We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Working out state pension amounts

My 60 year old husband has only 14 years full NI years which is very worrying. He will probably work for as long as he possibly can but realistically as a self-employed builder it is unlikely he would be able to work much longer than state retirement age. We don’t have a lot of money but if we could pay for a couple of years extra contributions how much would that affect how much he would get? Equally if he deferred for say 3 years how would that affect things? Are there mathematical equations used to work out those figures?

Thanks in advance

Jane

Comments

-

If he buys post 2016 years each one will add £5.29/week to his State Pension. So very good value for money.

NB. He cannot exceed £185.15 so the final year may not be as good value.

Deferment adds 5.8% to what he has accrued at his State Pension age. This is less clear cut a choice but not to be discounted.

Have you/he checked his forecast on gov.uk and if so which years are available to buy?

As a self employed person I presume he is completing Self Assessment returns and is paying Class 2 NI which is amazing value for money.

It might be useful for you to post the forecast and his NI history then you will get some helpful responses.1 -

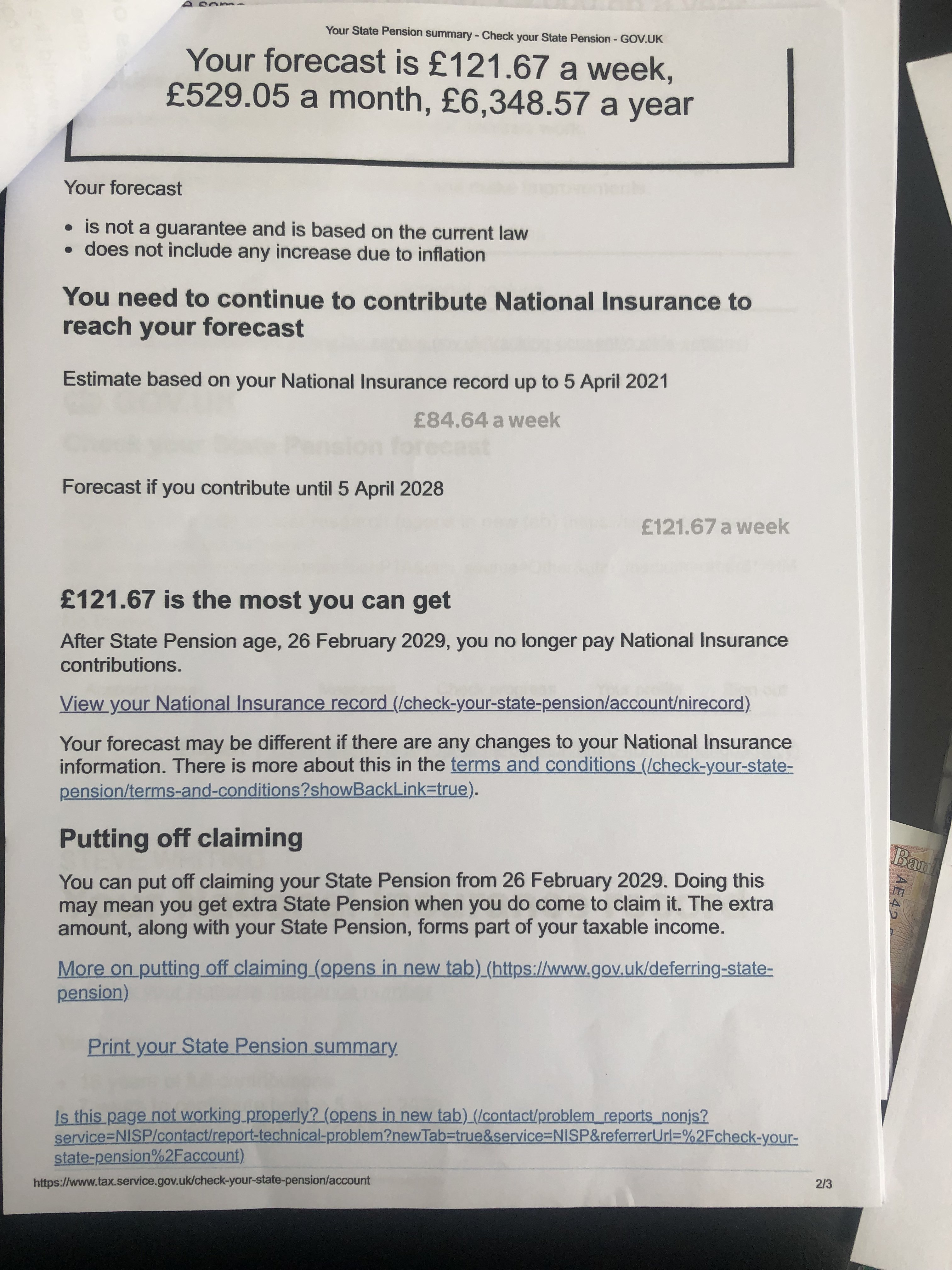

Thanks for replying. I have just looked again and he has 16 years of full contributions and is forecasted to get £121.67 in 2028. He is missing all years before 2008 and is also missing 2012/13, 2013/14, and 2014/15. Since the 2014/15 he has had full years - can you not buy years before 2016? It’s all looking very bleak.Dazed_and_C0nfused said:If he buys post 2016 years each one will add £5.29/week to his State Pension. So very good value for money.

NB. He cannot exceed £185.15 so the final year may not be as good value.

Deferment adds 5.8% to what he has accrued at his State Pension age. This is less clear cut a choice but not to be discounted.

Have you/he checked his forecast on gov.uk and if so which years are available to buy?

As a self employed person I presume he is completing Self Assessment returns and is paying Class 2 NI which is amazing value for money.

It might be useful for you to post the forecast and his NI history then you will get some helpful responses.0 -

You can currently buy years back to 2006-07. The ability to purchase 2006-07 to 2016-17 ends next April so needs to be looked at before then. They should be available at the class 2 rate - around £160 per year - so well worth looking into. He needs to contact the Future Pension Centre for his options. https://www.gov.uk/future-pension-centre Each of those years have the potential to add £5.29 per week to his pension so not to be sniffed at.What are all the figures from the front page of the forecast ?

0 -

@moleratmolerat said:You can currently buy years back to 2006-07. The ability to purchase 2006-07 to 2017-18 ends next April so needs to be looked at before then. They should be available at the class 2 rate so well worth looking into. He needs to contact the Future Pension Centre for his options. Each of those years have the potential to add £5.29 per week to his pension so not to be sniffed at.

Really !?! I'd been told you couldn't buy prior to 2016. Can you link something as this might effect my OH's SP?I’m a Forum Ambassador and I support the Forum Team on Debt Free Wannabe, Old Style Money Saving and Pensions boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.

Click on this link for a Statement of Accounts that can be posted on the DebtFree Wannabe board: https://lemonfool.co.uk/financecalculators/soa.php

Check your state pension on: Check your State Pension forecast - GOV.UK

"Never retract, never explain, never apologise; get things done and let them howl.” Nellie McClung

⭐️🏅😇🏅🏅🏅🏅0 -

See (and read very carefully)

https://www.moneysavingexpert.com/savings/voluntary-national-insurance-contributions/

Your husband should ring the Future Pensions Centre as soon as possible to get advice on his situation.0800 731 0175

https://www.royallondon.com/siteassets/site-docs/media-centre/good-with-your-money-guides/gwymg-1b-topping-up-state-pension-2019-interactive.pdf

may also be of interest but this guide has not been updated since.1 -

Brie said:

@moleratmolerat said:You can currently buy years back to 2006-07. The ability to purchase 2006-07 to 2016-17 ends next April so needs to be looked at before then. They should be available at the class 2 rate so well worth looking into. He needs to contact the Future Pension Centre for his options. Each of those years have the potential to add £5.29 per week to his pension so not to be sniffed at.

Really !?! I'd been told you couldn't buy prior to 2016. Can you link something as this might effect my OH's SP?Paying back to 2006-07 was introduced as part of the transitional measures with the introduction of the 2016 pension so that everyone had the opportunity to gain the minimum 10 years needed. For timeline purposes, the 2 & 6 year rule, they were all treated as 2016-17 with prices frozen until April 2019 and expiring in April 2023.Eligibility

You must be eligible to pay voluntary National Insurance contributions for the time that the contributions cover.

You can usually only pay for gaps in your National Insurance record from the past 6 years.

You can sometimes pay for gaps from more than 6 years ago depending on your age.

If you’re a man born after 5 April 1951 or a woman born after 5 April 1953

You may be able to pay voluntary contributions by 5 April 2023 to make up for gaps between 6 April 2006 and 5 April 2016 if you’re eligible.

You’ll pay the current rate.

1 -

Hi molerat - the front page shows the following - would it be possible to buy them at the class 2 rate? If so that would be wonderful even if we managed a couple it would be worth doing

0

0 -

That is interesting as it doesn't give an amount with purchasing back years, there is usually a third amount with filling prior gaps. Does it give costs to fill those gap years in the NI record ? If those 5 post 2006 gaps could be filled then that could take him to £148.11. Definitely a case for speaking to the FPC to clarify the situation.

0 -

Definitely a case for speaking to the FPC.

Indeed - and see my post above.

Has her husband always been self employed?

In second link page 7

How to work out if you have gaps in your National Insurance record which can be filled

If you have gaps in your National Insurance (NI) record you may be able to make up the gaps, and

so increase your State Pension, by paying voluntary National Insurance contributions (NICs). However, you can’t fill a gap if, in the year in question, you were:• over State Pension age at any point or

• eligible to pay the special reduced ‘married woman’srate’ of National Insurance for that year, or

• exempt from paying NI as a self-employed person because you held a low earnings exception certificate. However, you may be able to pay voluntary Class

2 NICs – the special category of NI for the self-employed – and the cost of this is just £3per week at 2019/20 rates.

Provided that you don’t fit in any of the above categories and that the deadline has not passed, you can buy back as many ‘missing’ years as you wish.

1 -

No, it gives no other figures - I will definitely get him to call FPC - thanks again for your helpmolerat said:That is interesting as it doesn't give an amount with purchasing back years, there is usually a third amount with filling prior gaps. Does it give costs to fill those gap years in the NI record ? If those 5 post 2006 gaps could be filled then that could take him to £148.11. Definitely a case for speaking to the FPC to clarify the situation.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards