We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Index Linked

Comments

-

Okay, so the assumption is that the inflation is a mere blip, due to the duration. And the market feels that interest rates will be 'stickier' than inflation.

I'm willing to bet that's not the case, I think I will get involved.

Some details below from RL's own library pages.

0 -

Most linked bonds are inflation + a little bit, so it's not entirely clear to me why the duration is so significant to an index linked fund. Presumably if the BoE are putting them to the market now, the little bit is more than the little bit the fund is already holding, I suppose.0

-

Duration and interest rates are important to all bonds equally, as the price of a bond is basically the present value of all the cashflows (ignoring the risk of default, which rounds to zero for gilts).

E.g. for a two year conventional gilt, with say 3% coupons and interest rates of 3%, and coupons paid annually for simplicity the value is as follows:

Value = 0.03/1.03 + 1.03/1.03^2 = 1

Now with interest rates of 6%, the value is:

Value 0.03/1.06 + 1.03/1.06^2 = 0.945 , so a fall of nearly 6% as duration is just under 2.

For the equivalent index-linked bond, the only difference is the coupons and redemption payment are linked to inflation.

i.e. inflation = 5%

Value = 0.03*1.05/1.03 + 1.03*1.05/1.03^2 = 1.05

And with interest rates rising to 6%

Value = 0.03*1.05/1.06 + 1.03*1.05/1.06^2 = 0.99

So the same percentage fall.

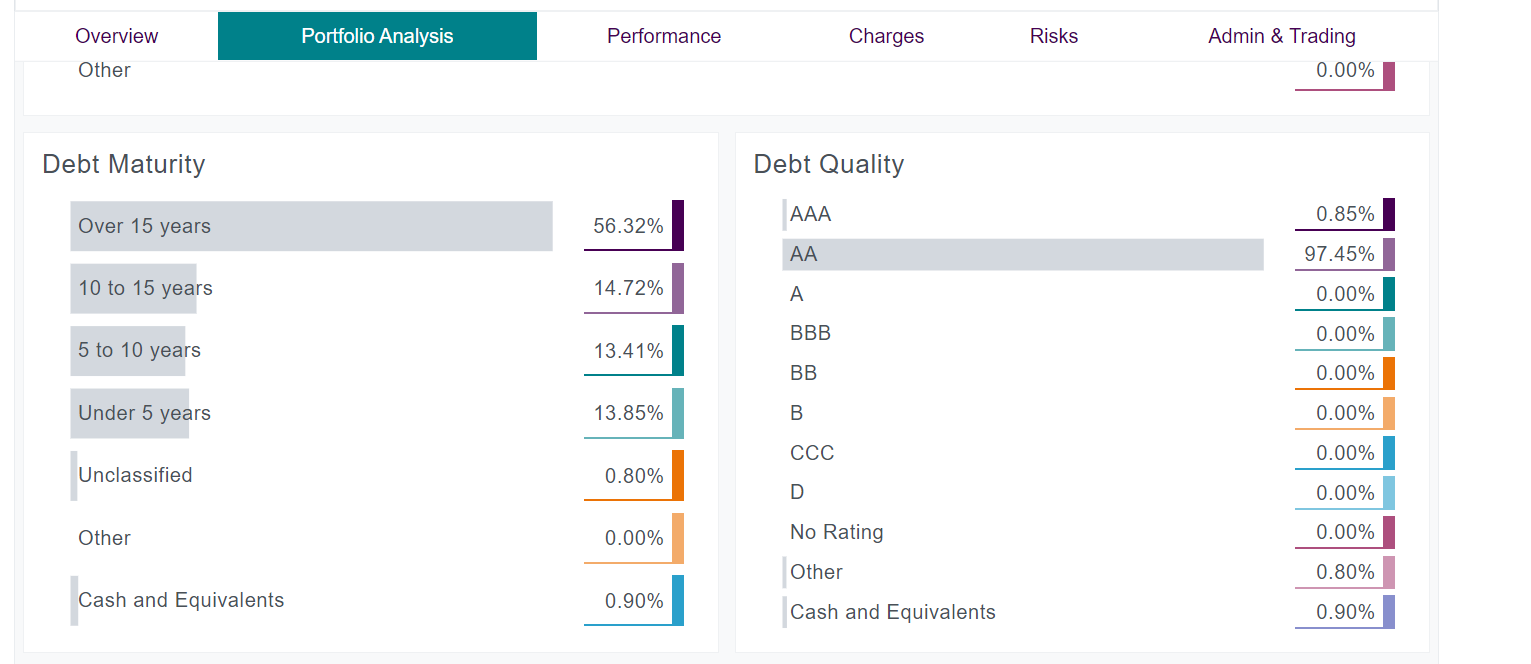

For the 15 year duration, the impact will be larger to the degree of (1+n)^(15/2). where n is the change in the interest rate.

Pensions actuary, Runner, Dog parent, Homeowner1 -

Duration is fundamental to any bond. On the day new bonds are issued with a different coupon you have a new price set for all bonds in circulation and the impact is much more significant for long duration bonds. You need to read up on this.Altior said:Most linked bonds are inflation + a little bit, so it's not entirely clear to me why the duration is so significant to an index linked fund. Presumably if the BoE are putting them to the market now, the little bit is more than the little bit the fund is already holding, I suppose.1 -

The “stickiness” of interest rates is not important. Mr Market cares about linkers issued today.Altior said:Okay, so the assumption is that the inflation is a mere blip, due to the duration. And the market feels that interest rates will be 'stickier' than inflation.

I'm willing to bet that's not the case, I think I will get involved.

Some details below from RL's own library pages.If they pay a better coupon over your duration then the value of what you own plunges. Say you need 100 GBP in coupon monthly. If the rate on new issues goes up, you can get this 100GBP for less. And that impacts old issues. Because who would want to pay the “old” price for your old car if you can get a new one thats exactly the same (pays the same 100GBP) but cheaper?1 -

This is correct. When Truss borrows her £100bn, the BoE will make some gilts for this purpose. There will be more gilts in supply which will lead to a reduction in the price of existing bonds, and higher interest rates.Deleted_User said:

Duration is fundamental to any bond. On the day new bonds are issued with a different coupon you have a new price set for all bonds in circulation and the impact is much more significant for long duration bonds. You need to read up on this.Altior said:Most linked bonds are inflation + a little bit, so it's not entirely clear to me why the duration is so significant to an index linked fund. Presumably if the BoE are putting them to the market now, the little bit is more than the little bit the fund is already holding, I suppose.

Conversely if the BoE decides to write off it's own debt by buying it's own bonds with made up money (QE), the price of bonds goes up and interest rates go down.Pensions actuary, Runner, Dog parent, Homeowner1 -

Yes, most of these concepts I'm aware of, ordinarily topics of a numerate or financial nature are intuitive to me but I need to crunch the numbers and put the jigsaw pieces together. It's not that I'm feeling the market is missing something, more so I'm trying to work out exactly what it's seeing that I'm not.

The info provided so far has been very helpful.

Another variable is surely when fund manager has to buy more, as the bonds they hold mature. Interestingly, the short version of this fund is top heavy with short duration maturing quite soon. I do already hold some of this in my workplace pension portfolio.

0 -

There's a number of factors that impact the price of index-linked bonds. I'll give some examples, led by demand, as we've already talked about supply.

The main buyers of these bonds are pension funds and insurance companies. These have liabilities which increase in real terms, so to protect against inflation they need to buy an inflation-linked asset. In general these schemes are now well hedged, and the amount of index-linked bonds needed will decrease over time as the schemes mature. Also, fewer retirees are buying annuities, so less there are fewer gilts being held in DC pensions.

All else being equal then the price of gilts falls.

There's a related phenomena in pension schemes, which is quite abstract. Pension increases usually have a cap (except in the public sector, which are largely unfunded anyway), say 2.5%, or 5% annually. When inflation is very high, like now, these caps come into play. The liabilities therefore behave more "nominally", and less linked to inflation. Therefore many schemes and insurers providing annuities will have been mechanistically selling index-linked gilts.

There also exists a premium for having an inflation-linked asset. This premium changes all the time, and tends to be higher when inflation is uncertain, i.e. now, which impacts price.

All in all, the impacts on prices are very nuanced, and not just led by future inflation expectations. It's fair to say that the gilt markets are more led by the needs of purchasers, and less by speculative investors. I would only buy gilts if I needed to hedge against interest rates and inflation, e.g. I was near to retirement, as the need for inflation matching can be met in the long term by holding equities (company profits are more or less linked to inflation), and corporate bonds provide a better return than gilts whilst hedging against interest rates.Pensions actuary, Runner, Dog parent, Homeowner2 -

Thanks for taking the time to provide this detail biscan25, really helpful.

The short index linked and conventional short gilt funds started at the same date in 2004, so are ideal for comparing. As you suggested and demonstrated, they are very heavily correlated. It's only in the last year that significant divergence has actually taken place. So we should expect them to converge again, question is, will that mean the linked losing value, or the conventional gilts gaining value.

I'm moving away from the prospect of placing significant amounts in these types of funds. The rational was that I feel the US equity space is overheated and I wanted to park the cash where it had some theoretical inflation protection, and move it back into equities when there is a correction (potentially).

For any readers interested, I found some useful resources when investigating this, especially the DMO website Gilt Market

Articles about tips, but same principles apply:

I bonds, TIPS, and inflation

Negative TIPS Yields0 -

There's been a huge move in real yields (almost all driven by nominal yields) which long dated linkers are extremely sensitive to. The reason they were so high last year was the reverse process. The duration is important as already noted above. Linkers tend to have longer duration due to the very small coupon hence the cashflows are much more dependent on the final repayment of principal. Ultra long dated linkers can be extremely volatile, more so than equities at times.

They do still provide good protection against inflation, but are subject to similar influences to conventional gilts when rates move, except more so due to the duration. The rate moves have overshadowed the inflation element this year, and the market was already anticipating inflation a lot higher than official forecasts a year ago, so it was already in the price then.

As also noted, the pricing of index linked gilts has been heavily driven by pension funds especially, and insurers to a lesser degree. Many were buying them purely to hedge the risk off the sponsor balance sheet and were paying little regard to price. UK linkers were therefore more expensive than US TIPS say.....there was also an influence from the RPI v CPI 'wedge' (the difference in inflation between the two calculations). IL gilts carried a premium because they linked to RPI not CPI, although that difference will disappear in 2030 which has gradually been discounted in market pricing of linkers too.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards