We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Do I have enough ?

On paper things look OK but I'm a bit worried about inflation.

My pensions and investments are

DB pension of £4200 from 60

SIPP current value £310k

Investments and savings £590k

Looking to move to a better area which will require about £100k.

Spend about £20k or so a year.

Just wondering how much I could potentially draw before my state pension kicks in at 67. This forecast at £10500.

Comments

-

Looks like you have more than enough, as £800k still invested (including some savings) after £100k spend on property upgrade. At a conservative estimate you could drawdown 3% per annum (£24k) increasing with inflation and be okay. However you only need around 2% (£16k) to give you £20k pa in total after you start to receive your DB pension. You will need even less drawdown when you get your State Pension. So even with inflation rising I'm sure you will be absolutely fine.5

-

Suggest you do some research around Safe Withdrawal Rates from pension/investment pots .0

-

I've probably read all there is to read on safe withdrawal rates.

I've got a nasty feeling that we may be going into a protracted period of high inflation and negative to low stock market returns.

0 -

Even if that happens I think you have more than enough to meet your level of spend. You only need £16k plus inflation per year for 7 years spending from age 60. I don't know how much of your pot is in cash savings, but if you wanted to you could convert enough to cash to cover these 7 years spending. After you get your State Pension at 67 you will only need to drawdown around £4k plus inflation per year, so your remaining pot would easily be enough to cover such a low withdrawal rate.Pablootes said:I've probably read all there is to read on safe withdrawal rates.

I've got a nasty feeling that we may be going into a protracted period of high inflation and negative to low stock market returns.2 -

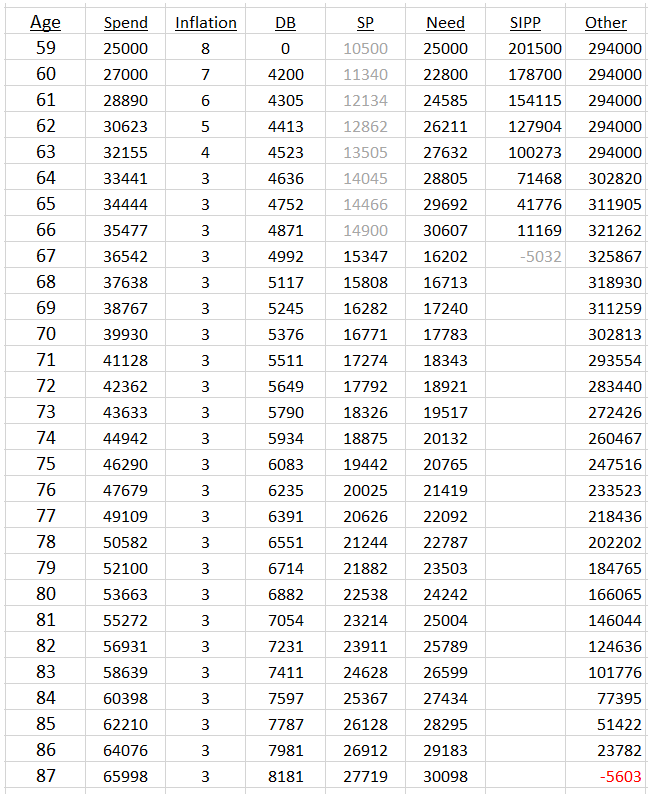

Just for kicks I ran the following scenario:

You spend 100k on moving house

The stock market collapses the next day and all of your investments lose 35%

They do not recover at all for 5 years, then grow at just 3% for the rest of your life

You spend 25k per year, increasing with inflation

Inflation runs rampant: 8% this year, then 7%, 6%, 5%, 4%, 3%, and never falls below 3%

Your DB is capped at 2.5% so it fails to keep up

In this apocalyptic scenario, you run out of money at age 87, which means you then have to live on just your DB and your SP. You could use equity release at that point, which would get you back about half the value of your house. Should see you through to 100 without too much trouble.

12 -

Thanks for this.

Looks like I'm OK then assuming that the government honours the triple lock.

0 -

The idea of a Safe Withdrawal Rate over a long period, takes into account that there will be maybe three or four difficult periods during the period.Pablootes said:I've probably read all there is to read on safe withdrawal rates.

I've got a nasty feeling that we may be going into a protracted period of high inflation and negative to low stock market returns.

The main worry is a big drop just as the period starts but if you have plenty of cash to cover this period , you do not have to sell investments at a loss.

Secret Second Account has kindly provided you with a worst case scenario, but more likely is that you could spend £30K pa, rather than £20K pa and pop your clogs at 90, with a large amount of money still left . Nothing is guaranteed of course but you have to work with some assumptions.

I suppose you have to ask your self how would you feel if you spent the early years of retirement , anxious about living off a modest £20K pa , and then later died with a Million pounds ( or more) still in the bank, and being maybe the richest man in the graveyard ?

Another alternative is buy a guaranteed lifetime annuity or even a fixed term annuity, although they are not great value for money at the moment.1 -

Does your £20k income requirement cover future costs such as a new car, boiler, house maintenance etc?0

-

If you are concerned total returns are going to be lower in future then look for natural yield and build the portfolio on that basis. Then draw less than the natural yield.

3% yield on £900k of investments is £27k a year. You may need to commit more of your savings to investments but that is not a bad thing. You can keep up annual pension contributions and S&S ISAs and have around £100k-£150k in a GIA without tax. (double up if you have a spouse).Just wondering how much I could potentially draw before my state pension kicks in at 67. This forecast at £10500.If you are funding the gap of £10,500 in 7 years time then its 7x10,500 in simple terms -£73,500. (depending on how close you are to 60 you may want to add some additional months and maybe round up to £80k for inflation.

It all seems very achievable with a bit of playing around with tax wrappers/risk levels.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2 -

My £20k spends includes a £3k pa contingency for boiler/car replacement etc1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards