We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Can civil service partnership pension be a good idea sometimes?

Comments

-

I seem to have derailed things by saying it was salary sacrifice, I didn’t understand the difference. It still is pretty good getting 40% tax relief though.So I have very little outside of tax shelters but probably a few hundred interest and no other income.So in my example of 70,000 income do I need to work out what my take home pay will be then work out what percentage of that 16,000 would be, which is then grossed up by 25% to 20,000? After that I then need to contact HMRC to notify them I am contributing to the pension and should get further tax relief? I also wouldn’t need to do self assessment? I have only previously done it for the high income child benefit charge.0

-

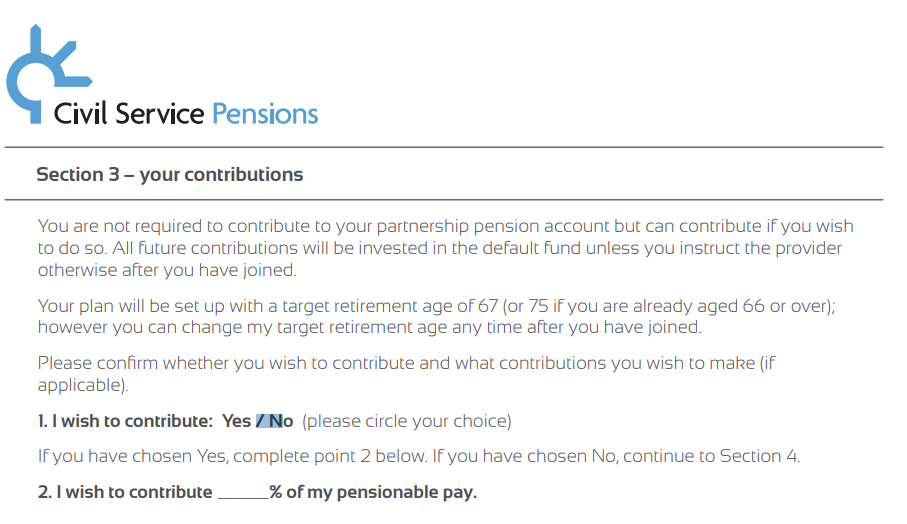

Where are you getting this take home pay stuff from? The application form asks :

No need to contact HMRC re. AVC contributions, your payroll takes care of everything through PAYE. Inform HMRC re. Partnership contributions, as D+C has detailed earlier in thread, with an in-year coding notice adjustment being easiest (I think you need to call them, at least to set it up initially, as it isn't an option in manage your tax online).

AVC:

Partnership:

1 -

Thanks. I had phoned someone in CSP. last week and they told me I had to work out give my percentage I wanted to contribute from my pay after tax as it was different to my current AVC’s but I am taking it that this was wrong?hugheskevi said:Where are you getting this take home pay stuff from? The application form asks :

No need to contact HMRC re. AVC contributions, your payroll takes care of everything through PAYE. Inform HMRC re. Partnership contributions, as D+C has detailed earlier in thread, with an in-year coding notice adjustment being easiest (I think you need to call them, at least to set it up initially, as it isn't an option in manage your tax online).

AVC:

Partnership:So if I earned 70,000 and said I want to contribute 30% of my pensionable earnings will that reduce my adjusted income to 49,000? Do they work it back from that as they would take much less then I would get some relief at source tax relief and have to notify HMRC about the rest?My AVC’s are much simpler as I can just email someone and tell them how much I want to pay in any given month which is what I gave done previously as I usually had to amend it a few times a year to get my adjusted income to 50k.Sorry for all the questions but I seem to have been given a dodgy steer initially or else I took them up wrong which is also entirely possible as this can get confusing.0 -

It is best to never call MyCSP or HMRC in regard to pensions, you can't rely on the responses being accurate. Use email or an old-fashioned letter, written responses will usually be far more accurate.Thanks. I had phoned someone in CSP. last week and they told me I had to work out give my percentage I wanted to contribute from my pay after tax as it was different to my current AVC’s but I am taking it that this was wrong?

In principle, yes, but you need to take into account other relevant income of course and in particular bonuses.So if I earned 70,000 and said I want to contribute 30% of my pensionable earnings will that reduce my adjusted income to 49,000? Do they work it back from that as they would take much less then I would get some relief at source tax relief and have to notify HMRC about the rest?

To continue the example, if you said 30% of £70,000 then your payroll would deduct £16,800 and send that to Legal and General, who would gross it up to £21,000.

You need to ensure your tax position is accurate with HMRC, which is most easily done through amending Tax Coding notice.1 -

Thanks, I understand the part about ensuring I count all income sources.hugheskevi said:

It is best to never call MyCSP or HMRC in regard to pensions, you can't rely on the responses being accurate. Use email or an old-fashioned letter, written responses will usually be far more accurate.Thanks. I had phoned someone in CSP. last week and they told me I had to work out give my percentage I wanted to contribute from my pay after tax as it was different to my current AVC’s but I am taking it that this was wrong?

In principle, yes, but you need to take into account other relevant income of course and in particular bonuses.So if I earned 70,000 and said I want to contribute 30% of my pensionable earnings will that reduce my adjusted income to 49,000? Do they work it back from that as they would take much less then I would get some relief at source tax relief and have to notify HMRC about the rest?

To continue the example, if you said 30% of £70,000 then your payroll would deduct £16,800 and send that to Legal and General, who would gross it up to £21,000.

You need to ensure your tax position is accurate with HMRC, which is most easily done through amending Tax Coding notice.Would you suggest writing to HMRC to amend tax coding or is there a particular form or section in my online HMRC account? How often should I tell HMRC about my pension contributions which require higher rate tax relief?0 -

Log in to online tax portal, PAYE section, check everything is okay, then call them to ask them to add in a Relief at Source pension contribution, giving them the amount. They can do that their end at it will show in online tax portal within a day or two.Fphelp123 said:Thanks, I understand the part about ensuring I count all income sources.Would you suggest writing to HMRC to amend tax coding or is there a particular form or section in my online HMRC account? How often should I tell HMRC about my pension contributions which require higher rate tax relief?

I'd suggest only bothering to amend it twice a year - once at the start of the year (ie estimates), and once near the end of the tax year (ie outturn, as everything should be known by this time barring any unexpected income close to end of financial year) but in time for payroll to implement a change in March payroll, so around the end of January to ensure there is a lot of time.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards