We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

USS Retirement Options

Comments

-

One other thing to consider is the risk/likelihood of redundancy impacting any of your plans. If anything this probably is something that supports the idea of a double-transfer as a redundancy could impact your ability to build the IB pot back up.2nd_time_buyer said:

Thanks very much for the reply. Those were pretty much my thoughts. I think it might take me 3 to 4 years to build the pot back up. Then I will have 5 years or so where I am looking at partial retirement and not making contributions. So there are quite a few uncertainties. I am leaning towards risking the double transfer nearer the time.ussdave said:

I'm fairly sure you can do this, but I eventually landed on sticking to the original approach you've gone for. I think purely monetarily the case is thre for a double transfer, but the extra timing stress just didn't seem worth it to me.2nd_time_buyer said:

Has anyone else got any thoughts on whether this would work?2nd_time_buyer said:

That make sense but I am wondering if you could transfer out the whole pot, then only transfer back in the amount required for max lump sum (?). That way you leave the savings in the USS Investment Builder for much longer,FIREmenow said:NickBFS said:

USS do not, afaik, allow you to transfer part of your IB pot to a SIPP. You have to transfer all of it. However, nothing prevents you from continuing to contribute to the IB after you have transferred what was in it (start in the IB from scratch again, as it were).

This is what I will do - more to have the option to use the IB pot to bridge early retirement years without having to take the RB too early. I'll have a think about whether I want to avoid triggering MPAA nearer to the time.

Because you can only transfer the whole pot out, The thing I need to work out is when to transfer the pot out to give it enough time to build up again from zero to the max lump sum I can take with the RB.

Otherwise, I am getting very close to the point where if I need to decide whether to transfer out the whole pot in order to give it time to build back up.

The SIPP platform I was looking at, II, allows partial transfers out. So the only thing I can think that would prevent it would be if the transfer-in to the USS it's treated differently in terms of how the benefits can be used. However, I can't see anything on the website saying that is the case.

Reasons against:

1. Money transferred in will be subject to ongoing management charges (not a big deal if you're planning to just draw it all out again imminently via TFLS).

2. Timings become a bit more complex in terms of making sure you have enough time to transfer out and back in before you draw your pension.

Reasons for:

1. Potentially longer period of your funds remaining in the IB and having reduced/zero fees.3 -

2nd_time_buyer, that is an interesting idea that I had not considered. It might also be a bit too risky/too much hassle for me though.On the info for IFAs pdf, the main things that worries me about transfers in is: "Transfers in to USS are permitted at the discretion of the trustee and are only available to active members of USS"I wonder if they would refuse if, for example, someone had already started asking for retirement calculations at the time of requesting a transfer in? More just on account of how much added work it would create to then be paid out in a short period of time. Or is this like death benefits being paid 'at the discretion of the trustee' but in practice they usually are? Would be interested to hear if anyone has successfully done this, although I think it would be a vanishingly small number of people who would know it was possible and then decide to do it. Thanks for the idea, I will keep mulling it over.I've got another thread going at the moment where I've dug into the funds offered in USS (mainly the Let Me Do It offering) - it has made me consider more the benefits of transferring out in terms of having wider choice and control over the funds in which the pot is invested, considering some funds in USS are made up of actively managed underlying funds that are underperforming their own targets or benchmarks. In the different growth funds, I don't think any have met their target of CPI+x% since launch in 2016. So it's possible that returns in a SIPP will dwarf the difference in fees for transferring out with enough time for it to build up again. There are also some decent cashback offers floating around for transfers into SIPPS which could also cover a good chunk of fees.I'm not at a point of costing all that up though, and I know I will definitely need some of the money out if I want to retire early as I have no other DC pensions, and will probably just use up the personal allowance, keeping it mostly tax-free. Salary sacrifice means I'm chucking in as much as I can at the moment. I'm also interested in using some of the transferred out funds in small pots in early retirement to avoid triggering MPAA in case I decide to work again. In my case, lots to weigh against saving some 20% tax (unlikely I'll be a higher tax-payer in retirement). Thanks for bringing all these thoughts to the surface!Can I ask what assumptions you used to estimate how many years you will need to build your pot back up if you transfer it all out?I find these threads really helpful for thinking about all the different angles on USS (including my occassional day dream about defecting to the civil service if they start mucking about with our benefits again)!

0 -

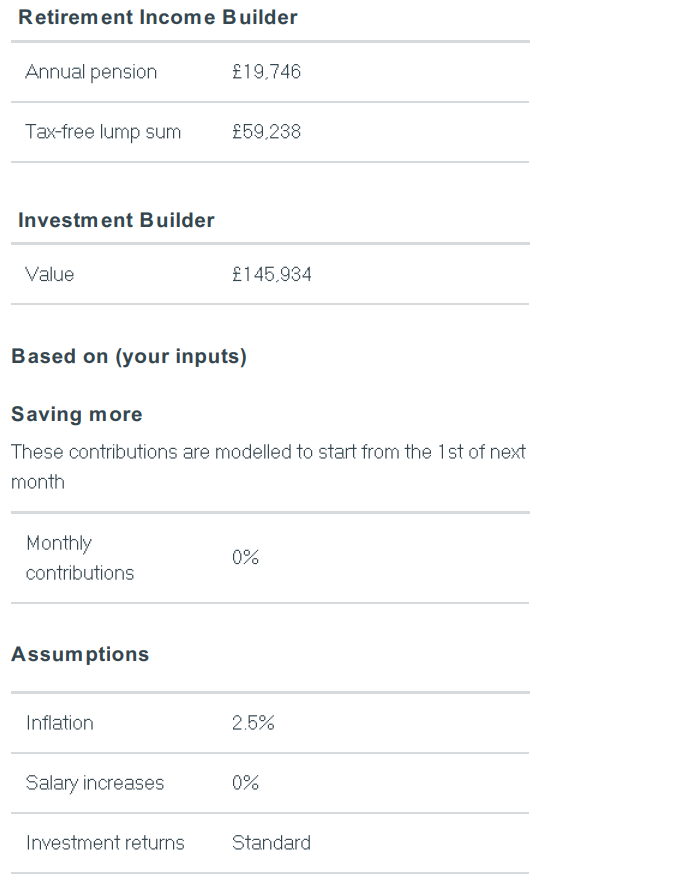

Is there still anyone here? @ussdave @MPLMPL @NickBFS @2nd_time_buyer @gwt1965 @FIREmenow @Cornish_mumAs discussed with a couple of established figures on this forum, I have played with the Benefit Calculator in my USS account. All makes sense regarding the magic number of 6.667 of DB for total Max TFLS. There is one thing I don't understand, that is why my projected RIB annual pension is a bit different from the Annual pension from DB when I take out benefits and savings together. Is that because this increase comes from the IB that I have accumulated?.This is the figure if I stop putting more in IB from now on (I reduced my contribution gradually and still see that even when the future contribution is 0% it is still this number - YET NOW I DOUBT IF IT IS RIGHT, as I know that my IB pot today is only above 40K, how come it becomes 145,934 just by investing - perhaps this Benefit Calculator is still not updated and still add in IB pot from anything above gross salary of 40K - I will need to come back to this again after the change is in place, meaning only the part of one's gross salary obove 70K can be automatically put in IB)

But when I choose to take out both benefits and savings, instead of having an annual pension of the same as the 19,764 RIB figure above I got higher annual pension of 22,541 (with no IB pot left)

But when I choose to take out both benefits and savings, instead of having an annual pension of the same as the 19,764 RIB figure above I got higher annual pension of 22,541 (with no IB pot left) When I try to increase future contribution to IB from 0% to 1% the RIB pot is still 19,764 (understandably) but when I take out both benefits and savings, the annual pension increase once more to 22,762/year (with 8.7K left in IB to keep invested). And yes YAY 22,762* 6.667 magic number it equals about the max TFLS below.

When I try to increase future contribution to IB from 0% to 1% the RIB pot is still 19,764 (understandably) but when I take out both benefits and savings, the annual pension increase once more to 22,762/year (with 8.7K left in IB to keep invested). And yes YAY 22,762* 6.667 magic number it equals about the max TFLS below. From this, if I increase my future contribution to 6%, 7%, or 20%, when I take out the benefits and savings it is still always annual pension at 22,762/year as above, just bigger IB pot left to invest.So I can see if I wish to use money for other types of investments I can just contribute 1% only in the IB pot (knowing it will be not tax efficient or NI efficient) I only have volunteer contribution of 1% and still get the max annual pension of 22,762/year and max TFLS of 151,747.

From this, if I increase my future contribution to 6%, 7%, or 20%, when I take out the benefits and savings it is still always annual pension at 22,762/year as above, just bigger IB pot left to invest.So I can see if I wish to use money for other types of investments I can just contribute 1% only in the IB pot (knowing it will be not tax efficient or NI efficient) I only have volunteer contribution of 1% and still get the max annual pension of 22,762/year and max TFLS of 151,747.

I just wonder how the projected RIB annual pension of 19,746 can increase to over 22.5K when I take both benefits and savings together at retirement. I thought that figure of 19,746 is fixed. And this method means I do not use any IB to buy extra annuity. Anyone having any idea? THank you.0 -

If I’m understanding what you’re asking correctly, I think the annual pension increases because the calculator is commuting all IB money to annual pension. Hence why you have no IB pot left.Apparently we should have a new up to date calculator from tomorrow!1

-

Don't forget either that current assumption in the calculator is that anything above 40K goes to the IB rather than the RIB. Therefore, if your salary is higher than this, your (and the employer's) contributions above that threshold will go into the IB. That is no longer true from now onwards (threshold goes up to circa 70K) but the calculator still functions under old rules (until tomorrow).1

-

gwt1965 said:If I’m understanding what you’re asking correctly, I think the annual pension increases because the calculator is commuting all IB money to annual pension. Hence why you have no IB pot left.Apparently we should have a new up to date calculator from tomorrow!Thank you gwt1965. Oh yes silly me. That's right. I thought my IB all went out in the TFLS but I was wrong, only 150,273-3*22,541=82,650 of the TFLS is from the IB pot. That means 145,934-82,650=63,284 from the IB pot has been commuted to annual pension (to make that increase in annual pension, like buying annuity).Right, I thought I did not want to commute the IB to annual pension because it's been said somewhere here that the commute rate is not very good.Do you know which option I should choose (Take all savings vs Take all benefits - i guess "take all savings"???) to see the calculation for NOT COMMUTING IB to pension? Many thanks.0

-

NickBFS said:Don't forget either that current assumption in the calculator is that anything above 40K goes to the IB rather than the RIB. Therefore, if your salary is higher than this, your (and the employer's) contributions above that threshold will go into the IB. That is no longer true from now onwards (threshold goes up to circa 70K) but the calculator still functions under old rules (until tomorrow).

Thank you NickBFS. Yes you're right, the calculator still assumes anything over 40K will go to IB pot. When it is updated I will see the change (so all of my salary will be used to calculate what's goes to DB, because it's over 40K but under 70K). I will try the tool again after tomorrow. Thanks.

0 -

Wow as we speak the calculator has been updated!!!!!

1 -

So, with the updated calculator I can see the IB pot will be smaller whilst the RIB is much bigger (since all my salary now goes to RIB - the RIB in the new tool is updated to 24,559, rather than 19,746 with the old mechanism, where only the salary under 40K goes there. Well done the union for pension fight to get this deal after the terrible change from Apr 2022. I hope this deal lasts.I first tried the same middle option - Take all savings and benefits, I put in future volunteer contribution just enough to cover 3.667 times the DB - so when I take it the annual pension is about the same as projected RIB and ALL IB pot goes to TFLS).AsI said above that I wanted to see an option not commuting IB (because the rate is said to be not good), I tried the other two options:Take only DB: annual pension goes down from 24,559 down to 20,606 (TFLS still 6.667 times this 20,606). I guess this means I still have all of my IB pot untouched and kept invested ?? (not going out to TFLS OR commuted to pension). Am just a bit surprised thinking I should still have an annual pension of 24,559 (I guess some of that goes in to make Max TFLS??)Take only DC: I don't know why someone would take this option and not taking out DB - Perhaps it just means the person takes 24,559 annual pension as it is but this tool shows how the IB pot can be invested further, or used to buy annuity as I can see those sub-options coming out at the next step.Can anyone confirm what is the best or most popular option here: Take only DB, Take all savings and benefits, or Take onlyDC? I guess it depends on people's pots and what an individual wants (max the TFLS, how much to keep investing, or certainty of annual pension for life) but as I don't understand the implications of each option well yet I am still not sure. I only remember it is said here in the forum before that it is max TFLS if DC and DB are taken out together.

0 -

Ooh. Will have to try it out when I'm home.

I'm glad you've had your question answered. I think I'd choose take all savings, assuming anything left over goes into a separate pot for UFPLS.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 248K Work, Benefits & Business

- 605.2K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards