We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

2 year base rate tracker

Parties03

Posts: 87 Forumite

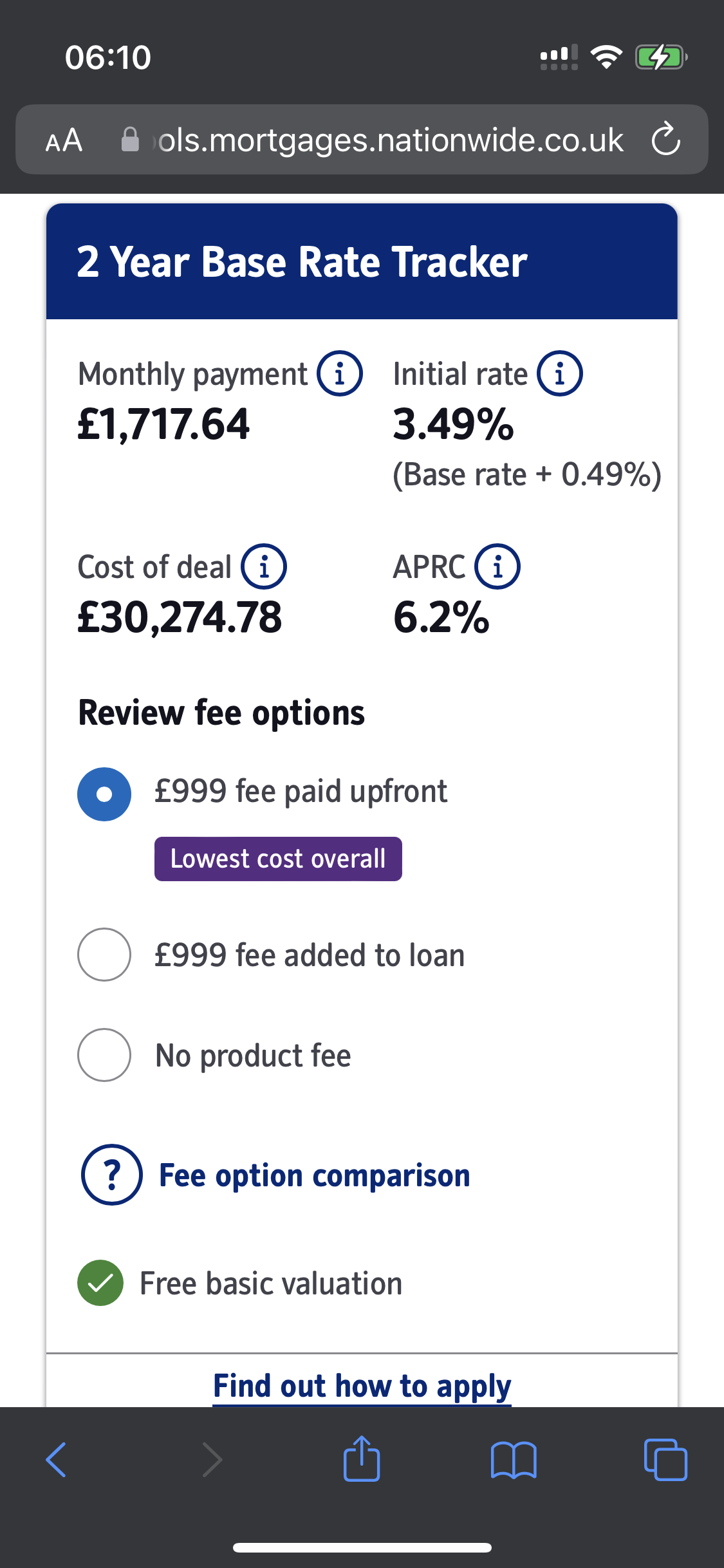

Hi, can someone explain this sort of mortgage to me please?

It’s looking like we may break chain to secure our sale and then purchase our next home, we would therefore not be able to port our mortgage.

It’s looking like we may break chain to secure our sale and then purchase our next home, we would therefore not be able to port our mortgage.

I only want to fix for 2 years with the interest rates being so high right now.

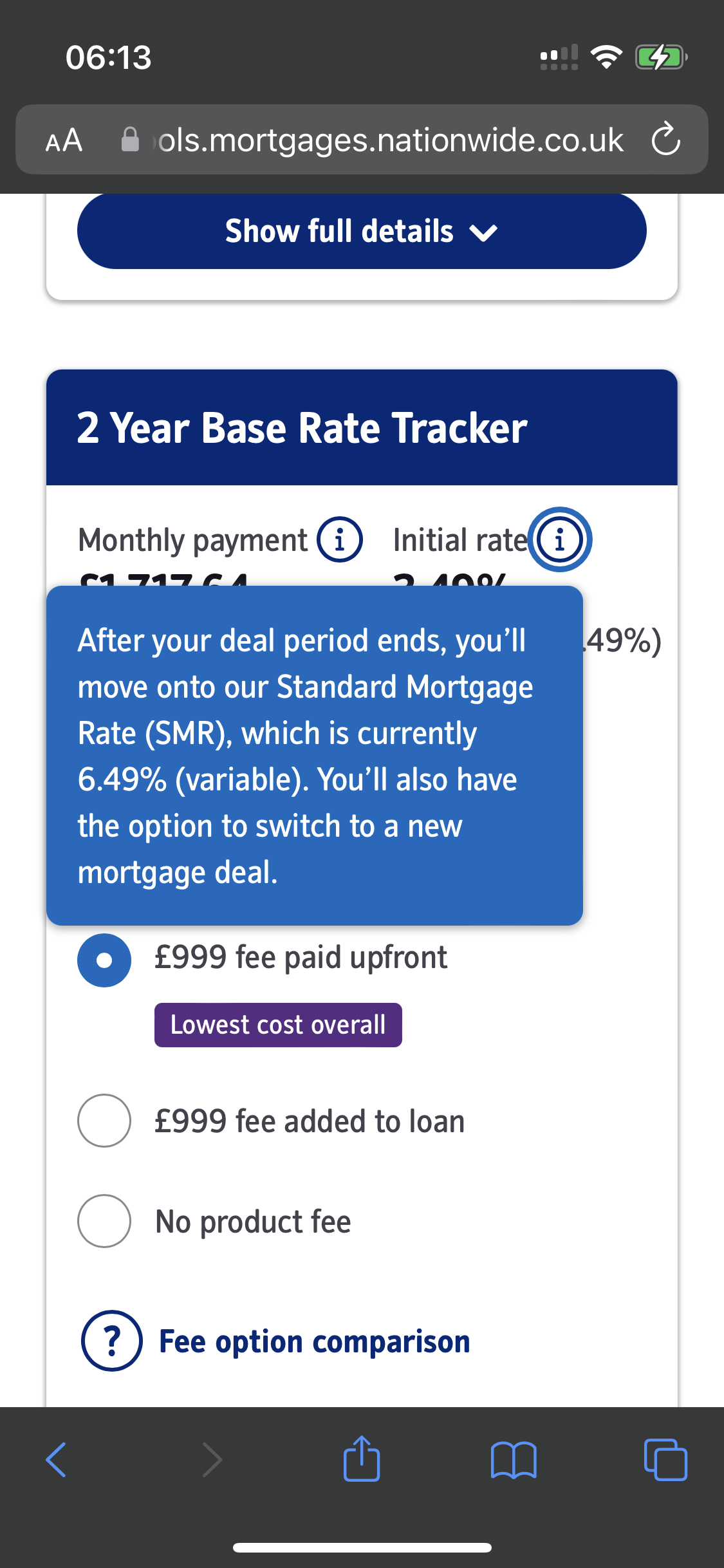

I came across this 2 year base rate tracker, but I’m confused. Is the 3.49% fixed for two years, much like a fixed term? Or can this change? It says quite clearly what the monthly payments for 2 years would be so then it moves to a higher SMR, at which time we would switch products.

Am I misunderstanding something here?

Thanks

0

Comments

-

It would change up or down with every change of base rate by Bank of Englad. The one you showed seems to be 0.49% above current rate of 3%

If Bank of Englad was to increase the base rate to 4% then you would start paying immediately 4.49% rate.1 -

It's also worth bearing in mind that the standard base rate, currently 0.49%, could change willy nilly. It used to be 0.96% not too long ago!1

-

Just making sure you've checked the conditions on your current mortgage portability? Some allow the mortgage to port with a delay/broken chain as long as the new house is purchased within a certain timeframe.0

-

So apparently if we complete within 3 months we can get back the early repayment charge for the first mortgage if we use the same lender. Otherwise from what our broker has said, unfortunately we can’t port this one which is a bummer as the rate is so much better.rc28 said:Just making sure you've checked the conditions on your current mortgage portability? Some allow the mortgage to port with a delay/broken chain as long as the new house is purchased within a certain timeframe.0 -

The bit that I’m confused about is that this is called an “intial rate” which makes it sound like it is fixed irrespective of the base rate.muffinek said:It would change up or down with every change of base rate by Bank of Englad. The one you showed seems to be 0.49% above current rate of 3%

If Bank of Englad was to increase the base rate to 4% then you would start paying immediately 4.49% rate.0 -

If it was fixed then it wouldn't be a tracker. Tracker rates track the BOE rate, if that rises your mortgage monthly payments rise with it, if it falls your month payment falls with it. The initial rate is the 0.46 above BOE, after the 2 years you revert to the SVR.Parties03 said:

The bit that I’m confused about is that this is called an “intial rate” which makes it sound like it is fixed irrespective of the base rate.muffinek said:It would change up or down with every change of base rate by Bank of Englad. The one you showed seems to be 0.49% above current rate of 3%

If Bank of Englad was to increase the base rate to 4% then you would start paying immediately 4.49% rate.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.8K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.4K Mortgages, Homes & Bills

- 178.2K Life & Family

- 260.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards