We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Defined Benefit Scheme

I am a 'preserved' member (I was in the scheme for just over 14 years) of the Brass railway pension scheme and within this scheme my normal retirement date was 02/05/21. As of today it states ''Your overall pot value: £15,967.93.'' Updated 19/01/22

I have just looked at the estimated value as of 14/12/21. And is attached below. What I want to know is, should I choose one of the options it gives me to take the money now, if so which option or should I leave it where it is? And could someone explain the options in simple 'Janet & John' terms please. I was thinking of choosing one of the options, and putting the lump sum in a easy access saving account and drip feeding the yearly pension into the same account until I can claim my state pension at 67, I am 61 this year.

Thank you for your help and thoughts

Comments

-

What did you do with the £15K lump sum you mentioned in November: https://forums.moneysavingexpert.com/discussion/6314416/lump-sum#latest

Might help people to answer helpfully if they know that.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

Hi Marcon,

Thanks for reply,

yes, sorry the £15k was my pension pot, I just didn't know how to explain it clearly.0 -

What exactly does your state pension forecast say?

Are you still earning and paying (or being credited) with NI?

BRASS is the AVC scheme for Railway Pensions.

https://www.btppensions.co.uk/in-the-fund/brass-avcs/taking-my-brass-benefits#:~:text=When you take your benefits,your regular pension payments start.

https://member.railwayspensions.co.uk/resources/news/2021/05/17/late-retirement

Did you opt for late retirement as a deferred member as described above?

If so, have you benefited from a late retirement enhancement?

https://member.railwayspensions.co.uk/in-the-scheme/planning-for-retirement/options-for-db-members/when-to-retire

Do you wish to take your Railway Pension now or (especially if you are still working) would you benefit from continuing to postpone taking it?

0 -

Thanks for reply xylophone. I will have a look later and update0

-

Thanks for reply xylophone. I will have a look later and update

In your PM you referred to an estimate showing Basic State Pension. (presumably from before NSP scheme started).

As you come under the new state pension scheme, what exactly does your state pension forecast say?

As I mentioned in PM, you should check with the administrator whether there is any enhancement to the pension if taking it is postponed beyond Normal Scheme Pension Age.

The Guide here

does clarify that the value of the BRASS (AVC) element does vary because it is related to that of the funds within the BRASS account.

What exactly is meant by the "level pension option"?

0 -

I wonder if 'level pension option' gives you more before state pension age and less afterwards. Do you reach state pension age in 2028?

But a banker, engaged at enormous expense,Had the whole of their cash in his care.

Lewis Carroll0 -

Hello again,

My gov state pension when I reach 67 (2028) is £179.60 p/w

The figure of £5604.32 is from an estimate dated 14/12/21 from my railway pension. See below, I have copied/pasted the actual estimate with personal details removed.

I currently work part time with an annual income of £15306.67 per year

Thank you in advance for your opinions and options I could take

0 -

The figure of £5604.32 is from an estimate dated 14/12/21 from my railway pension.I really don't understand how this figure for average basic state pension was calculated but I am assuming that it was the figure used when setting the "level pension option".

I tried Google again and found this

- Level pension

You may want to take your RPS benefits before you can claim your State Pension.

With the level pension option you take more RPS pension before your State Pension age and less RPS pension after your State Pension age.

This aims to smooth or level out your income throughout your retirement .........

Link above also references a planner which is available to you when you log in to your pension details - this helps you to model your options.

The choice for you depends on which suits your particular situation best.

Would you be better off in the longer term taking a lower lump sum and benefiting from inflation linking on a higher pension?

When exactly were you a member of RPS?

With regard to your state pension forecast, does it say that you need to continue to contribute to reach a full new state pension?

See this

Would you continue to work if you drew your railway pension?

I would check with the administrator as to whether there would be late retirement enhancement if you chose to postpone taking the pension.

Presumably you are a member of your current employer's pension scheme?

And do you have other pensions apart from current and Railway deferred ( and SP in due course)?

0 -

Hi,

To answer your original question, you need to identify what you want to achieve.

By default the railway pension scheme (RPS) gives you a lump sum and a pension. You can choose to convert the lump sum to / from pension at a commutation rate of 12:1, subject to a limit on the maximum amount of lump sum of 25% of the tax value of the pension (tax value = 20x pension + lump sum + BRASS). BRASS is an AVC scheme into which you could pay extra if you wanted, you may have been lucky enough for your employer to match your contributions at the time. The RPS rules require that BRASS is taken as a lump sum.

Before the revised state pension arrangements came in, the RPS pension was designed such that when you retired, the sum of your railway pension and your basic state pension amounted to 2/3rds of your pay, assuming that you worked on the railway for 40 years. That is why the RPS retains the concept of a basic state pension in its statements although you don't need to worry about that now (except perhaps with respect to the level pension option - see below).

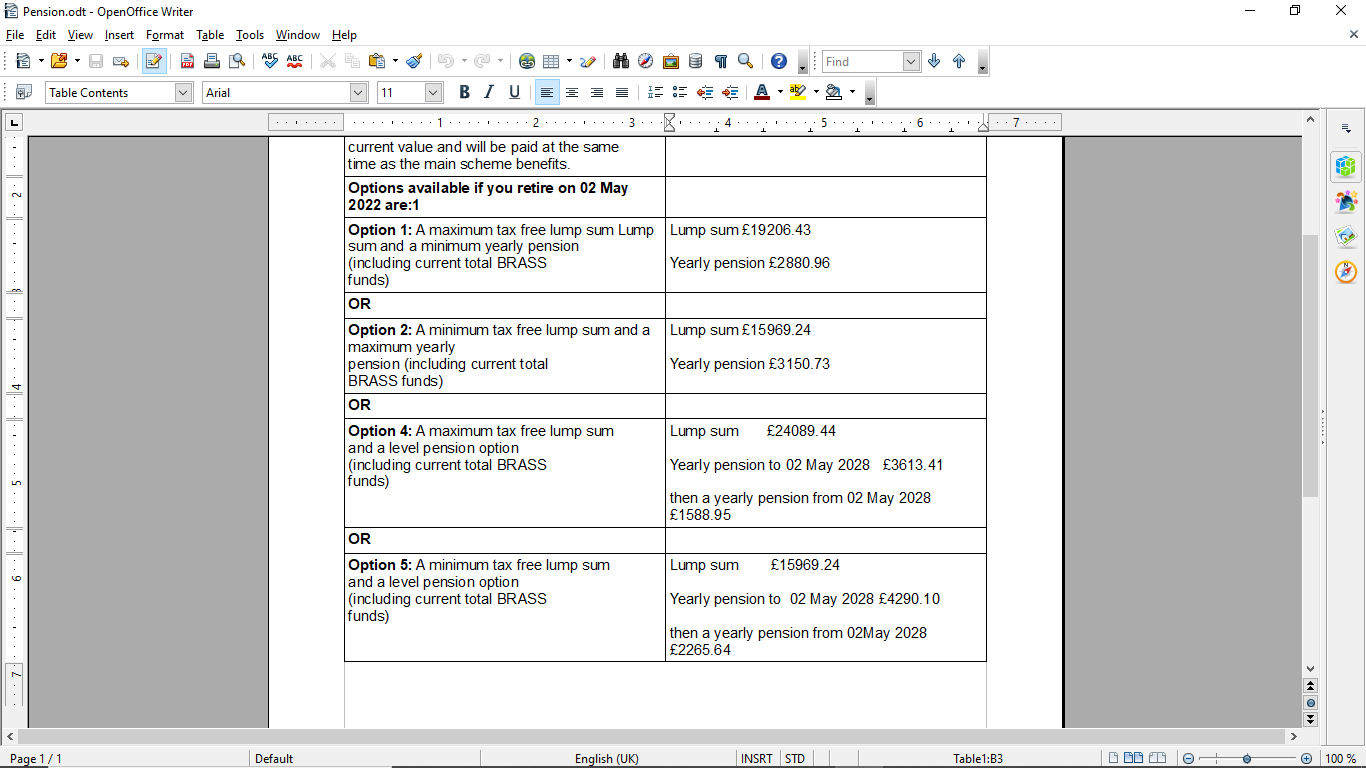

Options 1 and 2 are based on you taking a fixed (but subject to inflation increases) pension and lump sum and illustrate the extremes between maximum pension / minimum lump sum and minimum pension / maximum lump sum, you could choose to go somewhere in the middle if you wanted.

The RPS has the concept of a level pension, intended to cater for the fact that the RPS retirement age was 60 and the (male) retirement age was 65. The idea of this was that you received an increased pension (by the amount of the basic state pension) from 60-65 and a reduced pension from 65 onwards so that you had a level income (when adding together your railway pension and basic state pension) from 60 until death (i.e. that the start of state pension at 65 was matched by a corresponding reduction in the railway pension). The new state pension arrangements will have interacted with this in ways I don't understand, if you wanted me to guess then I would assume that the level pension option would be based on your later retirement age but on the RPS stated basic state pension, not the new (larger) state pension. Guessing is a poor way to plan for retirement though so if you are interested in this option then you need to get more details from the RPS.

Options 3 and 4 are the level pension option but with the same options as 1 and 2 - i.e. maximum / minimum pension / lump sum.

So, with respect to what is the best thing for you to do, what is it you want to achieve?

What is behind your idea of taking the pension and putting it into a savings account? Is this something for yourself or something you want to pass on to children? Without knowing more about your circumstances then it is very difficult to comment on whether this is a good idea.

You are 61 and could have taken the railway pension at 60 so it appears that you have decided that you don't need the pension right now - is that correct?

Are you sure that your pension will be increased to reflect the greater age at which you start taking the pension - historically the RPS didn't offer any benefit for taking it late but I think this might have changed? Have you checked this with the RPS?

Taking the BRASS separately (apart from it being difficult, you would need to transfer it out) doesn't make sense - if you don't need the pension then you don't need the BRASS either - or do you have an urgent need for the money?

If you are looking to maximise your overall money from the RPS when you do take it then taking the maximum pension and smallest lump sum (i.e. options 2 or 5) is probably financially the best move - you only need to live 12 years for it to be worthwhile - having said that, the later you leave taking your pension, the greater the chance that you won't make those 12 years (although you stand a good chance of doing so if you take the pension on/before state retirement age).

Finally, does the level pension look like something that might interest you? If so then you need to find out the exact details from RPS.1 -

Hello again,

Thank you very much xylophone and doodling, I will make a couple of phone calls and update you.

Again Thank you1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.9K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards