We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Can someone help explain transfering into NHS?

MakingUpGround

Posts: 97 Forumite

I have a transfer figure to transfer in I'm trying to understand.

Its a private pension worth about 15.5k.

I have been offered 4 years worth of transfer. I'm part time admin, I think i build up about £225 pension per year. I'm only in the 2015 scheme.

So does this mean they are offering £900 per year?

Thank you

Its a private pension worth about 15.5k.

I have been offered 4 years worth of transfer. I'm part time admin, I think i build up about £225 pension per year. I'm only in the 2015 scheme.

So does this mean they are offering £900 per year?

Thank you

0

Comments

-

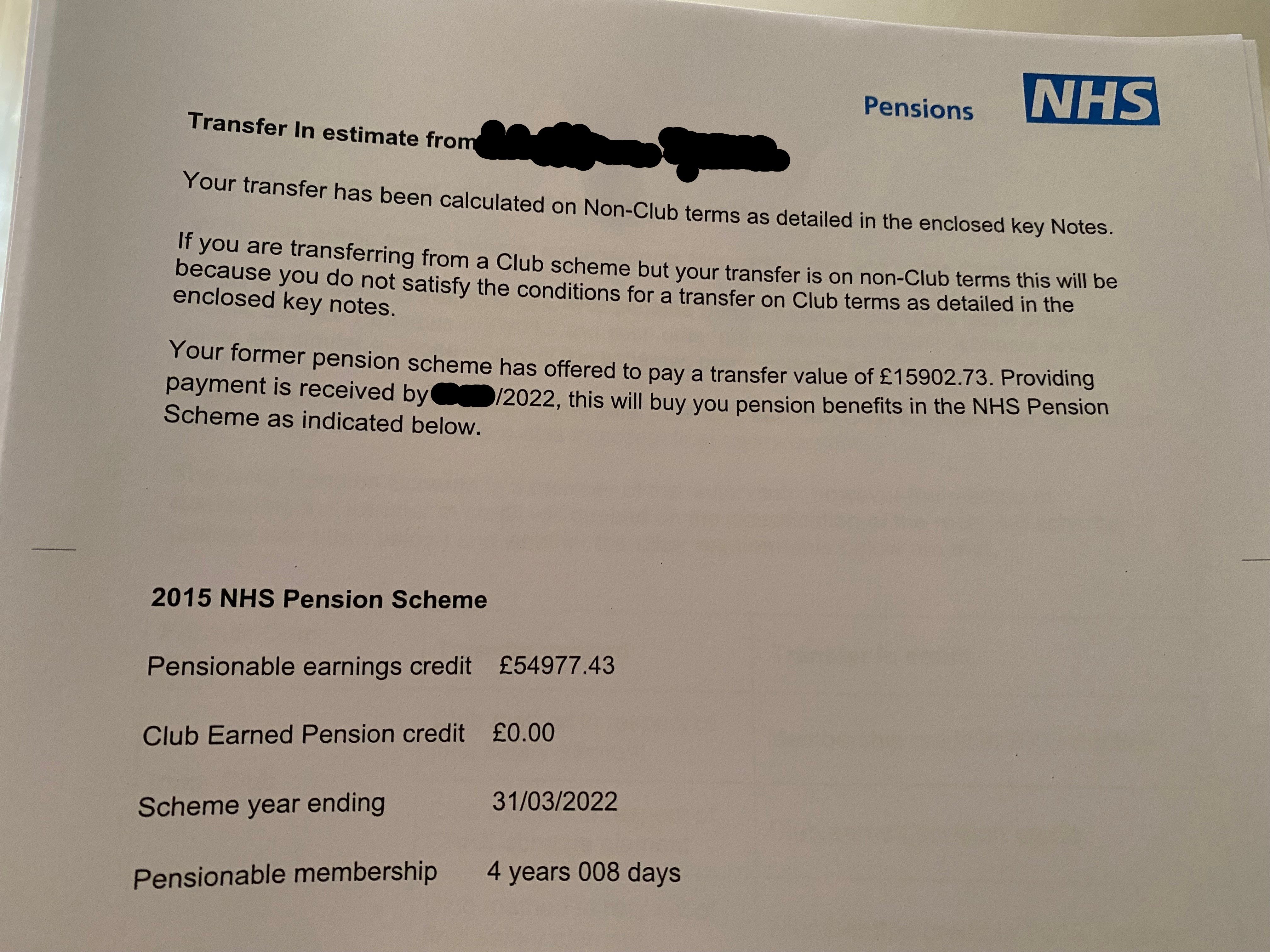

4 years worth seems a funny way of putting it. It should be a figure. If it’s £900 pension that means they will pay you £900 per year from your set retirement age. This is index linked so will increase with inflation (it maybe CPI +1.5% as per main benefits or just CPI as a transfer). You can take it earlier but will get less per year but for more years.Annual pension of £225 says your paid £12150 per year (because NHS pension is accrued at the rate of 1/54ths).

I would take the offer if it is £900, you won’t have the chance to buy guaranteed retirement income again.0 -

What does the paperwork say specifically? As MX5huggy say, it seems odd that they offered years since it is normally it is fixed income you are buying after all. Always ask to double-check and clarify, do not assume anything about this.MakingUpGround said:I have a transfer figure to transfer in I'm trying to understand.

Its a private pension worth about 15.5k.

I have been offered 4 years worth of transfer. I'm part time admin, I think i build up about £225 pension per year. I'm only in the 2015 scheme.

So does this mean they are offering £900 per year?

Thank you0 -

The paperwork is more confusing! yes you are correct re my annual salary at around 12.15k.

But if I take this and my husband survives me he only gets a 1/3, whereas he'd have all the private pot left over?

That's my biggest worry as he has nothing above state pension at the moment

Yes, it says it increases by Treasury Orders plus 1.5%

I've only been with the NHS for 6 months so 4 years is not my existing membership

0 -

The 'pensionable membership' figure quoted isn't very material as it doesn't relate to actual pension, just if there's any subsidiary benefit where eligibility depends on length of membership.MakingUpGround said:

Yes, it says it increases by Treasury Orders plus 1.5%

I've only been with the NHS for 6 months so 4 years is not my existing membership

For a 'non-Club' transfer in like yours (i.e. you aren't transferring in from another public sector scheme), the transfer value purchases you notional pensionable pay to go with your actual pensionable pay from your first year in the NHS scheme. Given the NHS scheme's accrual and revaluation rates, this means from a CETV of £15902.72, you are purchasing an annual pension of 54977.43 x 1/54 = £1,018.10 pa that rises by CPI+1.5% on each 1st April while you remain an active member of the scheme, then by CPI at the start of each April once you are not. So were you to be 20 years an active member, that £1018.10 pa would have become £1,371.23 in today's money by the end, stay 30 years and it would become £1,591.37 in today's money,But if I take this and my husband survives me he only gets a 1/3, whereas he'd have all the private pot left over?We're talking about two very different things, a guaranteed annual income for life (indeed one that will increase by inflation each year) vs. a pot of money. If you were to die before the scheme's normal retirement age, then the survivor pension would also be 33.75% of the notional tier 2 ill health pension, not just 33.75% of your pension accrued and revalued to date.

3 -

The presentation follows how the scheme regulations specify the nature of the credit purchased by a non-Club transfer in (https://www.legislation.gov.uk/uksi/2015/94/regulation/143/made). Of course the statement could go beyond that, however I suppose from a presentational point of view giving an annual pension could be considered slightly misleading given the active member revaluation rate is important in determining the credit's final value.JoeCrystal said:

What does the paperwork say specifically? As MX5huggy say, it seems odd that they offered years since it is normally it is fixed income you are buying after all. Always ask to double-check and clarify, do not assume anything about this.MakingUpGround said:I have a transfer figure to transfer in I'm trying to understand.

Its a private pension worth about 15.5k.

I have been offered 4 years worth of transfer. I'm part time admin, I think i build up about £225 pension per year. I'm only in the 2015 scheme.

So does this mean they are offering £900 per year?

Thank you

That said, I would still show it personally, in the same way it was common to show the immediate impact of a reckonable service credit back in the final salary pension days...3 -

Thank you both, your insights help me make more sense of it.

I possibly have a different local government pension (very small) to transfer in as well.

I think I've realised if I didn't go back to local government employment within 5 years it automatically refunds me my contributions. At the moment it's in deferment and not increasing at all annually.

Will that change any of the above transfer?0 -

That would be a separate, Club transfer in. With a Club transfer, you keep the revaluation rate of the previous scheme, which is just CPI for the LGPS (compared to the NHS scheme, the LGPS has a better accrual rate instead of the better revaluation rate).MakingUpGround said:Thank you both, your insights help me make more sense of it.

I possibly have a different local government pension (very small) to transfer in as well.

I think I've realised if I didn't go back to local government employment within 5 years it automatically refunds me my contributions. At the moment it's in deferment and not increasing at all annually.

Will that change any of the above transfer?1 -

A refund is only on the cards if you have less than 2 years membership (the vesting period). A transfer to the NHS is a much better option than taking a refund of your own contributions (less tax).MakingUpGround said:Thank you both, your insights help me make more sense of it.

I possibly have a different local government pension (very small) to transfer in as well.

I think I've realised if I didn't go back to local government employment within 5 years it automatically refunds me my contributions. At the moment it's in deferment and not increasing at all annually.

Will that change any of the above transfer?

Transferring your LGPS benefits into the NHS won't stop or affect your private pension transfer in any way.

1 -

It will be increasing in line with (cpi) inflationMakingUpGround said:Thank you both, your insights help me make more sense of it.

I possibly have a different local government pension (very small) to transfer in as well.

I think I've realised if I didn't go back to local government employment within 5 years it automatically refunds me my contributions. At the moment it's in deferment and not increasing at all annually.

Will that change any of the above transfer?0 -

Thank you, yes, just realised the headline figure is what it started at, turn over to smaller print for what it is now!Andy_L said:

It will be increasing in line with (cpi) inflationMakingUpGround said:Thank you both, your insights help me make more sense of it.

I possibly have a different local government pension (very small) to transfer in as well.

I think I've realised if I didn't go back to local government employment within 5 years it automatically refunds me my contributions. At the moment it's in deferment and not increasing at all annually.

Will that change any of the above transfer?

Gosh pensions are sooo complicated0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards