We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

65k in 65m

Comments

-

You are doing an incredible job of paying this down. I hope you take some time to appreciate that each month!2

-

MatyMoo - haha yes I suppose that's what I should be doing. Unfortunately I have a sweet tooth and a full blown sugar addiction so anything left in the travel pot at the end of the month gets spent on treats! The only double whammy here is to my hips lol

savingholmes - it is indeed. It was a bit anticlimactic when I finally filled it, but I filled it and that's what matters!

Viking_mfw - oh yes to the appreciation! It's so very satisfying seeing the numbers in the balance tumble away with each DD taken and each OP made, onwards and downwards we go!

Thanks for your comments! (:I want to be 30 and debt free and thriving1 -

Month 18:

So, a whole year has passed since I finally moved into my house, after some of the worst and most stressful moments of my life. I knew things would get better, and they have, but I don't really know how to feel at the moment with everything that's going on.

One one hand, I feel happy that I am in a relatively good place financially, and then on the other, I feel guilty about it because I'm doing OK when others aren't. If anything, I'm steadily becoming better off each month, all the more so at the moment because of overtime. But I live in one of the most deprived areas of the country, and I see the struggle that many face firsthand. It's getting worse, no doubt about it, and it seems like it's going to continue that way. Just yesterday I was reading about 'warm banks' being set up. In one of the richest countries in the world.

I've been inspired by others online to donate the £150 council tax rebate to the foodbank, along with the £400 energy bill credit. I feel a little horrid that I'll be doing it not out of the goodness of my heart or to be charitable, but to ease my guilt. I'm justifying it to myself though because it's still something, and that's better than nothing.

For the time being, I will continue to do as much overtime as I can. As they say, make hay whilst the sun is shining. Winter is coming.

Bottom line:

£49400 owed

£15600 / £65000 cleared

Emergency fund: £4485 / £3000

I want to be 30 and debt free and thriving3 -

While it's good you can manage your mortgage debt - it's still debt and I'd prioritise either clearing that or building up pension or both. I wouldn't feel bad for working hard to put yourself in a good financial position. I don't understand why you would feel guilty.

If you want to give - give - but doing it out of guilt seems misplaced. Not sure if I am explaining myself well enough...

Achieve FIRE/Mortgage Neutrality in 2030

1) MFW Nov 21 £202K now £169.8K Equity 37.1%

2) £2.4K Net savings after CCs March 26 (but owed £1.1K) so £3.5K

3) Mortgage neutral by 06/30 (AVC £36.2K + Lump Sums DB £4.6K + (25% of SIPP 1.3K) = 42.1£127.5K target 33% 27/2/26 (If took bigger lump sum = 64K or 50.1%)

4) FI Age 60 income target £17.1/30K 57% (if mortgage and debts repaid - need more otherwise) (If bigger lump sum £15.8/30K 52.67%)

5) SIPP £5.2K updated 16/1/263 -

savingholmes - you're quite right. I've reread what I wrote and don't think I made much sense lol. I'm just in some sort of funk that I can't shake off with everything that's going on at the moment. Think a bit of time off to relax and self-care is much needed.

I want to be 30 and debt free and thriving2 -

Month 19:

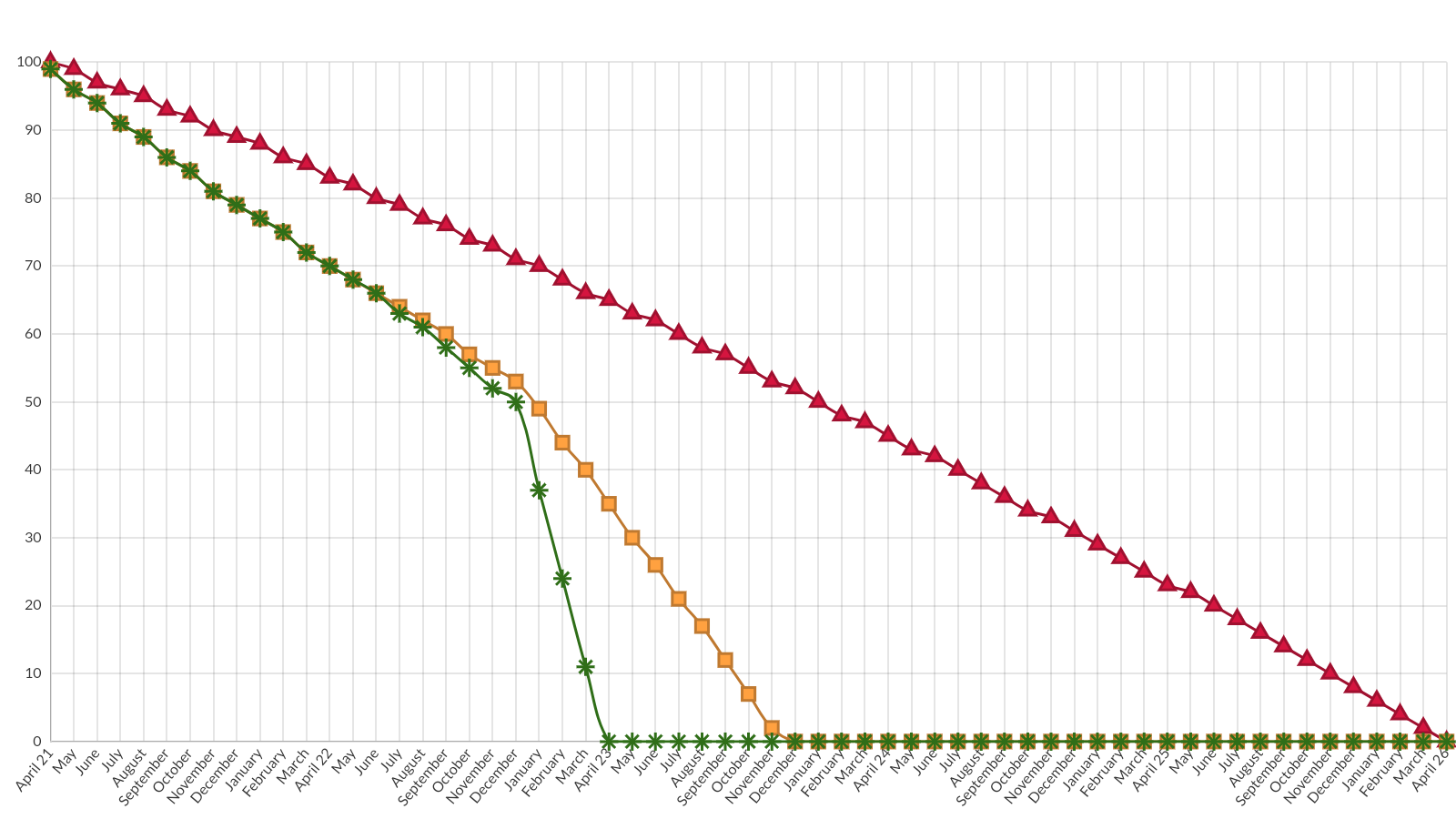

So, I finally opened up my spreadsheet to work out just how much quicker I can pay off my loan, now that I have a full emergency fund with a surplus. And it's very good news:

(y-axis is % paid off)

The amber line was my original plan, to overpay steadily whilst continuing to grow my savings, to clear the loan by December 2023. The green line is my new plan, which actually broke off from the original this July when I upped my overpayments. But the main difference is that I will hit half the loan paid off this December, and then I've decided to clear the remaining half in the following four months, in April 2023. So two years after taking out the loan it will be repaid in full! It will come at the cost of my outgoings exceeding my income for those four months, eating into the emergency fund I've painstakingly built up, but that's a price I'm willing to pay.

The interest paid under the green line will be £1000, yes really. The difference between the green and amber line is an additional £135 in interest. That saving isn't anything to write home about, but for me the bigger saving will be the eight months knocked off the term. This loan has given me so much stress, more than the mortgage and that's for a heck of a lot more! Whenever I open the bank app I see my current account and then below that is the loan account, almost taunting me. For some reason I have this irrational fear that at any moment the bank is going to raid my current account and put it towards the loan so that they get their money back quicker. I realise how daft that seems after writing it haha. Thank goodness the mortgage is with a totally separate lender otherwise I don't think I'd be able to function! Anyway, just another six months to worry like this and then it'll be paid off and gone forever. I can't wait!

The red line in the graph is the repayment schedule in the loan contract. A full 5 year term with the full £1985 in interest. That was never going to happen (:

Bottom line:

£46815 owed

£16385 / £65000 cleared

Emergency fund: £4875 / £3000

I want to be 30 and debt free and thriving3 -

Lovely to be so close to finished.Achieve FIRE/Mortgage Neutrality in 2030

1) MFW Nov 21 £202K now £169.8K Equity 37.1%

2) £2.4K Net savings after CCs March 26 (but owed £1.1K) so £3.5K

3) Mortgage neutral by 06/30 (AVC £36.2K + Lump Sums DB £4.6K + (25% of SIPP 1.3K) = 42.1£127.5K target 33% 27/2/26 (If took bigger lump sum = 64K or 50.1%)

4) FI Age 60 income target £17.1/30K 57% (if mortgage and debts repaid - need more otherwise) (If bigger lump sum £15.8/30K 52.67%)

5) SIPP £5.2K updated 16/1/262 -

Well done young man, when I was your age I was working overtime to pay off debts on credit cards and loan's. Gruelling as it was it taught me to look at money and interest in a different way. So grab the overtime whilst it's there, without it impacting your social life too much.

One thing getting older teaches you is... not everything goes to plan, and not everything has to go to plan.

You have a good fixed rate on your mortgage, were in a time where interest rates are on the up (finally for saver's). So you're in a strong position now, keep over paying bit also take advantage of some savings accounts like Barclay's rainy day saver, and have a look at switching bank accounts for "free" £150-200.

Another possibility of saving more on interest is use your emergency fund at the start of the mortgage year and pay the 10% limit off in one go, doing this will save you sizable interest over the fixed rate of your mortgage. Then pay what you would have paid in overpayments back into savings, rinse and repeat for the following years.

I loved playing with my spreadsheets for my mortgage, in the early years it was getting to milestones i.e. under £5 a day interest, or getting it under £70k, £60k etc.

The main one I looked forward to was getting to the half way mark of the fixed rate when overpaying like you do, that's when the debt really starts to snowballs down.

Keep it up2 -

In the previous update it should have said £48615 owed, not £46815. How'd I type that wrong, embarrassing xD

savingholmes - indeed, just 5 more months to go! Finish line is in sight and now it feels like this is no longer a marathon, it's a sprint lol

Coffeekup - thank you, lots of food for thought here! With regards to paying off the overpayment allowance in one go, that's definitely something I'm going to have a look at doing once I've cleared the loan and actually have enough saved to be able to do it lol.I want to be 30 and debt free and thriving1 -

Month 20:Happy Friday!I've seen in some diaries here that there are budgets and SOAs posted and I haven't done one yet so here is mine. I don't think there's anything that could be changed but then I've never discussed my finances with anybody so I don't really know any different!Income:£1600 (plus overtime)Outgoings: (all figures are averaged out and rounded)£900 - mortgage and loan (DDs and OPs)£325 - spending money*£110 - gas and electric (currently reduced by EBSS)£80 - council tax (single person discount)£25 - home insurance£20 - unlimited SIM plan£15 - water*£325 - I don't really have a strict budget for this, but it's usually £150 for food and general expenditure, £70 bus, then the rest is fun money with £50 kept back in savings for unexpected expenses. It's the only money I spend out of my pay and it's worked well for the last few years, though I am feeling the tiniest of pinches now. In all honesty, I don't see this figure increasing whilst I still have debt. If push came to shove then I could decrease it, but I would be very reluctant to do so as it would have a significant impact on my quality of life.Leftover:£125 (plus overtime) - it all remains in the bank and adds to my emergency fund. I don't use or spend this money; the long-term plan is to put it towards paying off the mortgage once the 5-year fix ends.Debt:£47825 - total£20115 paid in 20 months£2940 interest (around half of the total interest to pay over 65 months)£17175 cleared (average of £860 per month so not yet on track for 65k in 65m)Savings:£5085 emergency fund£600 spending account£700 cash under mattress£100 cash in handBottom line:£47825 owed£17175 / £65000 clearedEmergency fund: £5085 / £3000I want to be 30 and debt free and thriving4

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.9K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.5K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards