 thus not paying anymore NI contributions?

...or is it a combo of both?

Thankyou all in advance0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.7K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.7K Work, Benefits & Business

- 603.2K Mortgages, Homes & Bills

- 178.2K Life & Family

- 260.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards