We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Losing guaranteed benefits from a pension transfer

I recently found out that i had a (very) small pension plan with Aviva from a past employer which i'm now looking to transfer over to my Vanguard SIPP. The value of the Aviva pension fund is £3,073, but including 'Post 97 accrued benefits with an RST underpin' totals £5,180. Aviva told me a few weeks ago that the 'guaranteed transfer value' would include the accrued benefits, so £5,180 in total.

Vanguard have just sent me documents stating:

Your existing policy contains guaranteed benefits which will be given up once you transfer to us. We therefore require you to sign and return the enclosed declaration. By signing the declaration, you are agreeing, upon transfer to your Vanguard Personal Pension to waive the guaranteed benefits associated with your existing pension policy. We recommend that you get financial advice to help you make the best decision for your financial situation.

Does anyone know what the 'guaranteed benefits' are that i'm waivering by signing the Vanguard transfer document? Is it relating to the accrued benefits and do i therefore stand to lose the additional £2,107 in my Aviva fund, or are the benefits Vanguard mentions related to something else?

Comments

-

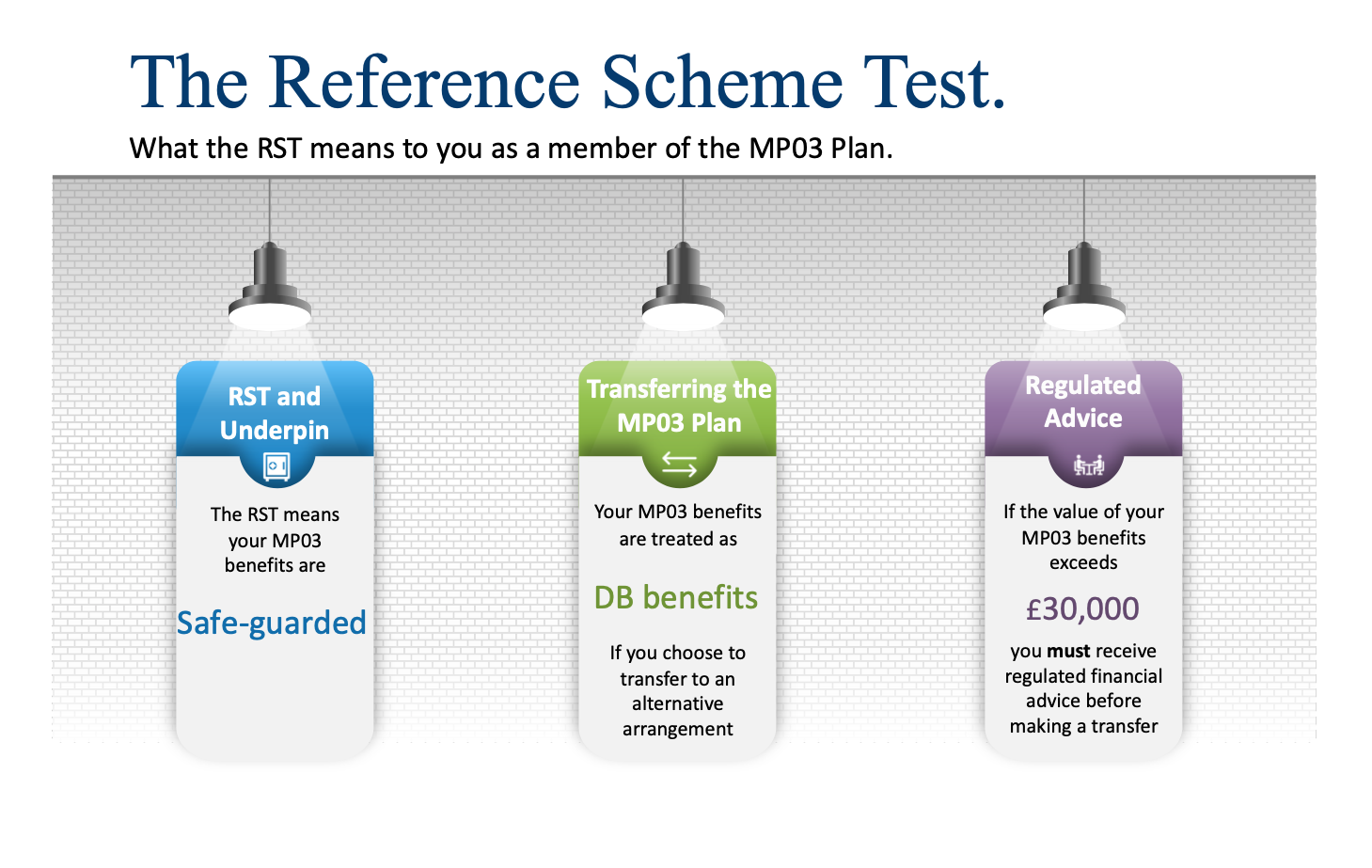

'RST' stands for Reference Scheme Test. What you are giving up is the certainty that your post 97 accrued benefits will be at least equal to the underpin provided in your current scheme. In lay terms, if you transfer and the value of your pot drops through the floor, tough!shoe_dog said:Hi

I recently found out that i had a (very) small pension plan with Aviva from a past employer which i'm now looking to transfer over to my Vanguard SIPP. The value of the Aviva pension fund is £3,073, but including 'Post 97 accrued benefits with an RST underpin' totals £5,180. Aviva told me a few weeks ago that the 'guaranteed transfer value' would include the accrued benefits, so £5,180 in total.

Vanguard have just sent me documents stating:Your existing policy contains guaranteed benefits which will be given up once you transfer to us. We therefore require you to sign and return the enclosed declaration. By signing the declaration, you are agreeing, upon transfer to your Vanguard Personal Pension to waive the guaranteed benefits associated with your existing pension policy. We recommend that you get financial advice to help you make the best decision for your financial situation.

Does anyone know what the 'guaranteed benefits' are that i'm waivering by signing the Vanguard transfer document? Is it relating to the accrued benefits and do i therefore stand to lose the additional £2,107 in my Aviva fund, or are the benefits Vanguard mentions related to something else?

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!1 -

You should at least find out what the underpin is. That way you will know what you are giving up and whether the alternative if viable or not.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

Does anyone know what the 'guaranteed benefits' are that i'm waivering by signing the Vanguard transfer document?

It would appear that you were a member of a "hybrid" occupational pension scheme - in your case this seems to have been a Defined Contribution Scheme which had a Defined Benefit contracted out element.

For example, the Scheme rules might have provided that where a member's pension at retirement was less than the value of the RST benefits, his fund would be increased to the level which would purchase the equivalent of the RST benefits.

The reference scheme test (the statutory standard), was applied to schemes that contracted-out of the state system. This test required a scheme to provide a pension at age 65, to have an accrual rate of 1/80th of qualifying earnings in the last three years before the end of contracted-out employment, and to pay a survivor’s pension to a widow, widower or civil partner of 50 per cent of benefits that the member was being paid before death.

0 -

I thought providers such as Aviva had a duty to send you a document called a 'safeguarded-flexible benefits risk warning' when people are looking to transfer benefits like these (ie pensions look like normal DC pensions but also have a guarantee.) I think the document is supposed to include an illustration so that you know what you'd be giving up.0

-

I’d leave well alone at the moment, share prices are on the floor.0

-

In fact they did, a 4 page document called 'RST Leaflet' (screenshots attached) but to be honest i find it hard to understand what it's explaining.sandsy said:I thought providers such as Aviva had a duty to send you a document called a 'safeguarded-flexible benefits risk warning' when people are looking to transfer benefits like these (ie pensions look like normal DC pensions but also have a guarantee.) I think the document is supposed to include an illustration so that you know what you'd be giving up.

0 -

The £3k is currently invested in the Aviva Pension BlackRock Blended Global Equity XE, is that better than transferring the £5k over to my Vanguard SIPP where i currently have 100% invested in the FTSE Global All Cap Index Fund?Hippycamper said:I’d leave well alone at the moment, share prices are on the floor.

I'm 20–25 years away from retirement, do current share prices matter that much if i'm effectively selling low and buying low?0 -

If you cannot answer the question yourself then why are you attempting to transfer it?The £3k is currently invested in the Aviva Pension BlackRock Blended Global Equity XE, is that better than transferring the £5k over to my Vanguard SIPP where i currently have 100% invested in the FTSE Global All Cap Index Fund?

At the moment, you appear to be wanting to transfer out of a pension with a potentially valuable guarantee invested in a tracker fund to a pension without a guarantee using a tracker fund.Would my Vanguard SIPP have an underpin in place? I only started it recently.Vanguard's pension is a type that would not have any safeguarded benefits.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

Well for a couple of reasons (prior to the RST underpin issue)...dunstonh said:

If you cannot answer the question yourself then why are you attempting to transfer it?

1. To keep my pension 'all under one roof' as it were for ease of management

2. The Aviva fund appears to be more weighted towards UK investments (60:40), where i'd prefer a more global approach

So how do i work out what the 'potential' value of this guarantee is? I left the company in question 20+ years ago, only worked there for a few months anyway and the fund is only valued at £3k. Will this guarantee really be worth much?dunstonh said:

At the moment, you appear to be wanting to transfer out of a pension with a potentially valuable guarantee invested in a tracker fund to a pension without a guarantee using a tracker fund.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.8K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards