We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Appreciate your views please .

My (our) finances are

Wife has full state pension with full years and I have two years left for full state pension.

My wife is 56 employed £21k part time and pays 6% (which employer puts in 16%)salary sacrifice to her DC pension ,pot stands around £100k at this time ,she also has DB pension of around £4K a year if taken now .

We have a mortgage of £37k left at 2% interest due to finish sept24 (house value around £600k)We are discussing options about her increasing her s/s to 40/50 % of her income , this will lower her tax bill I take it ? Or would putting some money into a stock & shares ISA be a better option ?

I’ve taken my pension earlier than anticipated due to the last couple of years and want to reduce my work hours . We want to enjoy some of the tax free but invest £20k in something that is better than a bank account rate 🤔 Ideally wife wants to retire in the next 5 years .

We would appreciate any ideas you may have .

Comments

-

Your wife can’t SS more than would reduce salary below National Minimum Wage £9.50 per hour, she should SS to this limit. You and her should then make the maximum pension contributions you can afford using up your lump sum and any other savings to a SIPP Pension beats ISA all day long.1

-

Are you a sole trader or a limited company? Pension payment options differ.Tony4625 said:I’m self employed and will be earning about £15-20 k ish per year after reducing my hours.

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.0 -

-

but invest £20k in something that is better than a bank account rate

Had you considered paying off £20k of the mortgage and contributing the money saved to a pension?

0 -

When do you want to retire? If it is before SPA you’ll have some unused personal allowance unless you have a SIPP already so maybe worth looking at that.

If your wife salary sacrifices 50% unless she has other income she’ll pay no tax as she’ll be below personal allowance.

What is your number for retirement and how do you aim to meet that prior to SPA?0 -

Which means she effectively gets no tax relief on part of the contributions.DT2001 said:When do you want to retire? If it is before SPA you’ll have some unused personal allowance unless you have a SIPP already so maybe worth looking at that.

If your wife salary sacrifices 50% unless she has other income she’ll pay no tax as she’ll be below personal allowance.

What is your number for retirement and how do you aim to meet that prior to SPA?

It would mean you (as a couple) may then be able to benefit from Marriage Allowance but I'm not sure sacrificing pay to save NI but no tax is as good an option as a lower sacrifice and then making personal contributions to a (relief at source) pension where she will get basic rate tax relief added despite not necessarily paying any tax herself.0 -

Or would putting some money into a stock & shares ISA be a better option ?

To be clear you can have the same ( or similar) investments in a S&S ISA and a DC pension/SIPP .

The pension has a tax advantage but the disadvantage is that the money is tied up until you are 55 . As you are both have already reached this age , then this disadvantage disappears.

You have not mentioned how her pension is invested ? Is this something you have actually looked into ( many people do not ) ?

0 -

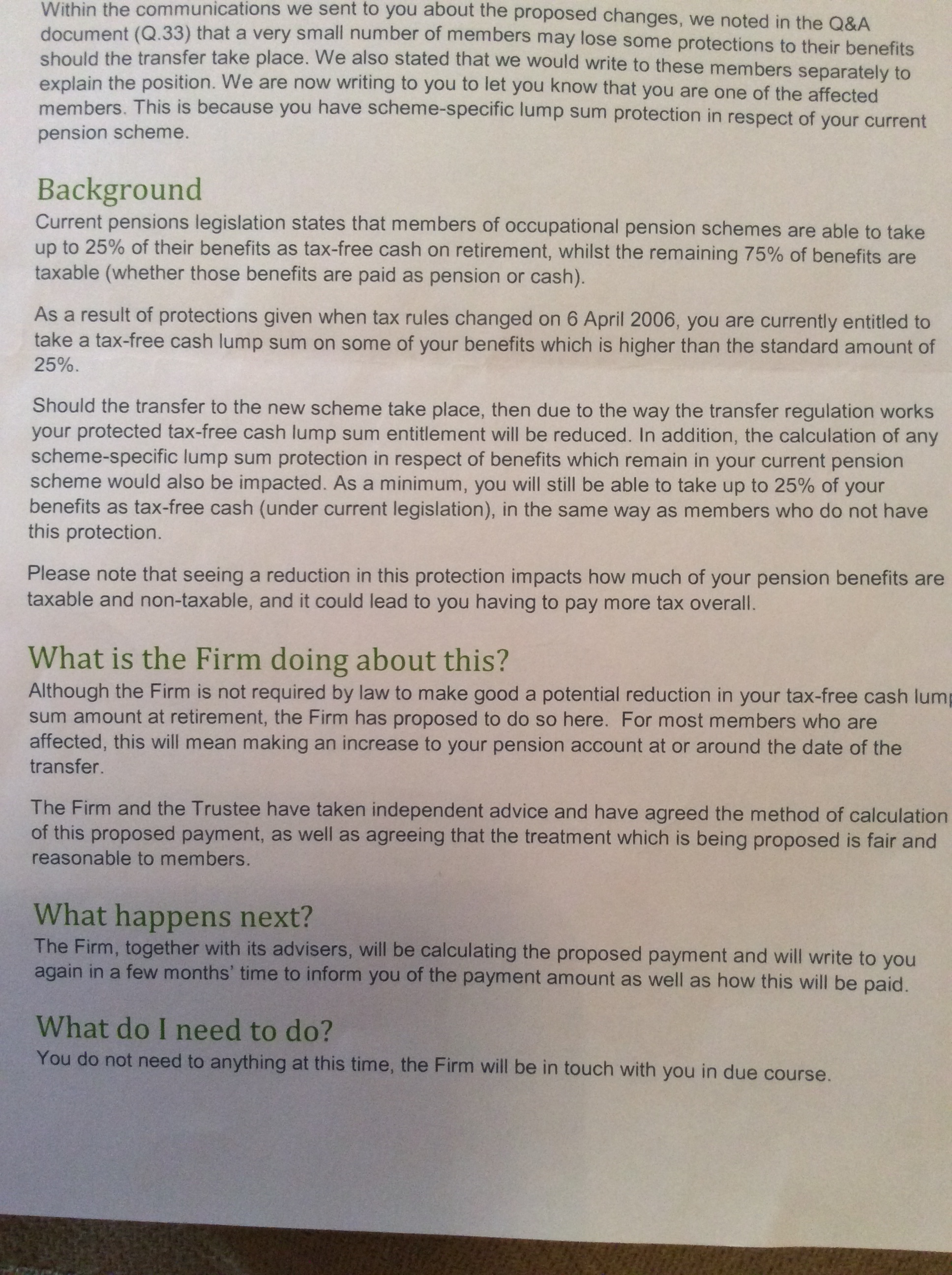

Thanks for your reply , my wife’s DC pension is in the process of being moved (by her firm ) to a L&G work / master trust . The consultation period is complete and will switch soon . She needs to decide what to invest in or just go into the default selection . She also received this letter concerning her tax free lump sum guarantee; looks like she would have been entitled to more than 25% tax free ?Albermarle said:Or would putting some money into a stock & shares ISA be a better option ?To be clear you can have the same ( or similar) investments in a S&S ISA and a DC pension/SIPP .

The pension has a tax advantage but the disadvantage is that the money is tied up until you are 55 . As you are both have already reached this age , then this disadvantage disappears.

You have not mentioned how her pension is invested ? Is this something you have actually looked into ( many people do not ) ?

0

0 -

Yes it does , but not clear how much more than 25%. Probably not a large % more . Anyway it seems there will be some compensation for the loss , so probably not a big deal .Tony4625 said:

Thanks for your reply , my wife’s DC pension is in the process of being moved (by her firm ) to a L&G work / master trust . The consultation period is complete and will switch soon . She needs to decide what to invest in or just go into the default selection . She also received this letter concerning her tax free lump sum guarantee; looks like she would have been entitled to more than 25% tax free ?Albermarle said:Or would putting some money into a stock & shares ISA be a better option ?To be clear you can have the same ( or similar) investments in a S&S ISA and a DC pension/SIPP .

The pension has a tax advantage but the disadvantage is that the money is tied up until you are 55 . As you are both have already reached this age , then this disadvantage disappears.

You have not mentioned how her pension is invested ? Is this something you have actually looked into ( many people do not ) ?

Regarding the investment , there are typically two types of default fund . One is a medium risk , middle of the road type fund . Usually around 50 to 60% equity content, although there is some variability from provider to provider. The other type is a so called Lifestyle default fund ( sometimes have different names ) that derisks as you approach retirement age . Two things to watch with these. They seem generally to derisk too much, especially if you intend keeping the pension for many years. They use a retirement date that is in their system , that you can change . This may or may not be when you actually intend to retire.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards