We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Deferred GMP and excess pension

Comments

-

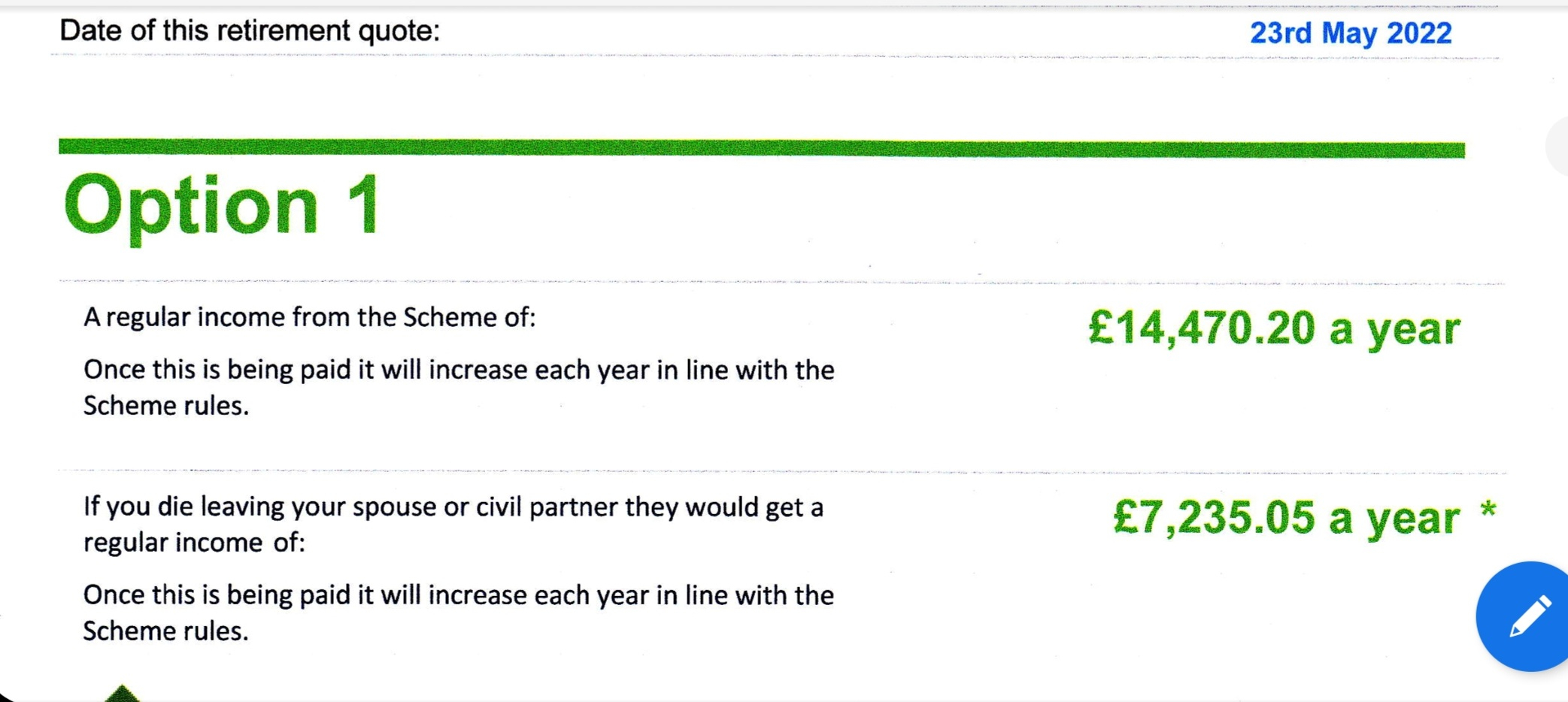

Thanks for the replies. Bear with me until I figure out how to quote part of your posts.I looked at the scheme booklet and there's no mention of state pension clawback. Phew!I've read Mr Floutiers figures and I've emailed the pension admins to clarify if I will get a step up at 65 (~£4k). If so fair enough, if not then straight to IRDP. They are likely to take a month to reply. I'll post back when they do.Their £14.4k is the retirement quote at my NRA 60 next month.Which I queried and they replied saying it was correct and furthermore implying it wouldn't increase at 65 either. Hence my original post.

2

2 -

Do let us know how the situation develops.0

-

Its taken a lot of to-ing and fro-ing and an IDRP to get this not very definitive answer. They don't seem to want to commit to a step up at 65!For members with Guaranteed Minimum Pension (GMP), ‘anti-franking’ legislation requires a certain minimum pension to be in payment at GMP Payment Age (65 for men, 60 for women). Schemes should test whether this minimum is met when a member reaches GMP Payment Age. If the pension in payment at GMP Payment Age does not meet the required minimum, then an uplift is awarded to the member.For members who are retiring on their normal retirement age where this is earlier than their GMP Payment Age, the test is carried out at GMP Payment Age, as required under the legislation. If the pension is below the anti-franking minimum, then it will be increased at that point to the minimum amount. This does mean that the pension can “step up” in this way several years after they retire.In your own case, were you to retire at your normal retirement age (age 60) then at your GMP Payment Age (age 65) your pension would be tested against this minimum, which takes account of the GMP revaluation due on your GMP. However, the Scheme rules and the anti-franking legislation allow the uplift for GMP revaluation to be offset against certain elements of your pension (primarily any annual increases you have already received between retirement and your GMP Payment Age) so your total pension may not be uplifted by the same amount as GMP revaluation. In some circumstances all of the GMP revaluation may be offset.

Surely, given that the increase to the excess is offset against the GMP revaluation it should be possible to provide an exact figure at 65? £18307.64 according to my calculations. Is it unreasonable to expect this in the retirement quote?

0 -

However, the Scheme rules and the anti-franking legislation allow the uplift for GMP revaluation to be offset against certain elements of your pension (primarily any annual increases you have already received between retirement and your GMP Payment Age)

Isn't this what Mike F describes in the previous linked posts?

it should be possible to provide an exact figure at 65?But how can this be done if the revaluation percentage for future years is unknown?

You will note that Mike was given an illustration based on an estimated 2.5%.

0 -

Unfortunately not, as no-one yet knows what the pension increases you will get between ages 60 and 65 will be.Surely, given that the increase to the excess is offset against the GMP revaluation it should be possible to provide an exact figure at 65? £18307.64 according to my calculations. Is it unreasonable to expect this in the retirement quote?

Even if the GMP Revaluation is known (which it might be if it's increasing at a Fixed Rate) the amount deducted isn't.0 -

Exactly, they just repeated back what I told them from what you told me here! They can't frank the whole of the GMP revaluation, just an amount equal to the increase in the excess between 60 and 65.xylophone said:However, the Scheme rules and the anti-franking legislation allow the uplift for GMP revaluation to be offset against certain elements of your pension (primarily any annual increases you have already received between retirement and your GMP Payment Age)Isn't this what Mike F describes in the previous linked posts?

it should be possible to provide an exact figure at 65?But how can this be done if the revaluation percentage for future years is unknown?

You will note that Mike was given an illustration based on an estimated 2.5%.

It should be possible to calculate since the excess returns back to what it was at NRA 60 so the CPI between 60 and 65 is irrelevant and the GMP is revalued at a fixed 6.25% each year.

0 -

I've managed to get the following via a DSAR which confirms my calculation, but it's not clear if I'm affected by the first coverage test. Any ideas?

0

0 -

Generally speaking, the GMP coverage test applies in more scenarios than the anti-franking test, but is less generous. By which I mean "technically the test will apply, but it won't matter for you because the anti-franking uplift will mean you will automatically pass it".1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.8K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.4K Mortgages, Homes & Bills

- 178.2K Life & Family

- 260.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards