We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Crunch time, do we complete on house in Spain?

Bossy_bird

Posts: 19 Forumite

Afternoon everyone, Newby post but at a real decision crunch point and could do with your advice….

Me and hubby both 43 and trying to avoid slipping into our respective mid life crises by actively engaging in pension planning. Ideally we would like to be flexible with employment choices at 55 and retired at 60. We have been lucky in our careers and could absolutely do more over the next few years to secure our future. We have been frivolous previously but both now love a spreadsheet!!

A little bit about us…

Combined DC pots are currently at £476k and I have a mini DB pension giving £4400 pa at 63. £75k in ISAs. Both have 3 yrs working left to full SP allowance. We have a mahoosive mortgage of £560k but with c. 50% equity. 19 yrs left. We also have a small place in Spain with no mortgage.

Me and hubby both 43 and trying to avoid slipping into our respective mid life crises by actively engaging in pension planning. Ideally we would like to be flexible with employment choices at 55 and retired at 60. We have been lucky in our careers and could absolutely do more over the next few years to secure our future. We have been frivolous previously but both now love a spreadsheet!!

A little bit about us…

Combined DC pots are currently at £476k and I have a mini DB pension giving £4400 pa at 63. £75k in ISAs. Both have 3 yrs working left to full SP allowance. We have a mahoosive mortgage of £560k but with c. 50% equity. 19 yrs left. We also have a small place in Spain with no mortgage.

We have found a bigger place in Spain that would be perfect for us to retire to or at least spend the 180 days permitted! However it would involve equity release from current home increasing LTV to 70% at a time when the world seems to be going slightly mental. Our target would be to pay off additional borrowing in 5yrs and then know that our retirement home is ours and then it’s just all about ‘the number’. However I’ve started to become anxious about job security and the pressure to maintain our current high salaries. We probably earn enough to retire early (50 ish) if we were sensible….but we are not 😬. The completion date is in 3 weeks and mortgage offer is currently on our kitchen table…extra borrowing at just over 1% fixed for 5 yrs feels like a great deal. I’m rambling, I guess I have two questions; Do we buy in Spain or is it too risky? and are we doing ok from a pensions perspective? I think we could do more….your advice is needed!!

0

Comments

-

There is nothing 'mini' about a DB pension which will pay £4,400 at age 63 - but are you sure that isn't the current value (i.e. is that an estimate which takes into account the pension will increase between now and when you draw it)?Bossy_bird said:Afternoon everyone, Newby post but at a real decision crunch point and could do with your advice….

Me and hubby both 43 and trying to avoid slipping into our respective mid life crises by actively engaging in pension planning. Ideally we would like to be flexible with employment choices at 55 and retired at 60. We have been lucky in our careers and could absolutely do more over the next few years to secure our future. We have been frivolous previously but both now love a spreadsheet!!

A little bit about us…

Combined DC pots are currently at £476k and I have a mini DB pension giving £4400 pa at 63. £75k in ISAs. Both have 3 yrs working left to full SP allowance. We have a mahoosive mortgage of £560k but with c. 50% equity. 19 yrs left. We also have a small place in Spain with no mortgage.We have found a bigger place in Spain that would be perfect for us to retire to or at least spend the 180 days permitted! However it would involve equity release from current home increasing LTV to 70% at a time when the world seems to be going slightly mental. Our target would be to pay off additional borrowing in 5yrs and then know that our retirement home is ours and then it’s just all about ‘the number’. However I’ve started to become anxious about job security and the pressure to maintain our current high salaries. We probably earn enough to retire early (50 ish) if we were sensible….but we are not 😬. The completion date is in 3 weeks and mortgage offer is currently on our kitchen table…extra borrowing at just over 1% fixed for 5 yrs feels like a great deal. I’m rambling, I guess I have two questions; Do we buy in Spain or is it too risky? and are we doing ok from a pensions perspective? I think we could do more….your advice is needed!!

If you are only 43, buying a place in Spain to retire to seems a bit premature, especially as you are concerned about job security and recognise you aren't sensible with money. Just because the mortgage rate is good doesn't make the enterprise a good idea!Bossy_bird said:However I’ve started to become anxious about job security and the pressure to maintain our current high salaries. We probably earn enough to retire early (50 ish) if we were sensible….but we are not 😬. The completion date is in 3 weeks and mortgage offer is currently on our kitchen table…extra borrowing at just over 1% fixed for 5 yrs feels like a great deal. I’m rambling, I guess I have two questions; Do we buy in Spain or is it too risky? and are we doing ok from a pensions perspective? I think we could do more….your advice is needed!!

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!5 -

Thank you for such a quick response. Good point about DB I will double check whether it is a forecast or current value. We already have what we thought would be our Spanish bolt hole but after a few holidays there recently with our two boys we’ve realised it’s tiny and we would need more space. I like the idea of forcing ourselves to pay something off now while we can afford it otherwise we will let income fritter away. We set ourselves two years to pay off our last Spanish house and did it. We are great at working towards targets! I am trying to think long term and not get a negative and cautious mindset as a result of Covid/Brexit0

-

Ps. I love the ‘only 43’ comment !!! Made my day ☺️0

-

"Me and hubby both 43"

"Both have 3 yrs working left to full SP allowance "

I thought you needed 35 years, did you start work at 11?

0 -

Those rules don't apply to the op as they will be under transitional rules (like the vast majority of people at the moment).timjim said:"Me and hubby both 43"

"Both have 3 yrs working left to full SP allowance "

I thought you needed 35 years, did you start work at 11?

If the op hasn't already done so they should check their forecast, and more importantly, the amount accrued to date to be sure of the current position.0 -

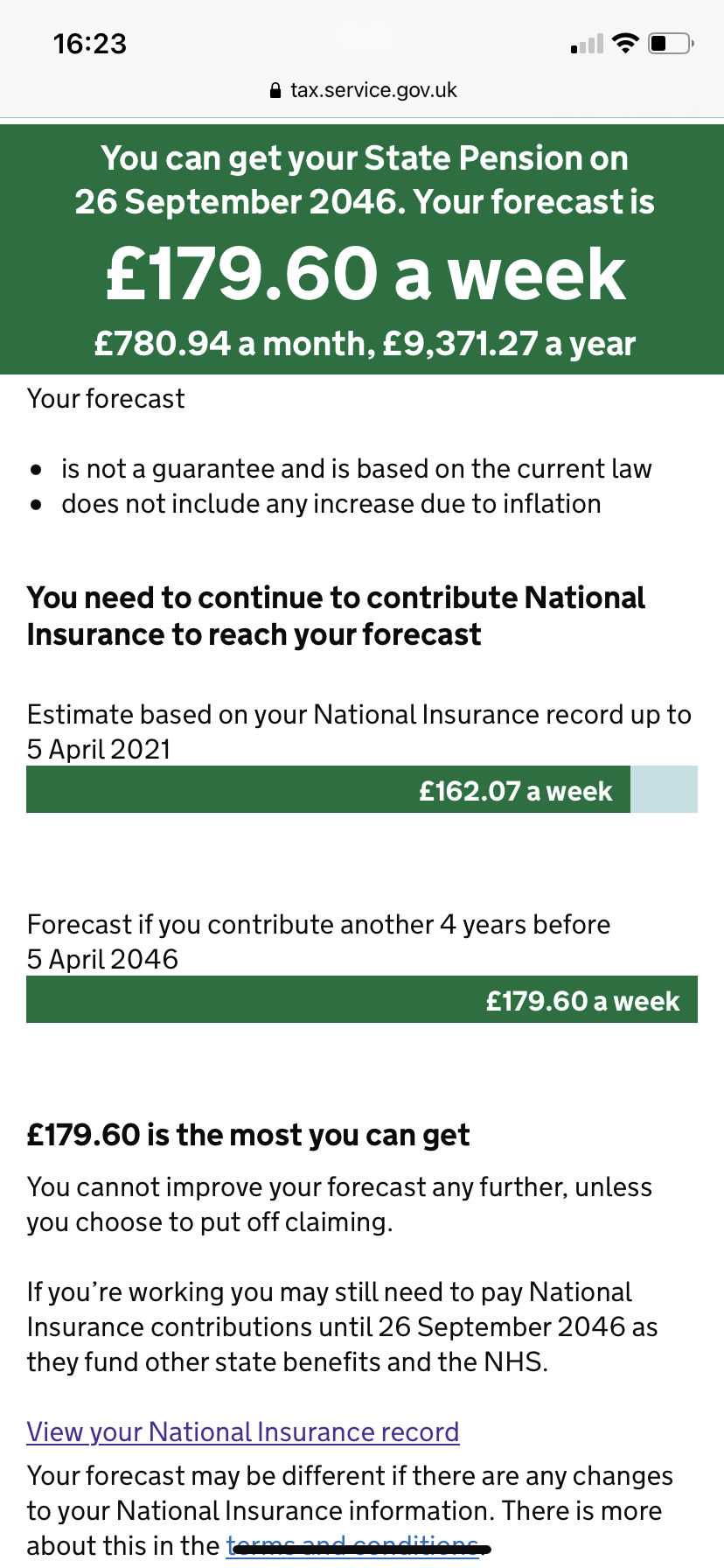

Sorry it’s 4 years or 3 years from April 22…well according to my online forecast 🤷🏻♀️

0 -

Another three years will take you to £177.46 with the fourth adding the final £2.14.1

-

feels like I started at 11 😂timjim said:"Me and hubby both 43"

"Both have 3 yrs working left to full SP allowance "

I thought you needed 35 years, did you start work at 11?

2 -

Under the system before 6 April 2016 you accrued one year of basic state pension for each full year and in addition got an earnings-related top-up. Since then it's been just one year with no earnings-related part. People had their amount calculated using both old and new rules for April 2016 and kept the higher amount. It's normal for those with a full working history who weren't contracted out of the earnings-related part to need less than 35 years because of the earnings-related but. Earnings-related top-up doesn't add more above roughly the higher rate income tax level of earnings. So no surprise if people with full work histories, particularly on above average wage, need far fewer than 35 years.timjim said:"Me and hubby both 43"

"Both have 3 yrs working left to full SP allowance "

I thought you needed 35 years...

The 2016 changes took future accrual away from those with full work histories to give extra money to those with limited work and mostly credits instead. As a result even low earners with a full working history will be getting about a quarter less under the new system than the old one, with the effect greater at higher earning levels.

At the moment if anyone who started earning or getting credits before 2016 needs 35 total it's just chance of their individual calculation.2 -

I suggest that you greatly increase your mortgage term with the goal of doing most repaying with the tax free lump sum from your pensions. This is because it gets you tax relief in effect on your capital repayments and because investment growth rates are currently expected to be well above mortgage interest rates, so you're expected to make more money than the extra interest cost. Note that around 250k per person is the maximum possible tax free lump sum because no tax free is possible on money above the pension lifetime allowance and that's currently a bit over a million Pounds with no inflation increases expected for a while.

If you do that you get the nice double benefit of lots of pension money for early retirement and significantly more efficient mortgage repaying. The benefit is even greater for higher rate tax payments and salary sacrifice.

If you're going to use the Spanish property a lot and perhaps let it for the time you don't use it then it could turn out to be a good buy.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards