We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Pay ERC and fix at current rates, or stay put

Lots of similar discussions recently.

Our individual circumstances: current fix with Barclays @2.44% ends in August 2023 with LTV comfortably below 60. The earliest we can lock in new rate is end of April 2023. That's five BoE interest rate reviews away. Current reasonable expectation is that there will be one more hike of 0.5 percentage points, and four of 0.25, taking the BoE interest rate to 3%, making most products available to us being around the 5 to 6% interest rate.

We are mid-term committed to the area where we currently live (until 2028/2029).

We are facing two options for:

- Pay £6k ERC, change product to current 7yr @2.70% offer for existing customers, pay £1000/month (lowest monthly we have ever paid) and stop worrying about interest rates, OR

- Stop panicking, keep the £6k and use it as a buffer to ride through whatever the next 9 months throw at us. If assumptions about interest rates above are correct, I am looking at £275 more per month (highest monthly we have ever paid), which will eat my £6k saved ERC in roughly 2 years.

For the time being me and wife lean more towards the first option. We even booked a Barclays mortgage advisor to do it, and they are all booked for weeks ahead, inundated with requests from people frantically trying to fix and paying exorbitant ERCs.

Judging by where things are going with energy prices and inflation, I personally think all bets are off by now for the next 2-3 years. Earlier this year, in March, I had a hunch about the energy market, and signed up for a fix that looked expensive at the time around the 1st April cap hike. This fix looks really cheap now compared to the current predictions for January 2023 (which is when the big heating bills come). I have the same hunch now - politicians and BoE have lost all control, and this is no time for gambling. GOV.UK will have no choice but to borrow and raise wages in the public sector to keep up with rising energy cost, which will drag everything into an inflationary spiral, forcing BoE to sacrifice big parts of the economy with higher than expected interest rates to try and put out the inflation fire. Buying peace of mind for £6k sounds like a good deal.

Any thoughts?

Comments

-

I think it’s impossible to predict interest rates for 7 years so it’s up to you.

Would you fix at ~3.05% for 7years if there was no ERC? (I’m guessing the £6k over 7 years amounts to about 0.25%) - I think that’s how I would look at it if I was in your position.No one has ever become poor by giving0 -

@id311299 Is there any reason you didn't use a mortgage broker to skip the Barclays queue? If you don't have a broker or don't want to pay a fee, there are plenty of fee-free brokers listed on the MSE guide hereid311299 said:

We are facing two options for:

- Pay £6k ERC, change product to current 7yr @2.70% offer for existing customers, pay £1000/month (lowest monthly we have ever paid) and stop worrying about interest rates, OR

- Stop panicking, keep the £6k and use it as a buffer to ride through whatever the next 9 months throw at us. If assumptions about interest rates above are correct, I am looking at £275 more per month (highest monthly we have ever paid), which will eat my £6k saved ERC in roughly 2 years.

For the time being me and wife lean more towards the first option. We even booked a Barclays mortgage advisor to do it, and they are all booked for weeks ahead, inundated with requests from people frantically trying to fix and paying exorbitant ERCs.https://www.moneysavingexpert.com/mortgages/best-mortgages-cashback/#step3

Not sure about Barclays off of the top of my head, but some lenders don't allow brokers to do PTs if there's an ERC involved, so it may well have not been an option for you.

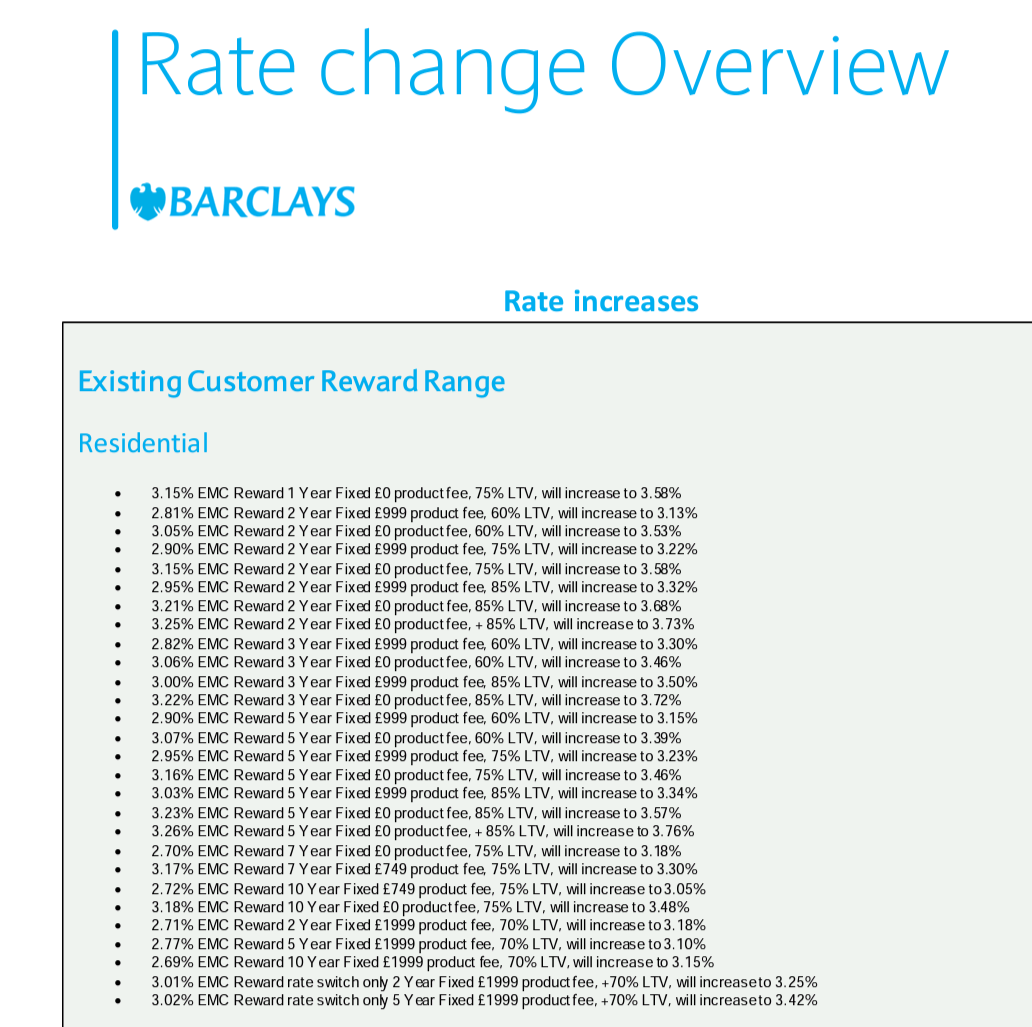

The 7yr 2.7% PT rate is being pulled tonight and replaced by 3.18%. I just reserved a 5yr fix PT rate for a client of mine this evening so they have the option to go ahead with it tomorrow if they wish to.

Mind you, everything I've said above relates to intermediary products, it may or may not be the same direct.

I hope you're able to get the 2.7% rate (or something that works for you), good luck!I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

2 -

Hi K_S,

Thank you for the heads up. I am really surprised that Barclays are pulling the deal I was referring to - I've been watching the SONIA swaps like a hawk since the last BoE rate rise, and they haven't really moved for the 7 years swaps and have even fallen for the 10 year swaps. Must be the stampede of customers switching and Barclays deciding that they can profit more on the back of the demand.

As for not using a broker - we have had a very poor experience with one when we were buying for the first time, and since then we've been doing everything ourselves.

I was ready to pay the ERC and fix for very long at the bottom of the interest rates in October 2021. I have allowed a Barclays mortgage advisor to convince me that it's not worth it. I have only myself to blame. Sigh...

0 -

I agree. What I am trying to achieve is to hedge against the possibility of absurd interest rates. They have been barely lifted off the floor, so not much room for going down. On the upwards direction, however, the sky is the limit, with catastrophic consequences for many households.thegentleway said:I think it’s impossible to predict interest rates for 7 years so it’s up to you.

Would you fix at ~3.05% for 7years if there was no ERC? (I’m guessing the £6k over 7 years amounts to about 0.25%) - I think that’s how I would look at it if I was in your position.

Those who think that ridiculously high interest rates are not possible, should remember that only months ago the idea of a 500% increase in energy prices YoY would have been laughable.0 -

It is not possible to predict future interest rates, but going by the trend I think we may see mortgage rates around 5-6% for few years. That is the reason I am thinking of fixing it at 3% for next 10 years https://forums.moneysavingexpert.com/discussion/6379178/should-i-pay-erc-of-10500#latest1

-

K_S said:

Mind you, everything I've said above relates to intermediary products, it may or may not be the same direct.

I hope you're able to get the 2.7% rate (or something that works for you), good luck!This morning the 2.7% deal is still listed in the Rates for existing customers on the Barclays website. - They posted the new rates a little bit later in the morning.Just curious, how come their 7yr no-fee fix for intermediaries offers a lower interest rate than the £749 fee equivalent (same LTV)?

0 -

Orchid96 said:It is not possible to predict future interest rates, but going by the trend I think we may see mortgage rates around 5-6% for few years. That is the reason I am thinking of fixing it at 3% for next 10 years https://forums.moneysavingexpert.com/discussion/6379178/should-i-pay-erc-of-10500#latestI've been trying to do some 'prediction' by watching the SONIA swap rates for 1,2,3,5,7 and 10 years.To my knowledge, the banks base the interest rates for their Fix products on the SONIA swap rates (swaps are being used by banks to hedge the risk of future interest rate increases). I've been watching these swap rates like a hawk for some time now, and I noticed that the banks appear to know in advance that these swap rates are about to increase. The system is rigged in their favour - they are literally allowed to see in the future what the swap rates will be, and adjust their product rates before the Joe public can possibly know and take defensive action.If the banks have access to products to hedge their interest rate risks, is there a similar product available for the borrower?Edit: I am being stupid. Paying the premium for a fixed rate as a borrower is effectively hedging your risks of future interest rate increases.0

-

Right, crunchtime for me - meeting with Barclays mortgage advisor is tomorrow, and I have made the necessary overpayments to bring my LTV down to 60%, and I have prepared the money for the ERC and new product fee. Judging by the movement of the swap rates, there is a very high chance Barclays will raise their fixed rates tonight, which means that I am looking at around 3.5% rates for 5Y (currently 3.15%). Still makes sense to me compared to expectations of 7%.@K_S: any chance you would share if Barclays have circulated another change to their products for tomorrow?0

-

@id311299 Sure. There's nothing that's come through yet, so you should be safe for tomorrow. In any case I don't think there's an immediate risk, given that they upped the Reward rates just last Tuesday.id311299 said:Right, crunchtime for me - meeting with Barclays mortgage advisor is tomorrow, and I have made the necessary overpayments to bring my LTV down to 60%, and I have prepared the money for the ERC and new product fee. Judging by the movement of the swap rates, there is a very high chance Barclays will raise their fixed rates tonight, which means that I am looking at around 3.5% rates for 5Y (currently 3.15%). Still makes sense to me compared to expectations of 7%.@K_S: any chance you would share if Barclays have circulated another change to their products for tomorrow?I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards