We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Plan Growth outstanding why?!

chapelhouse123

Posts: 13 Forumite

I’m just fascinated and ever hopeful that this can happen. What I’m trying to find out is, what is this some sort of Covid investment glitch? Or could it happen again?

0

Comments

-

Pretty much anything could happen. That's the nature of investments.

That's Royal London's branding isn't it? You can go to their website and see the historical performance of all their funds: https://www.royallondon.com/pensions/investment-options/fund-prices/.

Taking a look at that info will give you some idea of how much of a departure from normal 2020 - 2021 was.

0 -

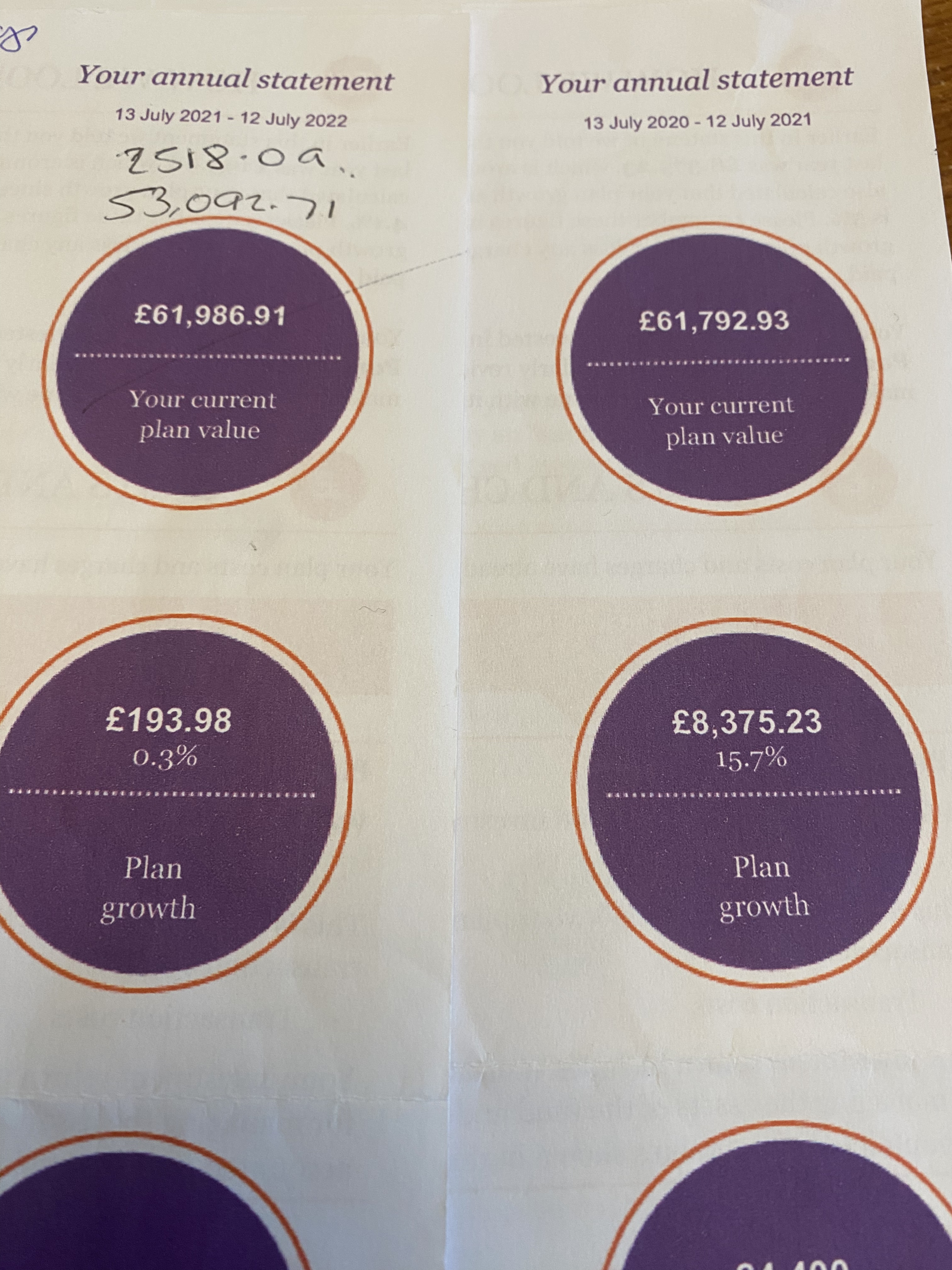

Is the £53,092- todays value?

2022 was not a good year for many investments .Ukraine war did not help but was not the only reason.

However it seems a bit odd that you seem to have suffered a 16% loss from July 2022 to today, but no loss from July 21 to 22, as a lot of the losses in the markets were actually in the first half of 2022.0 -

I’m just fascinated and ever hopeful that this can happen. What I’m trying to find out is, what is this some sort of Covid investment glitch? Or could it happen again?

2021-22 was a poor period and showing any growth is a good outcome (July to Dec 21 was good, then it was all downhill from there until Oct 22).

2020-21 was a good period.

You get good years and bad years. Over the long term, around 1 in 5 years are negative.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

Hi dunstonh. No problem if you don’t want to express an opinion on this.dunstonh said:I’m just fascinated and ever hopeful that this can happen. What I’m trying to find out is, what is this some sort of Covid investment glitch? Or could it happen again?

2021-22 was a poor period and showing any growth is a good outcome (July to Dec 21 was good, then it was all downhill from there until Oct 22).

2020-21 was a good period.

You get good years and bad years. Over the long term, around 1 in 5 years are negative.

What are your ‘expectations’ for the rest of 2023?

My IFA is suggesting things may ‘pick up’ in the second half of this year. Believe his thoughts were mainly based on falling inflation and interest rates.0 -

Some years I have been +30% and others -20%. Then a lot in the middle of that range. No-one can predict the future and it really doesn't matter. Ideally, for those of us not yet retired we want low steady growth with a few crashes for good measure. That changes at the point of retirement however.

0 -

Hi dunstonh. No problem if you don’t want to express an opinion on this.I never give short-term expectations. Its a fool's game if you try. Long term is fair enough as these things tend to revert to mean over the long term. But short term leaves you open to not guessing a Japanese Nuclear station is going to melt down or people will fly planes into the twin towers, or Russia will invade Ukraine.

What are your ‘expectations’ for the rest of 2023?My IFA is suggesting things may ‘pick up’ in the second half of this year. Believe his thoughts were mainly based on falling inflation and interest rates.2022 was a year of repeated knife cuts. Just as one appeared to be healing, along came another. Statistically, most negative periods last less than a quarter. A lesser number last 2 quarters and so on. Also, statistically, there are very few consecutive negative years. They happen but not very often. However, the last one to happen was actually three negative years in a row. So, even if you go with the statistically most likely outcomes, fate will poop on you from a height.

Statistically, after recessionary pressures, the markets become rather stable for a period. The volatility reduces but there is not much in the way of growth. Neither going up or down much but holding steady. Then when the bad news stops coming in as frequently, and more hints of good news begin to appear, it tends to start the recovery. We appear to be that potential stage. However, 2022 had several of those periods before some more bad events occurred and that can happen again (and again). So, statistically, the odds would suggest a recovery is more likely than a negative but who knows.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

Do you have the equivalent statements for 2019/20 and previous years, which will give you a more informed comparison than simply one good year and a neutral one?chapelhouse123 said:I’m just fascinated and ever hopeful that this can happen. What I’m trying to find out is, what is this some sort of Covid investment glitch? Or could it happen again?0 -

Thanks dunstonh,dunstonh said:Hi dunstonh. No problem if you don’t want to express an opinion on this.I never give short-term expectations. Its a fool's game if you try. Long term is fair enough as these things tend to revert to mean over the long term. But short term leaves you open to not guessing a Japanese Nuclear station is going to melt down or people will fly planes into the twin towers, or Russia will invade Ukraine.

What are your ‘expectations’ for the rest of 2023?My IFA is suggesting things may ‘pick up’ in the second half of this year. Believe his thoughts were mainly based on falling inflation and interest rates.2022 was a year of repeated knife cuts. Just as one appeared to be healing, along came another. Statistically, most negative periods last less than a quarter. A lesser number last 2 quarters and so on. Also, statistically, there are very few consecutive negative years. They happen but not very often. However, the last one to happen was actually three negative years in a row. So, even if you go with the statistically most likely outcomes, fate will poop on you from a height.

Statistically, after recessionary pressures, the markets become rather stable for a period. The volatility reduces but there is not much in the way of growth. Neither going up or down much but holding steady. Then when the bad news stops coming in as frequently, and more hints of good news begin to appear, it tends to start the recovery. We appear to be that potential stage. However, 2022 had several of those periods before some more bad events occurred and that can happen again (and again). So, statistically, the odds would suggest a recovery is more likely than a negative but who knows.

As you say it’s all best endeavours to forecast, but literally anything can happen. Expect the unexpected!0 -

My IFA is suggesting things may ‘pick up’ in the second half of this year.His opinion and time comes free to you, or do you pay for this?As you say it’s all best endeavours to forecast, but literally anything can happen.Costs matter when compounded over long periods.0

-

Corrected that for you.Albermarle said:Is the £53,092- todays value?

2022 was not a good year for many investments .Ukraine war Russia's war did not help but was not the only reason.

However it seems a bit odd that you seem to have suffered a 16% loss from July 2022 to today, but no loss from July 21 to 22, as a lot of the losses in the markets were actually in the first half of 2022.

The problem as I see it is that a number of shares became very overheated in the latter part of Covid and have adjusted themselves, including some I hold and that doubled in value (almost) to their pre-Covid value without any real underlying reason for this. These are now a lot more realistically priced, although through 2022 I did 'lose' on these, I don't consider them far outside of the overall forecast that I'd expect.GSP said:

Thanks dunstonh,dunstonh said:Hi dunstonh. No problem if you don’t want to express an opinion on this.I never give short-term expectations. Its a fool's game if you try. Long term is fair enough as these things tend to revert to mean over the long term. But short term leaves you open to not guessing a Japanese Nuclear station is going to melt down or people will fly planes into the twin towers, or Russia will invade Ukraine.

What are your ‘expectations’ for the rest of 2023?My IFA is suggesting things may ‘pick up’ in the second half of this year. Believe his thoughts were mainly based on falling inflation and interest rates.2022 was a year of repeated knife cuts. Just as one appeared to be healing, along came another. Statistically, most negative periods last less than a quarter. A lesser number last 2 quarters and so on. Also, statistically, there are very few consecutive negative years. They happen but not very often. However, the last one to happen was actually three negative years in a row. So, even if you go with the statistically most likely outcomes, fate will poop on you from a height.

Statistically, after recessionary pressures, the markets become rather stable for a period. The volatility reduces but there is not much in the way of growth. Neither going up or down much but holding steady. Then when the bad news stops coming in as frequently, and more hints of good news begin to appear, it tends to start the recovery. We appear to be that potential stage. However, 2022 had several of those periods before some more bad events occurred and that can happen again (and again). So, statistically, the odds would suggest a recovery is more likely than a negative but who knows.

As you say it’s all best endeavours to forecast, but literally anything can happen. Expect the unexpected!

2022 was a really difficult year also as we had a large jump in inflation caused by a variety of factors (many of which were in place before Russia's war in Ukraine began), there has been a huge swing in certain currency pairs through the year and it's been very difficult in general for many companies to plan ahead with recessionary-like conditions even if there hasn't been a recession. As a small group of companies we made the decision to bring certain investments forward while delaying others and I'm not sure, even with a much more detailed understanding of the industries and areas we work in and the current economic effects of those than most, that we have got it completely right.

This year overall looks to be one that could go either way in general for share prices and will be largely dependent on how inflation is controlled generally. Some markets are better than others in this regard.💙💛 💔0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards