We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Early Repayment Charge - what to do

Haywooddiablo

Posts: 4 Newbie

I'm a little bit confused by HSBCs ERC and hoping someone can advise.

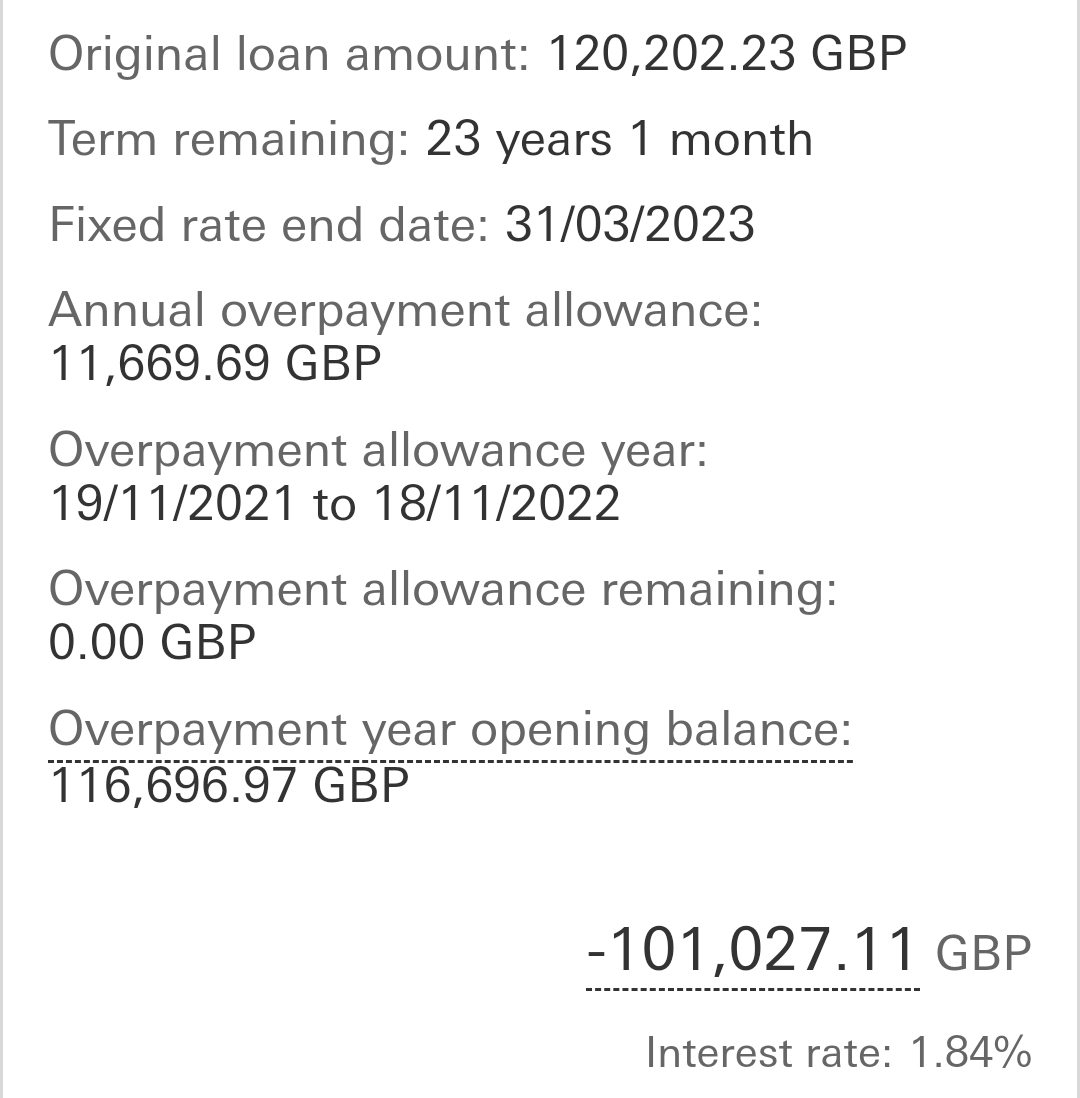

As you can see, our fixed rate is due to end in March '23, and given the rates of interest, I've decided to lock in a new rate now. That's at about 5.5% for 5 years.

As you can see, our fixed rate is due to end in March '23, and given the rates of interest, I've decided to lock in a new rate now. That's at about 5.5% for 5 years.

I've overpaid by the allowed 10% this year, and as soon as I take out the new deal I was going to overpay by the 10% again, so around £10k.

I was then considering overpaying by another c.£15k on top of the 10%, but know there's an Early Repayment Charge of 1% for the remaining term (which I think is just the fixed part)

If it's worth doing given the penalties, I had a last minute thought, that I'd be best off doing this now with my fixed term about to end, than doing this when the new deal starts. Is that right? Trying to figure if I've understood that correctly!!

TIA

As you can see, our fixed rate is due to end in March '23, and given the rates of interest, I've decided to lock in a new rate now. That's at about 5.5% for 5 years.I've overpaid by the allowed 10% this year, and as soon as I take out the new deal I was going to overpay by the 10% again, so around £10k.

I was then considering overpaying by another c.£15k on top of the 10%, but know there's an Early Repayment Charge of 1% for the remaining term (which I think is just the fixed part)

If it's worth doing given the penalties, I had a last minute thought, that I'd be best off doing this now with my fixed term about to end, than doing this when the new deal starts. Is that right? Trying to figure if I've understood that correctly!!

TIA

0

Comments

-

To me it looks like your overpayment allowance resets on 19/11. So on 19/11 you should be able to overpay without penalty by up to 10% of whatever the opening balance is on 19/11.I'm not sure what happens on 01/04 - does the overpayment allowance reset or does the same window continue to 18/11/2023.0

-

Do you have an ERC now, if you move to a new deal before the end of this fix? If so, how much is it and does it make the whole deal unpalatable? I'd be thinking that an increase from your current 1.84% to 5.5% plus a repayment charge to end the current deal early isn't very attractive, particularly factoring in the loss of 1.84% for nearly 6 months.I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.1

-

Thanks. I'm just nervous that if I wait until Jan when I can lock in a new deal, that the rate will have gone up even higher and in the long term I'd be worse off! That's why I thought I'd take the hit, albeit to your point, 6 months loss at 1.84% is costly.silvercar said:Do you have an ERC now, if you move to a new deal before the end of this fix? If so, how much is it and does it make the whole deal unpalatable? I'd be thinking that an increase from your current 1.84% to 5.5% plus a repayment charge to end the current deal early isn't very attractive, particularly factoring in the loss of 1.84% for nearly 6 months.0 -

@haywooddiablo Assuming that what you're trying to do is a product-switch (PT) and staying with HSBC -

- you should be able to delay the new product kicking in for up to 120 days. So if you apply for a PT on 01 Nov, you *should* be able to delay the switch to 28 Feb or so. I've done this a couple of times recently for clients' HSBC PTs so I'm assuming the same will be possible direct

- with HSBC usually the ERC is pro-rated at 1% per year remaining so if you do the above, the ERC payable in a fix ending 31/03/2023 should only be 1/12 of 1% of the outstanding loan size on 28 Feb.Haywooddiablo said:

Thanks. I'm just nervous that if I wait until Jan when I can lock in a new deal, that the rate will have gone up even higher and in the long term I'd be worse off! That's why I thought I'd take the hit, albeit to your point, 6 months loss at 1.84% is costly.silvercar said:Do you have an ERC now, if you move to a new deal before the end of this fix? If so, how much is it and does it make the whole deal unpalatable? I'd be thinking that an increase from your current 1.84% to 5.5% plus a repayment charge to end the current deal early isn't very attractive, particularly factoring in the loss of 1.84% for nearly 6 months.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards