We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Bankruptcy help please - desperate

Mollymoo45

Posts: 7 Forumite

Hi everyone,

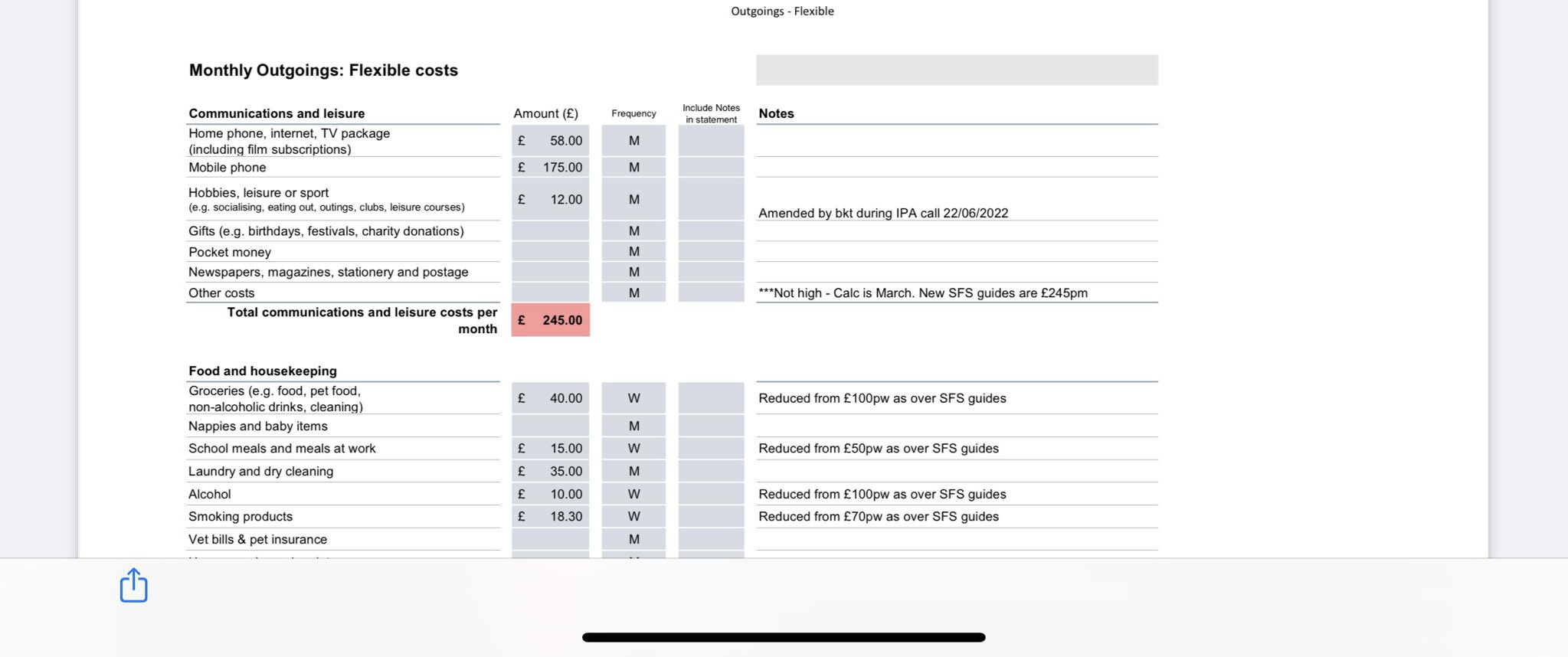

I’m writing for a friend, he is in a very bad way. He has old debts, credit cards, store cards etc, he was with stepchange, paying £700 per month. He is struggling to pay stepchange. His husband took a loan out for him as he has a poor credit rating and he also has to pay him back £320.00 per month. He has had a call from the insolvency service and had an IPA Assessment, they want him to pay £1200 per month. He is really low and doesn’t know what to do. His relationship is suffering as he husband is paying for everything which is putting a Strain on their relationship. They can’t go out as his husband has to pay and this causes arguments, can’t go on holiday etc. the IPA Assessor has reduces all his weekly spending he smokes a packet of cigarettes a day and the assessor has said he can afford 1 packet a week, he has reduces all his usual,spending by around 60%, even his dry cleaning ( he is a teacher) . It gets worse. He is now in a worse position than he was with stepchange. Does anyone have any experience with IPA’s please? They have even said the loan has to be paid by his husband and not him. This is making the relationship even worse. I’m sorry this is a bit disjointed - he is so desperate for help, I don’t know where to turn for him.

I’m writing for a friend, he is in a very bad way. He has old debts, credit cards, store cards etc, he was with stepchange, paying £700 per month. He is struggling to pay stepchange. His husband took a loan out for him as he has a poor credit rating and he also has to pay him back £320.00 per month. He has had a call from the insolvency service and had an IPA Assessment, they want him to pay £1200 per month. He is really low and doesn’t know what to do. His relationship is suffering as he husband is paying for everything which is putting a Strain on their relationship. They can’t go out as his husband has to pay and this causes arguments, can’t go on holiday etc. the IPA Assessor has reduces all his weekly spending he smokes a packet of cigarettes a day and the assessor has said he can afford 1 packet a week, he has reduces all his usual,spending by around 60%, even his dry cleaning ( he is a teacher) . It gets worse. He is now in a worse position than he was with stepchange. Does anyone have any experience with IPA’s please? They have even said the loan has to be paid by his husband and not him. This is making the relationship even worse. I’m sorry this is a bit disjointed - he is so desperate for help, I don’t know where to turn for him.

Thanks in advance for any help at all,

Molly x

Molly x

0

Comments

-

The loan to husband will be included in the bankruptcy. Really need to see what his outgoings are to advise further0

-

Having read again, whose name is the loan in?0

-

Does your friend have any assets? A house? A part-share of a house? Expensive car? Bankruptcy would likely take these away if he had them.. However if he has no assets aside from all his debts, bankruptcy could be an option. How much does your friend owe in total? (If the husband took out the loan in his own name - this debt couldn't be included in bankruptcy though, so they'd have to come to a private arrangement on that - however the official receiver likely wouldn't recognise it when looking at earnings and outgoings)0

-

He is a council tenant, no car. He takes the train to work. I’ll try and copy and add the assessment here without his personal details0

-

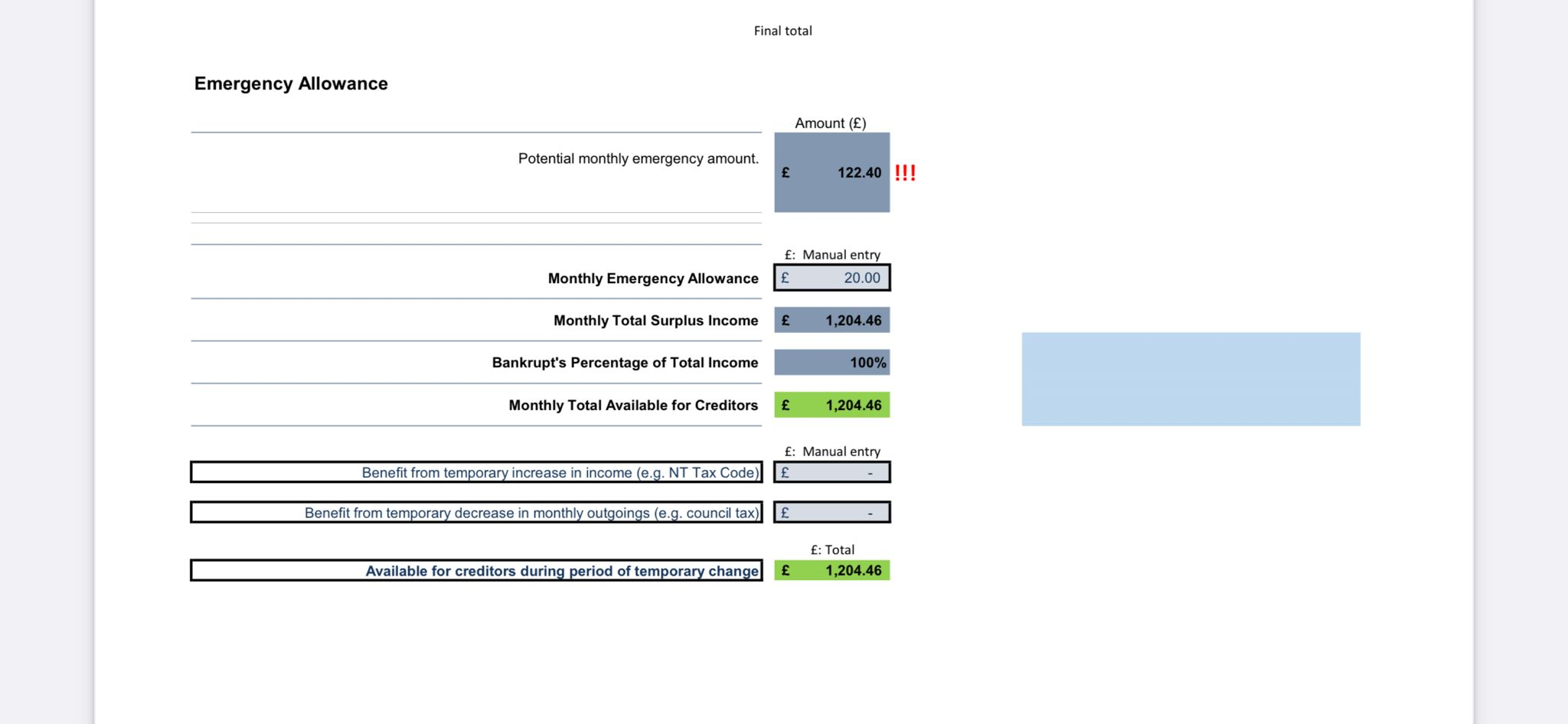

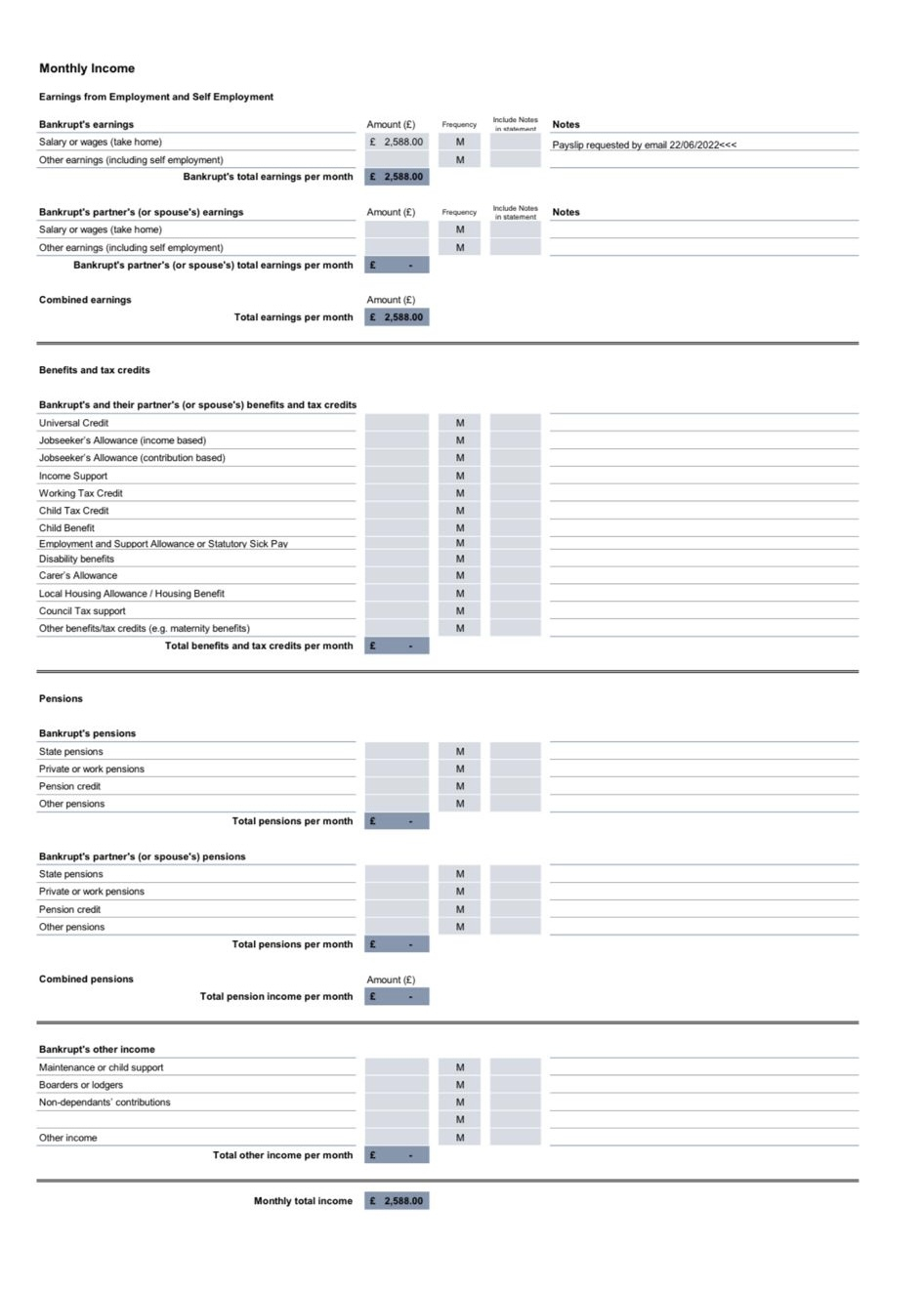

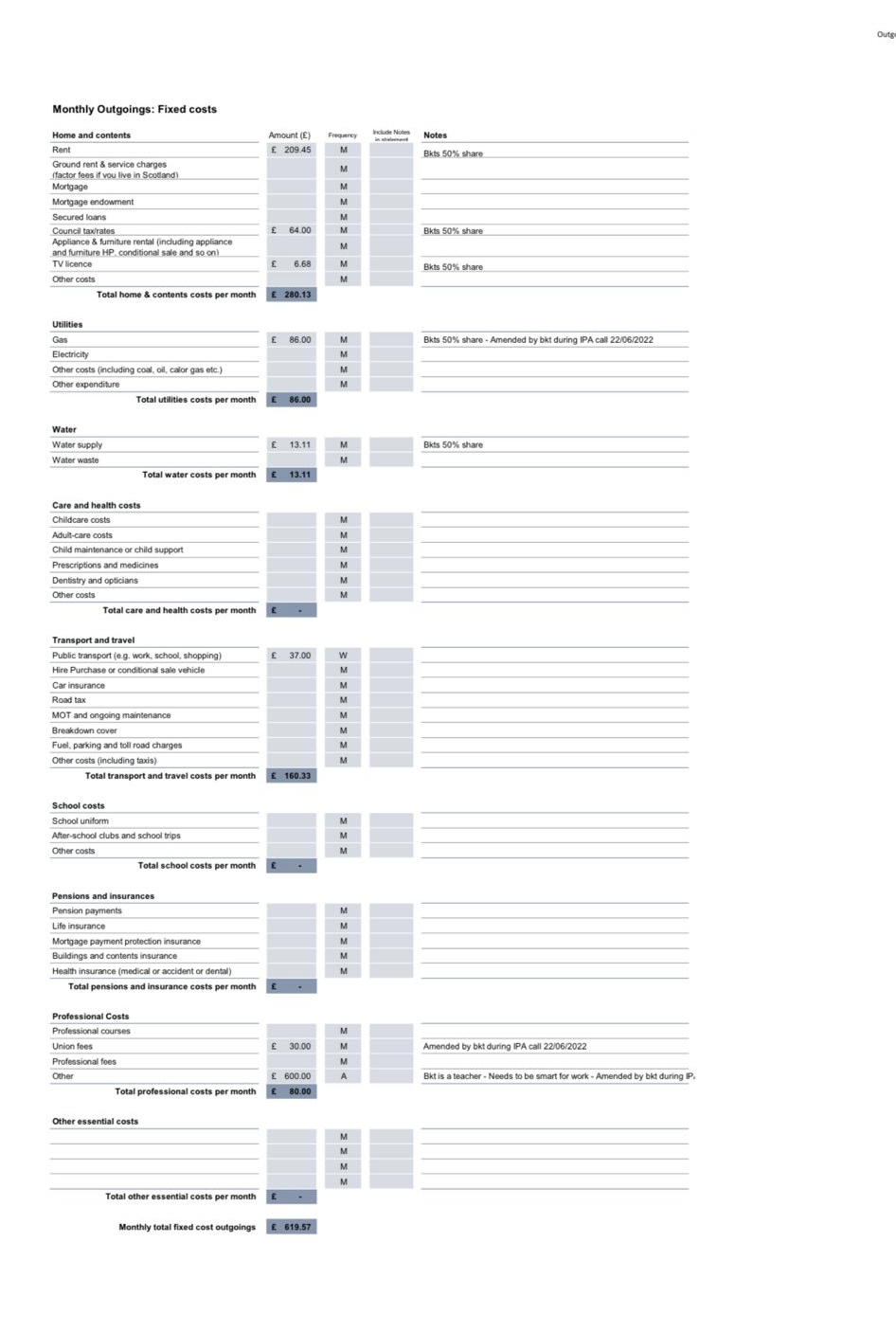

This is his assessment, I hope this is ok

This is his assessment, I hope this is ok

0 -

He is in a worse situation than when he was with stepchange. He thought all his worries would be gone, but they have increased ten fold. They are going to leave him with nothing. With the utilities increase and food costs rising, this has not been taken into consideration.

Thanks for all your messages x0 -

So why has he not got back in touch with stepchange and re-done his budget?

Or is the problem that he is making preferential payments to the loan taken out by his husband?

If you've have not made a mistake, you've made nothing1 -

You haven't mentioned what the total debts are. It's normal that the potential bankrupt does contribute to the bankruptcy, and can see from your assessment that they'll be wanting to take a substantial chunk. Your friend would need to ensure that every cost (aside from his husband's personal loan) was taken into account to maximise the amount of salary being kept, and keeping the contribution as low as possible. With increasing costs, it might be worth challenging some of the figures, but don't expect to have an 'emergency fund' of £1000 a month. Bankruptcy isn't 'party-time' where you get rid of your debts and immediately have lots of free money to play with. It does write-off the debts, but there is an expectation that the bankrupt continue to contribute. This is where the total level of debt needs to be considered. If it's £10k or £100k would make a difference in how to deal with it. The husband would also need to be supportive in that by going down this route - the loan would likely not be paid during the bankruptcy period. (As there'd be no available funds to do so)1

-

Debt is about £28k0

-

Was there a reason he went for bankruptcy over other debt solutions? Without knowing assets, etc, a DRO or DMP might have been an option?1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards