We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Mortgage Refused

davybull

Posts: 60 Forumite

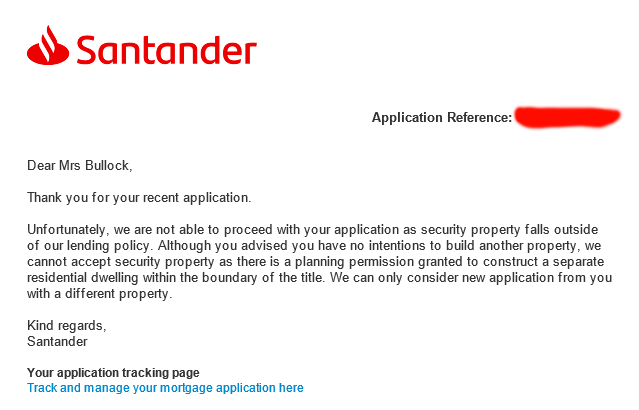

Just had a Mortgage from Santander refused because there is outline planning permission to build a bungalow at the back of the plot.

We were putting an £85,000 deposit down.

We have no intention of doing the build and have offered to sign a document ensuring this but to no avail.

So now need to look for a different company.

Similar situation to a previous post in 2015. I can only see Santander doing this.

https://forums.moneysavingexpert.com/discussion/5251859/mortgage-refused-because-outline-planning-permission-is-on-the-land

We were putting an £85,000 deposit down.

We have no intention of doing the build and have offered to sign a document ensuring this but to no avail.

So now need to look for a different company.

Similar situation to a previous post in 2015. I can only see Santander doing this.

https://forums.moneysavingexpert.com/discussion/5251859/mortgage-refused-because-outline-planning-permission-is-on-the-land

0

Comments

-

Fairly standard policy from Santander. Never made an exception on it as far as i am aware. They refuse to split title if there is a mortgage on it so take a blanket rejection when there is a risk of that happening.

3 -

Try a different lender or a different property.0

-

How much has the outline planning permission inflated the price of the property?0

-

It's their policy and many lenders do not use legal and general. Connells is one of the larger ones.Chetlaw said:@davybull did you find another lender ? We are having a similar situation . Santander have said its the surveyor policy not theirs. They said legal and general are the surveyors for most banks valuations, so we would find this issue if we switch providers..

Do you have a broker? Ask them to find you a suitable lender.0 -

Care: 2022 thread revival@davybull did you find another lender ? We are having a similar situation . Santander have said its the surveyor policy not theirs. They said legal and general are the surveyors for most banks valuations, so we would find this issue if we switch providers..In some areas, L&G are the only valuers for all the lenders. In others they are not.

In the OP's case, they were not proceeding with the build in the planning permission. So, all they had to do is cancel the planning application. If you are in the similar situation is the OP, as you say you are, then cancel the planning application.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

dunstonh said:In the OP's case, they were not proceeding with the build in the planning permission. So, all they had to do is cancel the planning application. If you are in the similar situation is the OP, as you say you are, then cancel the planning application.You can't do that on property that you do not yet own though...Would be interesting to know if an undertaking to cancel it would have been acceptable?1

-

Good point. I was working on the basis that it was a remortgage rather than a purchase.MWT said:dunstonh said:In the OP's case, they were not proceeding with the build in the planning permission. So, all they had to do is cancel the planning application. If you are in the similar situation is the OP, as you say you are, then cancel the planning application.You can't do that on property that you do not yet own though...Would be interesting to know if an undertaking to cancel it would have been acceptable?I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

I don't think you can 'cancel' planning permission anyway? Once it's been decided on by the LA (approved/refused), that's it - it stays valid for the time that the LA states (usually 3 years), and then it expires if the work hasn't commenced.

Only other possibility might be to ask the vendor/conveyancers to separate the land where the PP is onto a separate title (you still want to make sure you're buying both, obviously). Then the mortgaged property won't have PP on it. But bear in mind that the property will be valued sans the separate land. That's also what would happen if the second dwelling were ever built anyway.

In reality, finding a less fussy lender might be easier.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.7K Work, Benefits & Business

- 603.1K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards