We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Looking to start a pension - advice needed

Comments

-

So in terms of arriving at a decision (to kick things off at least) i think i'm going to opt for a 100% global equity investment. Whilst i appreciate some people like the UK bias in the Life Strategy funds, i'd personally prefer something more globally distributed.

Would committing 100% to a single global index i.e. the VG Global All Cap be considered a good option? Or should i be looking for a fund made up of multiple global index funds (so like the LS but without the UK bias)?

I think i read somewhere that it doesn't really matter if you're investing in a single index fund as opposed to a fund-of-funds as it's the underlying holdings that matter, of which the FTSE Global All Cap has over 7000 of. Am i right in thinking this?

Also, are there alternatives to the VG Global All Cap i should consider or is it a fairly safe bet for what i want to achieve?

Once i land the fund i can start looking at platforms.0 -

There is more than one type of 100% equity global index fund . However the differences between them are not large and their long term returns are similar. AFAIK the main difference is whether they contain a few % of Emerging market shares and there fore a little bit lower % of developed world shares ( so a a few % less in the US for example ).

These funds are also well known

Fidelity Index World Fund P Accumulation Key Statistics | GB00BJS8SJ34 | Fidelity

HSBC FTSE All-World Index Fund Accumulation C Key Statistics | GB00BMJJJF91 | Fidelity

0 -

Both of which charge about half as much as the Vanguard equivalents.Albermarle said:1 -

Is this with regards to the ongoing fund charge?Secret2ndAccount said:

Both of which charge about half as much as the Vanguard equivalents.Albermarle said:

So essentially on a £200,000 pension pot for example, the VG Global All Cap would cost me £460 (0.23%) a year vs. the HSBC FTSE All-World which would cost me £260 (0.13%) or the Fidelity Index World Fund which would cost me £240 (0.12%). Am i calculating that right?

In terms of the funds, the Fidelity and HSBC funds are Large Cap as opposed to All Cap, whilst i understand the meaning, what might the impact be - if any - on overall performance of an All Cap vs a Large Cap?0 -

Compare their performance using Trustnet , or one of the SIPP providers . You do not need to be a customer to see the investment fund info.0

-

Correct. £200/yr plus compound interest.bpk101 said:

So essentially on a £200,000 pension pot for example, the VG Global All Cap would cost me £460 (0.23%) a year vs. the HSBC FTSE All-World which would cost me £260 (0.13%) or the Fidelity Index World Fund which would cost me £240 (0.12%). Am i calculating that right?

In terms of the funds, the Fidelity and HSBC funds are Large Cap as opposed to All Cap, whilst i understand the meaning, what might the impact be - if any - on overall performance of an All Cap vs a Large Cap?

Albermarle said:

Compare their performance using Trustnet , or one of the SIPP providers . You do not need to be a customer to see the investment fund info.

I did create a chart to show the relative performance of the funds, but decided not to include it in my post. Here's why:

In recent years, megacap tech has been so successful that large cap has outperformed small-cap by a clear margin. However that hasn't always been the case. The theory is that it only takes just a couple of tiny companies to turn into huge companies, and you've made a massive profit - far outweighing the extra cost of holding the wider funds. The counter-argument is that the megacaps are now so large that it makes it hard for the tiny companies to get a foot-hold. The megacaps can spend almost any amount on advertising, recruiting, salaries, lobbying, research. And if they see a competitor making an impact, they often buy it and consume it before it becomes large enough to harm them.

Who knows what the future holds. If you have shares of many companies in many countries, you have covered your bases. I would suggest listening to people who say they can't be sure what's better than that, rather than anyone who says they can be sure to do better than that.

1 -

I've almost arrived at a decision and it's between the Vanguard Global All Cap fund and the Fidelity Index World fund but had one last question...

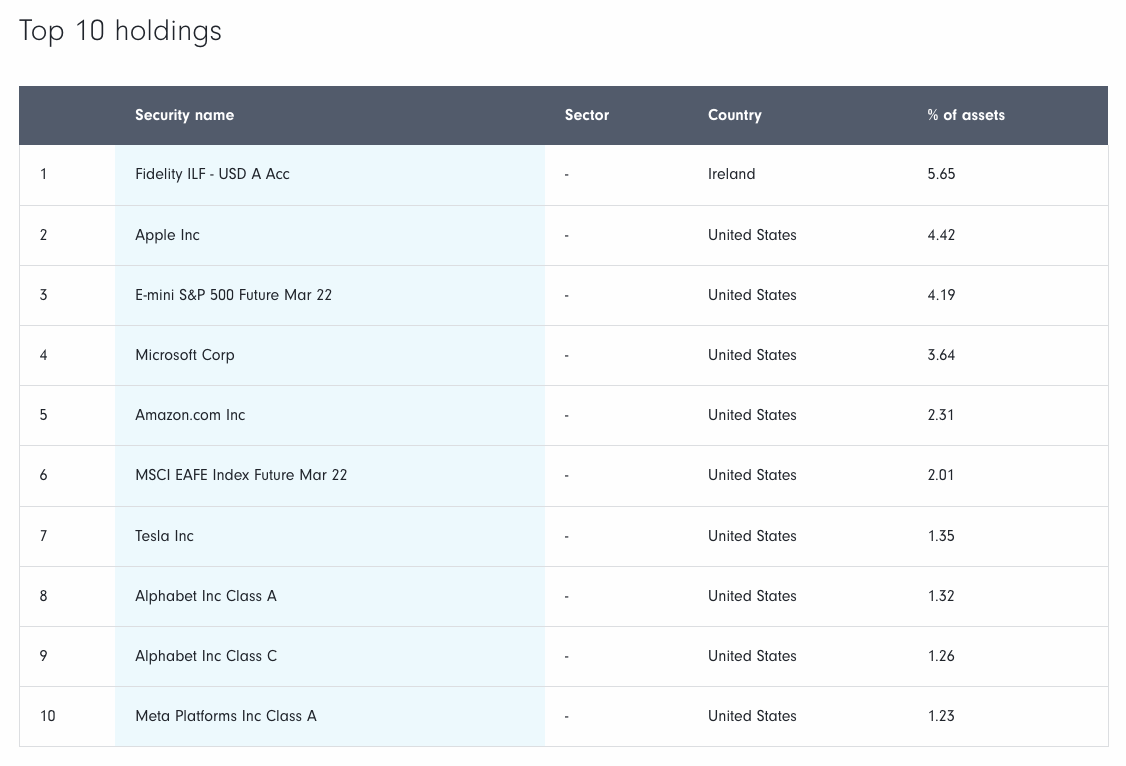

When looking at the Fidelity fund on the Fidelity website, the top holding listed (with a relatively large slice of 5.65% of assets allocated) is another fund, the Fidelity Institutional Liquidity fund (Fidelity ILF – USD A):

Confusingly though when i look at the same fund on Trustnet it doesn't feature in the list of holdings:

So does it feature in the fund or not?

Does anyone know what this fund actually is and why it has such a large allocation?

And what might it tell me about potential future performance?

Thanks

0 -

If you look in the small print of Fidelity Index World fund it says

" it aims to replicate the composition of the index. However, for practical reasons and/or to reduce the dealing costs of the Fund, it may not invest in every company share in the index"

The Vanguard fund says

"The Fund attempts to track the performance of the Index by investing in a representative sample of Index constituent shares"

It is not practical for the fund manager to go out and buy or sell 7000 different shares around the world every day. The cost, and the administrative effort would make it impossible to offer the fund at a charge of 0.2%. So they place smart bets on certain assets in an effort to track the index as best they can. Every index fund comes with a tracking error. It's usually small, and sometimes it's in your favour.

What you are seeing in the Fidelity information is fund management in action. The Liquidity Fund is their way of holding cash. Incidentally, it returned 0.03% last year, so Fidelity isn't getting any more interest than you or I on it's instant access savings.

When they hold 5% cash, they are obviously not going to keep up if the Index goes up. So they have to place some bets. Look at Item 3 on the list: S&P 500 Futures. That is a bet that the S&P 500 goes up. If it does, it pays out - more than a similar investment in the 500 shares. If the S&P goes down, they lose more. That's the risk you pay the fund manager to balance for you. Either way, this allows them to track the performance of the S&P at a fraction of the cost of buying all 500 constituents.

Same thing applies to item 6. They are passing off the complexity of tracking the MSCI index to a 3rd party.

The Trustnet listing is showing you the proportions of various equities in the Index. The Fidelity listing is an accurate snapshot of how they are replicating that Index.0 -

So essentially they're saying the same thing, that both funds aim to track/replicate the performance/composition of the indices but won't necessarily invest in all the shares within the index to achieve this?Secret2ndAccount said:If you look in the small print of Fidelity Index World fund it says

" it aims to replicate the composition of the index. However, for practical reasons and/or to reduce the dealing costs of the Fund, it may not invest in every company share in the index"

The Vanguard fund says

"The Fund attempts to track the performance of the Index by investing in a representative sample of Index constituent shares"

Will the inclusion of this underlying Institutional Liquidity fund have any significant affect on its risk or performance when compared to the VG Global fund?

Or are the funds pretty much doing exactly the same thing?

I'm leaning towards the VG fund as it includes exposure to small-caps and emerging markets which the Fidelity fund doesn't. But i might look to switch funds when my pension pot get's bigger as the VG's ongoing charge is greater.

0 -

All index funds fail to track their index. There is always a tracking error. In my experience the error is small, and will sometimes work in your favour.

Different funds use different methods to simulate the Index. In theory, if there was a massive, unexpected move in the Index, one fund might track it much better than another, but we're getting way out into the weeds here. You are looking at two funds, and you already have no way of knowing which one will outperform the other. I would suggest that tracking error is not your prime concern.

Compare the past performance of the two indices, or investigate the constituents of the two indices. Decide which index you prefer. Choose a low cost index tracker that tracks your index.

If you can't decide, you could buy half and half. Or put all of your current money into one, then buy the other with your future contributions.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.9K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.5K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards