We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

We're aware that some users are currently experiencing errors on the Forum. Our tech team is working to resolve the issue. Thanks for your patience.

Default pension de-risking - good/bad? what would you do and how quickly?

RNV

Posts: 145 Forumite

Hello again,

Well, the time has probably come when I have to make a decision (rather than rely on a default) and I'm not ready for that (not enough knowledge and confidence) so asking for your opinions on how quickly I need to act if at all.

I'm in a default workplace Balanced Risk Pension Plan with Scottish Widows. With a targeted retirement age of 65 (whereas I plan/hope for 55; I left 65 deliberately so that not to down risk too quickly or at least until I know for sure that I go for it at 55).

I turned 50 a few days ago and today noticed a transfer of about 2% of the total units value from "Scottish Widows Pension Portfolio Two" (where I was 100% before) to "Scottish Widows Pension Portfolio Three". The summary of the portfolios are copied below. Considering my ambitious target (retirement at 55), would you consider this de-risking a good or bad idea?

A piece of info, which I think is relevant, is I'm currently at £300k, targeting min £500k at 55yo with £40k/year contributions for the next 5 years.

Thanks for your thoughts and time!

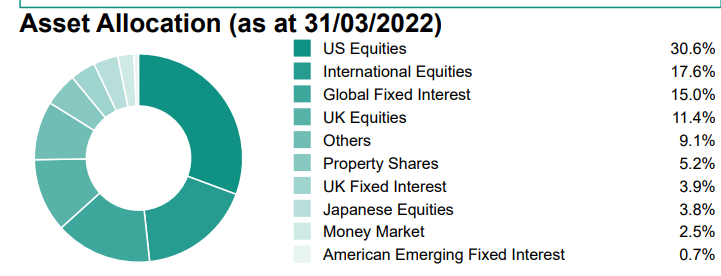

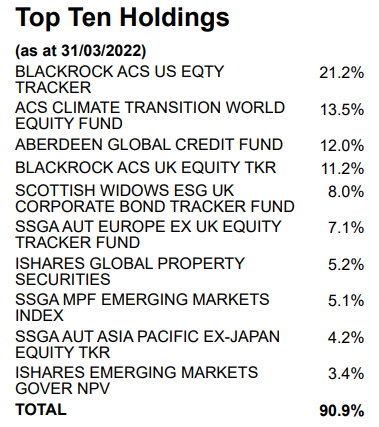

Portfolio 2

Portfolio 3

Well, the time has probably come when I have to make a decision (rather than rely on a default) and I'm not ready for that (not enough knowledge and confidence) so asking for your opinions on how quickly I need to act if at all.

I'm in a default workplace Balanced Risk Pension Plan with Scottish Widows. With a targeted retirement age of 65 (whereas I plan/hope for 55; I left 65 deliberately so that not to down risk too quickly or at least until I know for sure that I go for it at 55).

I turned 50 a few days ago and today noticed a transfer of about 2% of the total units value from "Scottish Widows Pension Portfolio Two" (where I was 100% before) to "Scottish Widows Pension Portfolio Three". The summary of the portfolios are copied below. Considering my ambitious target (retirement at 55), would you consider this de-risking a good or bad idea?

A piece of info, which I think is relevant, is I'm currently at £300k, targeting min £500k at 55yo with £40k/year contributions for the next 5 years.

Thanks for your thoughts and time!

Portfolio 2

Portfolio 3

0

Comments

-

The Portfolio 2 is a typical medium/high risk fund with nearly 80% equities- sometimes called high growth or dynamic or similar.

The Portfolio 3 is a typical medium risk fund with around 60% equities, often referred to as a balanced fund or a classic 60/40 fund.

It seems unlikely a 2% move from one to the other will have any discernible effect overall, one way or the other.

Couple of other comments.

Moving the retirement date on a product like this is a quick fix for the short term, but probably not ideal as a long term plan.

Managing your investments and drawdown after you retire ( especially at the young age of 55 and many years until sate pension helps) ) is generally thought to be more critical than before you retire ( mainly because you still have job income if something goes wrong ). £500K is a lot of money to manage, and probably would be a good idea to get a bit more knowledgeable over the next 5 years. I think many on this forum have probably done the same post 50, including me. As retirement comes on the horizon the motivation to learn more about pensions, investments etc gets stronger !1 -

Default pension de-risking - good/bad? what would you do and how quickly?You may or may not need to de-risk.

What are your plans for retirement? i.e. drawdown or annuity? If drawdown, what type of drawdown and how do you intend to draw?

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

Thanks for the comments.

I think I would probably (rightly or wrongly) prefer to remain in a higher risk for a bit longer. Agree that 2% is neither here nor there but I will check how my next contribution is allocated (should see it within a few days) and if all goes to Portfolio 3 I may have to force myself to click a few buttons on SW site.

Reason for this higher risk attitude is mainly:

a) going at 55 is a "want", if have to (if all goes wrong) I will stay in employment longer. However, if not all goes wrong - this higher risk may bring an extra reward.

b) we are in a fortunate position as a family to have other incomes/assets. So this is "my own" income/financial freedom if you wish, the family will be affected, of course, if I mess up but these will be relative luxuries rather than "food or heat"

What I'm currently thinking is definitely not an annuity (at least def. not until 70) but drawdown. Prob. with a portion of 25% tax free only for the first year/two until I clearly see that full retirement is working mentally and financially and I do not need to go back to work.0 -

If drawdown, then you are going to be investing for another 25-30 years. So, derisking is not necessary. Although if you are higher risk to begin with, some people lower it a notch or two on retirement. Any cash being drawn should be derisked about 3-5 years before it is drawn (depending on your risk profile)

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

I may have to force myself to click a few buttons on SW site.

Like most things, the more you do it the easier it gets

") 1

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards