We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Why are the mortgage tables dominated by building societies and discounted rates?

IAMIAM

Posts: 1,432 Forumite

Are these 'better' than trackers? The rates are very good

0

Comments

-

@iamiam Pros and cons. With trackers you know what you're getting, with discounts the lender has more flexibility to hike their SVR.

In some cases the flexibility works in your favour (most BS SVRs haven't passed on the whole BoE rate hikes through) and in some cases they may not.

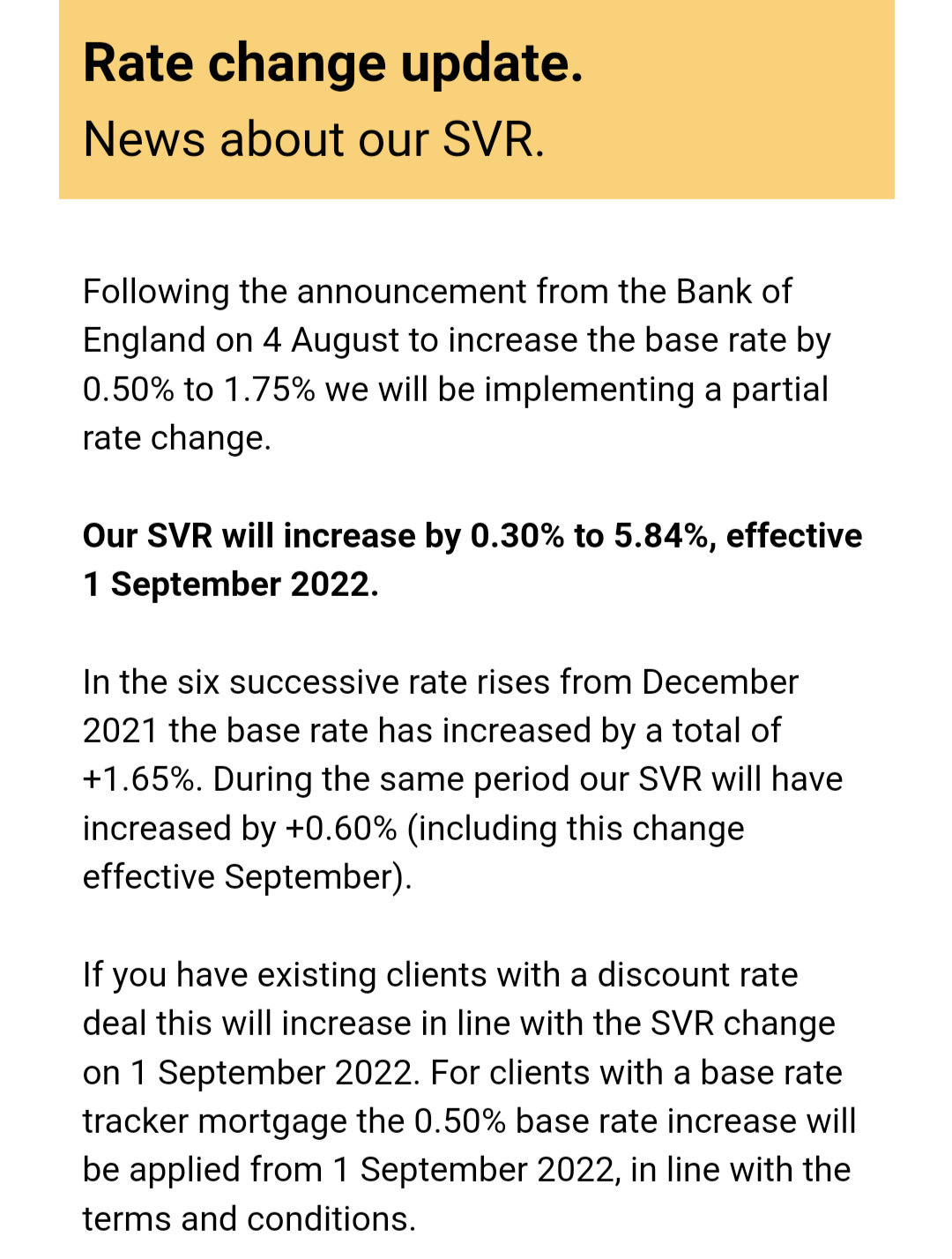

As an example, see the email below from a BS advertising their discount rates.

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

2 -

I made a post about this a few weeks ago.

Apparently building societies (unlike banks) have to do a particular amount of variable rate mortgages (that can be discounted rates, tracker rates etc). Nobody wants them at the moment, but the b/s still have to do them.

In order to get them out, they are doing them cheaply.I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.1 -

I'm in a similar situation.. Have always stuck to 2 year fix deals but am now tempted to take the risk on a discounted variable. Furness have offered me a starting 1.64% after the BoE 0.5 rise (They only applied a 0.2 increase on their own rate).. The best fix I can get is 3.15% so it's a considerable difference and the BoE rate would likely need to rise by at least another 1.5% in the next 2 years before I am worse off, if not more...

Difficult situation to be in and decision to make!0 -

They are not the only b/s to not pass on the full rate rise.

The worry from applicants (understandably) is what happens if they choose to just bump the rate up. But as I mentioned above, these b/s need a certain level of business on variable rates and its not a small amount - 40% with one of the b/s - so its not a ploy to get you in, its due to the fact they need people on variable rates in order to lend more on fixed rates.I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.0 -

I’m with Coventry on a flexx for term mortgage. Since the rises started I’ve moved from 1.75 to 2.35%. Increases were .15% not .25% I’m waiting to see what they do with the Bank of England .5% increase though as I’ve had no correspondence since that happened. For me it’s not ideal but bearable as my outstanding balance is about £45k. Anxiety levels would be much higher with a balance over £200k. Trying to overpay as much as I can but my plans to do big overpayments have been scuppered by increases elsewhere. I really feel for people just starting out with huge mortgages.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards