We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Are we expecting BOE to remain at 4.75% on 8th February 2025?

Comments

-

It could be beneficial to research how the economy was doing when Thatcher won the first of her general elections as a party leader.littleteapot said:

I'm also suprised that growth isn't consistently negative. I don't know whether the figures are being massaged in some way.MattMattMattUK said:

It is far from great, but considering the impact of the pandemic, Brexit and the general economic mismanagement of the last 25 years we are probably lucky it not consistently negative.Strummer22 said:

Agreed, but the BoE have consistently reiterated the 'higher for longer' rhetoric and a rise this month coupled with a (nearly) guaranteed rise next month would give them justification for this - at least, in their eyes.sevenhills said:Strummer22 said:Based on today's inflation figure coming in higher than predicted, the first cut won't be until May at the earliest.One month's inflation figure is not that important.RPI inflation = Dec 2023 - 5.3% down from the previous month's figure of 5.2%

The fact is, inflation will probably still fall below 2% by April or May. The lag from rate changes is so long that just the expectation that this will happen should result in rate reductions soon, in order for those rate reductions to actually have some effect this year. The BoE is scared of getting it wrong again and will end up unnecessarily stifling economic growth. Yes, we may still avoid recession and the economy has been fairly resilient. But growth bobbing around 0% isn't great, is it?

I thought the mismanagement of the economy started with Maggie Thatcher, decimating the mining and manufacturing industries. That puts it nearer 45 years than 25...

Obviously everyone has their own views when it comes to management of the economy, however it's pretty wild to argue she triggered mismanagement of the economy!

1 -

I'd say it's pretty revealing that the graph shows there are only two brief occasions where spending has been less than revenue collected for half a century. That can be pinned on all politicians that have had a chance to influence it, the civil service and the general populace, whose expectation of what the 'government' should spend (our) money on is generally far too great. With no comprehension of the ramifications, see the last part of the chart.

I personally don't feel we'll see a move from the BoE until the Fed moves first, or they know that the Fed will move. National debt is so high now that in my view these matters are now only nominally in our gift to control.0 -

Altior said:I'd say it's pretty revealing that the graph shows there are only two brief occasions where spending has been less than revenue collected for half a century.There must surely be some error in the figures for the gap between spending and revenue to be such a constant.Add to that the cost of the interest on the debt, I don't believe that we can blame anyone, except the politicians.

0 -

sevenhills said:Altior said:I'd say it's pretty revealing that the graph shows there are only two brief occasions where spending has been less than revenue collected for half a century.There must surely be some error in the figures for the gap between spending and revenue to be such a constant.Add to that the cost of the interest on the debt, I don't believe that we can blame anyone, except the politicians.

That's lifted from HoC official publications. The difference is adding to the now unbelievably vast, still climbing public debt.

We get the politicians we deserve. As any politician attempting to get elected on a mandate of only spending what was received in tax revenue simply wouldn't get elected. As I've alluded to, the general assumption now is if anyone experiences difficulties, 'the government' (ie other taxpayers) should pay. We witnessed that mindset only quite recently with apparently serious people debating the realistic prospect of private mortgage bailouts!

2 -

Where is the UK economy going..........

[spoiler alert: the large developed/developing economies suffer from low productivity/high asset prices due to excess debt created to try and artificially juice GDP]

Did the monetary and fiscal stimulus of 2020/21 create any lasting impact of higher employment?

Let's see.......

Employment, marginal change is declining and now turning negative. Less jobs = less confidence = slower spending (velocity of money) = lower GDP

In order to create confidence in an economy, people need jobs. You can increase productivity all you want but if those gains go to shareholders, then the wider economy does not benefit since the wealthy have a tendency to hoard wealth and not spend it.

And in order to avoid inflation, supply needs to be increased at the same time demand increases. So, the Tory idea of tax cuts in order to stimulate demand will only work if they get more people into more jobs.

But look at how low the unemployment rate is......

On a macro level, people are already employed (many have 2 jobs). [it's why govts want to increase immigration despite saying they don't]. There aren't enough additional people who want to work to add to employment.

And so if so many people are already employed why are we as a country facing this issue? Why, if employment is so high and with so much fiscal and monetary stimulus, is GDP not rising?

You could ask, where is all the money going?

Well, if you tie a monkey to a machine it doesn't matter how many nuts you throw at it, it can only work so fast. Those extra nuts will lie on the floor wasting. Or they will be picked up and placed in unproductive means; e.g. property speculation.

In short, cutting interest rates and increasing deficits is only of use if you have idle capacity. The UK doesn't. Nor does the US.

So, at this stage we are at, if stimulus gives money to the working classes it will create goods and services inflation. If stimulus is done by giving more money to the wealthy it will create asset inflation.To solve inequality and failing productivity, cap leverage allowed to be used in property transactions. This lowers the ROI on housing, reduces monetary demand for housing, reduces house prices bringing them more into line with wage growth as opposed to debt expansion.

Reduce stamp duty on new builds and increase stamp duty on pre-existing property.

No-one should have control of setting interest rates since it only adds to uncertainty. Let the markets price yields, credit and labour.1 -

The only reason there is an advance in living standards *for all* is productivity. Even if you get more people into work, that would only benefit those people, unless you have a policy of redistribution from the have to the have-nots. And the UK doesn't.

The post above talks about an increase in GDP, not GDP per capita. GDP can be increased through extra resources e.g. workers, but GDP/capita only through productivity.

Productivity and innovation only comes through time. Unfortunately the political system of re-election every 5 years means government is unwilling to wait. So to speed things up, it uses debt to stimulate. Either its own debt or by reducing rates (yes, BoE controls rates - but has the same agenda - please don't say 2% inflation is its target) and encouraging people into debt.

But debt only brings consumption forward from the future. More debt now = more spending now = less spending in future (unless you create even more debt over and above the debt which needs to be repaid from the last time.

Perhaps we should all just try and be comfortable with the life we have. Perhaps we can find pleasure and fulfilment from the people around us as opposed to a bigger house, shiny car or images on social media.......just an idea.To solve inequality and failing productivity, cap leverage allowed to be used in property transactions. This lowers the ROI on housing, reduces monetary demand for housing, reduces house prices bringing them more into line with wage growth as opposed to debt expansion.

Reduce stamp duty on new builds and increase stamp duty on pre-existing property.

No-one should have control of setting interest rates since it only adds to uncertainty. Let the markets price yields, credit and labour.1 -

I see mortgage data was released today.....and net lending was negative; i.e. the level of outstanding mortgage debt decreased.

The following chart shows a clear relationship between house prices and the change in mortgage debt. House prices are positively correlated with mortgage debt. No surprise for most us.

But stepping back and thinking about what that implies......

Higher house prices require each house buyer to borrow more than the seller. And so on an aggregate basis for this to continue ad infinitum, if the debt burden of mortgages is not to increase, wages must at least match the increase in house prices.......

Over the past year, there has been a significant gap opening up with wage growth materially higher than house price growth.

So why then is outstanding mortgage debt not rising if housing is relatively more affordable than last year?......

The answer of course lies in the path of interest rates.......the benefit from higher wages is more than lost from the rise in the cost of servicing outstanding mortgage debt. Just look at how fast the cost of outstanding mortgages is rising shown in the chart below........imagine if house prices were growing at the same time.

Even if mortgage rates comes down, people in the UK refinance every 2-5 years which means as time passes the interest burden shown in the chart above will rise even as mortgage rates come down. The below chart shows the BBA mortgage rate at 8%. Remember first time buyers who support the market come in with little equity and so face higher rates than those with higher equity.

So on the one hand in order to support house prices, the BoE needs to cut rates significantly but, as outlined in my earlier post above today, without raising employment, additional monetary stimulus only serves to raise asset prices and does not create a permanent increase in GDP.

What will the BoE do? Cut rates in order to stimulate debt knowing the country does not have the idle resources to increase supply? Thereby knowingly only supporting house prices.

Or leave rates where they are knowing this will cause a fall in real-terms house prices (unless there is a fiscal stimulus)?

If there is both a monetary and fiscal stimulus with the current high levels of employment and wage growth I see both rising asset prices and goods and services inflation staying above 2% and potentially rising.

To solve inequality and failing productivity, cap leverage allowed to be used in property transactions. This lowers the ROI on housing, reduces monetary demand for housing, reduces house prices bringing them more into line with wage growth as opposed to debt expansion.

Reduce stamp duty on new builds and increase stamp duty on pre-existing property.

No-one should have control of setting interest rates since it only adds to uncertainty. Let the markets price yields, credit and labour.0 -

lojo1000 said:But debt only brings consumption forward from the future. More debt now = more spending now = less spending in future (unless you create even more debt over and above the debt which needs to be repaid from the last time.

Perhaps we should all just try and be comfortable with the life we have. Perhaps we can find pleasure and fulfilment from the people around us as opposed to a bigger house, shiny car or images on social media.......just an idea.Just looking at the government's debt payments, the debt payments over two years from 2020-2022 cost the Government £101 billion, which is roughly the same amount it spends on education in one year. That is a massive amount and the debt repayments were even higher in 2023.Not sure why the payment swung so widely, from £20 billion in one quarter to £6 billion only a few quarters later.Most people's mortgages are fixed, but certainly don't move so much.

0 -

sevenhills said:lojo1000 said:But debt only brings consumption forward from the future. More debt now = more spending now = less spending in future (unless you create even more debt over and above the debt which needs to be repaid from the last time.

Perhaps we should all just try and be comfortable with the life we have. Perhaps we can find pleasure and fulfilment from the people around us as opposed to a bigger house, shiny car or images on social media.......just an idea.Just looking at the government's debt payments, the debt payments over two years from 2020-2022 cost the Government £101 billion, which is roughly the same amount it spends on education in one year. That is a massive amount and the debt repayments were even higher in 2023.Not sure why the payment swung so widely, from £20 billion in one quarter to £6 billion only a few quarters later.Most people's mortgages are fixed, but certainly don't move so much.

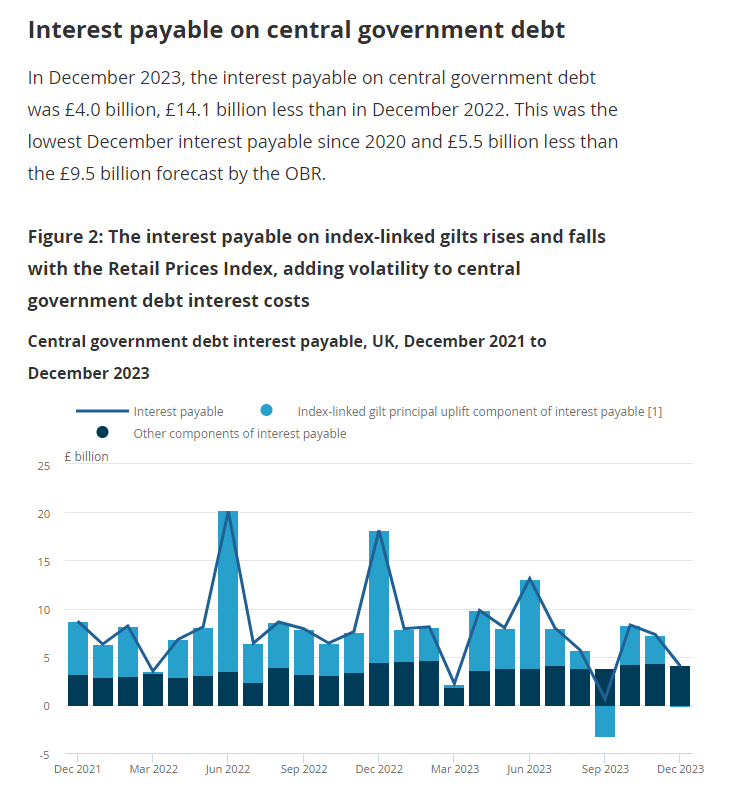

"Figure 2: The interest payable on index-linked gilts rises and falls with the Retail Prices Index, adding volatility to central government debt interest cost"

To solve inequality and failing productivity, cap leverage allowed to be used in property transactions. This lowers the ROI on housing, reduces monetary demand for housing, reduces house prices bringing them more into line with wage growth as opposed to debt expansion.

Reduce stamp duty on new builds and increase stamp duty on pre-existing property.

No-one should have control of setting interest rates since it only adds to uncertainty. Let the markets price yields, credit and labour.0 -

lojo1000 said:"Figure 2: The interest payable on index-linked gilts rises and falls with the Retail Prices Index, adding volatility to central government debt interest cost"

Do the inflation rates vary so wildly, just a quirk of how it's measured, I guess.

0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards