We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

What would you do

hippocrates1

Posts: 354 Forumite

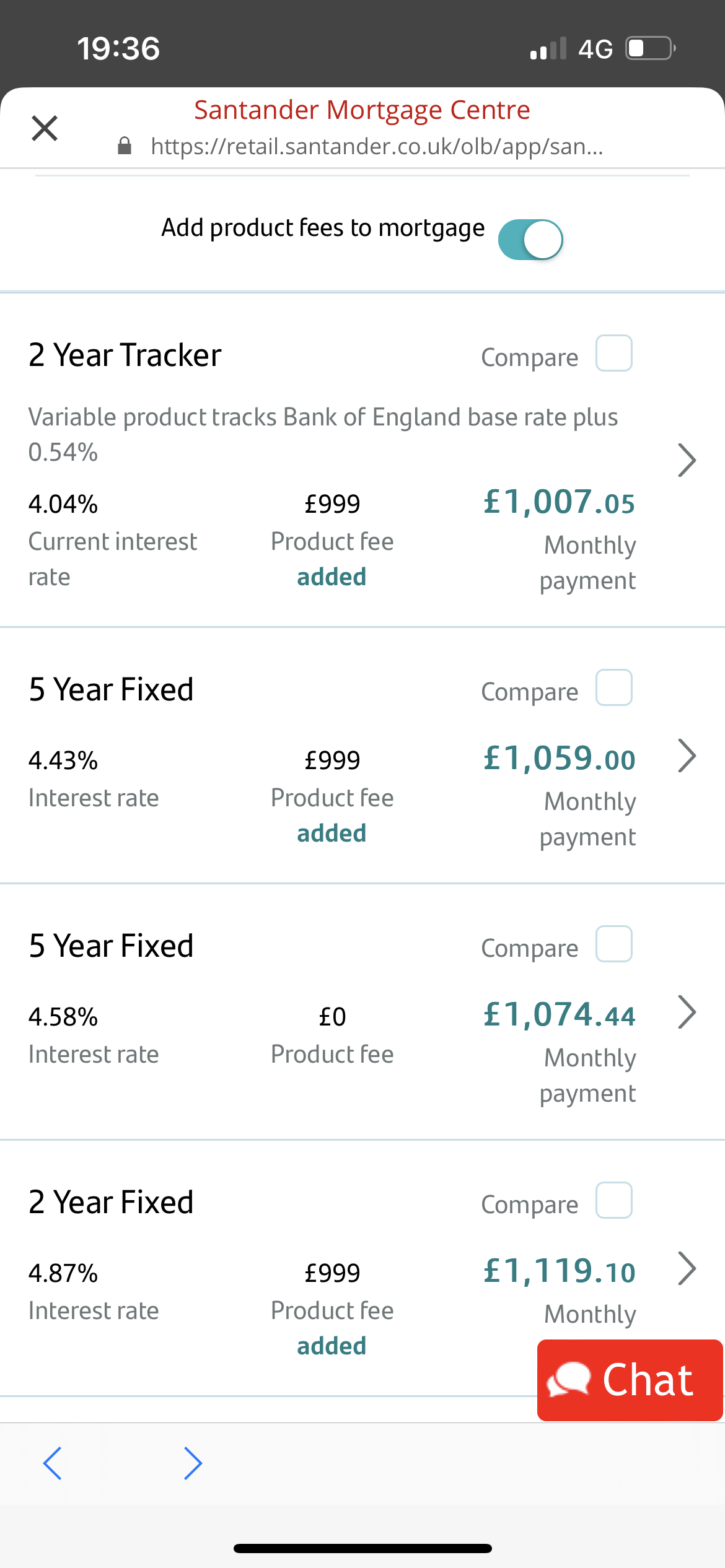

Coming up to the end of a 2 year fix taken out June 21.

Current mortgage is £906 per month. Bought with 10% deposit.

I have a few questions.

Current mortgage is £906 per month. Bought with 10% deposit.

I have a few questions.

1. Which of these deals would you go for?

2. if I select one now, will the payments change at the end of my term of from next month?

3. if I pick one now and rates change can I change deals before the end of my term?

4. is it worth shopping around banks or are these deals pretty in line with the market? To add I have just changed jobs so I dunno if it’s too much hassle?

5. Why is there a product fee if I’m staying with the same bank?

3. if I pick one now and rates change can I change deals before the end of my term?

4. is it worth shopping around banks or are these deals pretty in line with the market? To add I have just changed jobs so I dunno if it’s too much hassle?

5. Why is there a product fee if I’m staying with the same bank?

DIP 09/02/21

Offer on property 17/02/21

Offer accepted 18/02/21

Mortgage application submitted 22/02/21

Desktop valuation 22/02/21

Mortgage offer received 22/02/21

Solicitor instructed 23/02/21

Draft contract received and enquiries sent 02/03/21

searches back 08/03/21

Enquiries back 10/06/21

Exchanged 23/06/21

Offer on property 17/02/21

Offer accepted 18/02/21

Mortgage application submitted 22/02/21

Desktop valuation 22/02/21

Mortgage offer received 22/02/21

Solicitor instructed 23/02/21

Draft contract received and enquiries sent 02/03/21

searches back 08/03/21

Enquiries back 10/06/21

Exchanged 23/06/21

0

Comments

-

I'm not in the market for a mortgage I did that long ago

Interest rates at the moment are likely to go up if only for this year so I would go for the 2 year tracker0 -

thank you for your response. Can I ask why would you pick a tracker if you suspect they will go up?MikeJXE said:I'm not in the market for a mortgage I did that long ago

Interest rates at the moment are likely to go up if only for this year so I would go for the 2 year trackerDIP 09/02/21

Offer on property 17/02/21

Offer accepted 18/02/21

Mortgage application submitted 22/02/21

Desktop valuation 22/02/21

Mortgage offer received 22/02/21

Solicitor instructed 23/02/21

Draft contract received and enquiries sent 02/03/21

searches back 08/03/21

Enquiries back 10/06/21

Exchanged 23/06/210 -

This government will only survive another general election by getting inflation down quick and convincing the public to stay, they have only this year to achieve that.hippocrates1 said:

thank you for your response. Can I ask why would you pick a tracker if you suspect they will go up?MikeJXE said:I'm not in the market for a mortgage I did that long ago

Interest rates at the moment are likely to go up if only for this year so I would go for the 2 year tracker

The best way to get inflation down is for the Bank of England to raise rates but

That puts borrowing up, something the government doesn't want.

So my guess is it will be quick and rates will fall and thats why I wouldn't want to be in a fix for long0 -

A tracker changes with the base rate? If the base rate goes up your mortgage repayments increase?MikeJXE said:

This government will only survive another general election by getting inflation down quick and convincing the public to stay, they have only this year to achieve that.hippocrates1 said:

thank you for your response. Can I ask why would you pick a tracker if you suspect they will go up?MikeJXE said:I'm not in the market for a mortgage I did that long ago

Interest rates at the moment are likely to go up if only for this year so I would go for the 2 year tracker

The best way to get inflation down is for the Bank of England to raise rates but

That puts borrowing up, something the government doesn't want.

So my guess is it will be quick and rates will fall and thats why I wouldn't want to be in a fix for longDIP 09/02/21

Offer on property 17/02/21

Offer accepted 18/02/21

Mortgage application submitted 22/02/21

Desktop valuation 22/02/21

Mortgage offer received 22/02/21

Solicitor instructed 23/02/21

Draft contract received and enquiries sent 02/03/21

searches back 08/03/21

Enquiries back 10/06/21

Exchanged 23/06/210 -

Well I obviously knew that and why I said they will fallhippocrates1 said:

A tracker changes with the base rate? If the base rate goes up your mortgage repayments increase?MikeJXE said:

This government will only survive another general election by getting inflation down quick and convincing the public to stay, they have only this year to achieve that.hippocrates1 said:

thank you for your response. Can I ask why would you pick a tracker if you suspect they will go up?MikeJXE said:I'm not in the market for a mortgage I did that long ago

Interest rates at the moment are likely to go up if only for this year so I would go for the 2 year tracker

The best way to get inflation down is for the Bank of England to raise rates but

That puts borrowing up, something the government doesn't want.

So my guess is it will be quick and rates will fall and thats why I wouldn't want to be in a fix for long

What you have to decide is how fast and how far will they go up and

How fast will they come down

The upward trend has a head start so I'm guessing not much higher and the fix offers you have seem to think the same

I'm no financial advisor and it's probably best you take no notice

I'm old and my guesses are from my experience of life

You will no doubt hear from more qualified forumites who will give you better advice after pointing out why I'm wrong0 -

Im in a very similar situation so look forward to any more responses on this thread. Im sort of leaning towards a two year tracker but i have another month or two to decide.0

-

As your fix isn’t up until June I’d see what happens on next boe announcement next week as this will change rates

MFW 2026 #50: £3,583.49/£25,00007/03/25: Mortgage: £67,000.00

Mortgage:

07/03/26: £34,418.15

16/01/26: £56,794.25

02/01/26: £60,223.17

12/08/25: Mortgage: £62,500.00

12/06/25: Mortgage: £65,000.00

18/01/25: Mortgage: £68,500.14

27/12/24: Mortgage: £69,278.38

Savings: £20,0000

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.8K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.4K Mortgages, Homes & Bills

- 178.2K Life & Family

- 261K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards