We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

We're aware that some users are currently experiencing errors on the Forum. Our tech team is working to resolve the issue. Thanks for your patience.

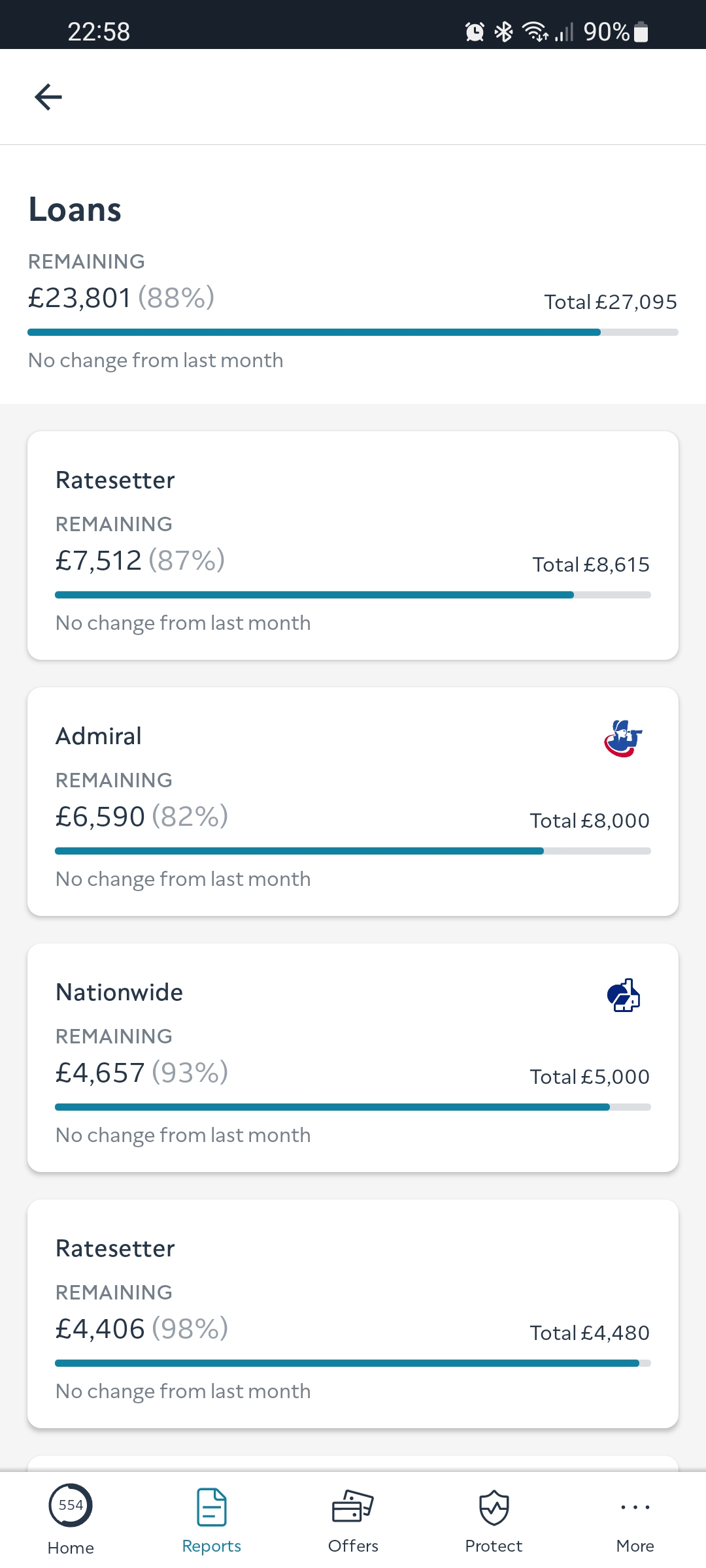

Major Trouble - £23K debt

Comments

-

As RAS says with an IVA you are on the Insolvency Register even if it fails, and you are tied in to it.

Also down the line you can get problems like this.

IVA completed but won't allow me to get car finance. — MoneySavingExpert Forum

With a DMP you are in control if circumstances change you can either increase or decrease your payments.

So think very carefully about your way forward.If you go down to the woods today you better not go alone.0 -

IVA`s are getting a bit long in the tooth these days, I guess they are still useful to some people, but that list gets shorter all the time, for the majority they are too restrictive, too inflexible, and last far too long.

They were originally designed as an alternative to bankruptcy for those with assets to protect, however due to quite lax regulation, the debt management companies saw an opportunity to make money from them, due to the large fee`s that can be charged, and they have since gained a reputation for being mis-sold on a massive scale to those who may technically qualify for one, but who would be much better off with a different solution.

They are sold with the headline "write off 70% of your debts" or statements to that effect.

It doesn't always happen that way, it depends greatly on your disposable income, and if your income increases over what can turn out to be up to 7 years in most cases, the vast majority of takers who sign up to these arrangements do so without fully understanding how they work.

Since IVA`s were introduced, debt management has become a whole lot easier and more widely accepted, than it previously was, although an IVA can give you legal protection from creditor action, nowadays those in debt management find they don`t really need that, as most creditors, once an arrangement is in place, are quite happy to take your money on a monthly basis until the debt is repaid, this has not always been the case.

But with updated guidelines from the FCA on debt collection practices, plus the cost of living crisis, the emphasis is now mainly on affordability, lenders will accept more or less what your budget says you can afford without question, reduced settlement offers are more frequent, and even write off`s on health grounds are easier to obtain.

Add all this together and the need for insolvency reduces to the point where it really won`t benefit you that much, much better and simpler to go the DMP route and look to make settlement offers further down the line.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter1 -

Okay thanks guys. I'll perform a new SOA. As a general rule should I wait til all the debts have defaulted before starting the DMP, so that the interest stops? They've all not been paid for 5 months but no notification of defaults, and my credit report doesn't state default (attached image)

0

0 -

Yes - best bet with a DMP is to allow everything to default.🎉 MORTGAGE FREE (First time!) 30/09/2016 🎉 And now we go again…New mortgage taken 01/09/23 🏡

Balance as at 01/09/23 = £115,000.00 Balance as at 31/12/23 = £112,000.00

Balance as at 31/08/24 = £105,400.00 Balance as at 31/12/24 = £102,500.00

£100k barrier broken 1/4/25

Balance as at 31/08/25 = £ 95,450.00. Balance as at 31/12/25 = £ 91,100.00

SOA CALCULATOR (for DFW newbies): SOA Calculatorshe/her1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards