We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Decisions decisions which fund should I choose?

Comments

-

Best me to it, this is the fund I use. Slightly more expensive than VLS but fairly well diversified (IMO). I've used VLS 80 and 100 previously, would use them again.cloud_dog said:

Why the ETF? Why not Vanguard FTSE Global All Cap OEIC?RoadToRiches said:I am undecided which one to go for, what are your thoughts?

Vanguard Life Strategy 100% Equity or Vanguard FTSE All World ETF

I am leaning towards the ETF only because of the UK bias on the VLS funds.

Or anything else like Scottish Mortgage Fund - but think that is over bought right now.

0 -

Thanks but I wanted something that covered the other regions too.Thrugelmir said:

An S&P 500 ETF tracker. Might as well go for it.RoadToRiches said:I am undecided which one to go for, what are your thoughts?

Vanguard Life Strategy 100% Equity or Vanguard FTSE All World ETF

I am leaning towards the ETF only because of the UK bias on the VLS funds.

Or anything else like Scottish Mortgage Fund - but think that is over bought right now.

0 -

Without referring to specific products, ETFs tend to have lower charges. There are other advantages, eg negation of stamp duty. As long as an individual is comfortablecloud_dog said:

Why the ETF? Why not Vanguard FTSE Global All Cap OEIC?RoadToRiches said:I am undecided which one to go for, what are your thoughts?

Vanguard Life Strategy 100% Equity or Vanguard FTSE All World ETF

I am leaning towards the ETF only because of the UK bias on the VLS funds.

Or anything else like Scottish Mortgage Fund - but think that is over bought right now.

0 -

The main difference between VLS 100 and FTSE all world is home bias. Vanguard has white papers addressing this issue. Worth a read before deciding. Excessive home bias (over 30% in UK) reduces diversification and can be detrimental. Some home bias reduces volatility without damaging long term performance.RoadToRiches said:I am undecided which one to go for, what are your thoughts?

Vanguard Life Strategy 100% Equity or Vanguard FTSE All World ETF

I am leaning towards the ETF only because of the UK bias on the VLS funds.

Or anything else like Scottish Mortgage Fund - but think that is over bought right now

1 -

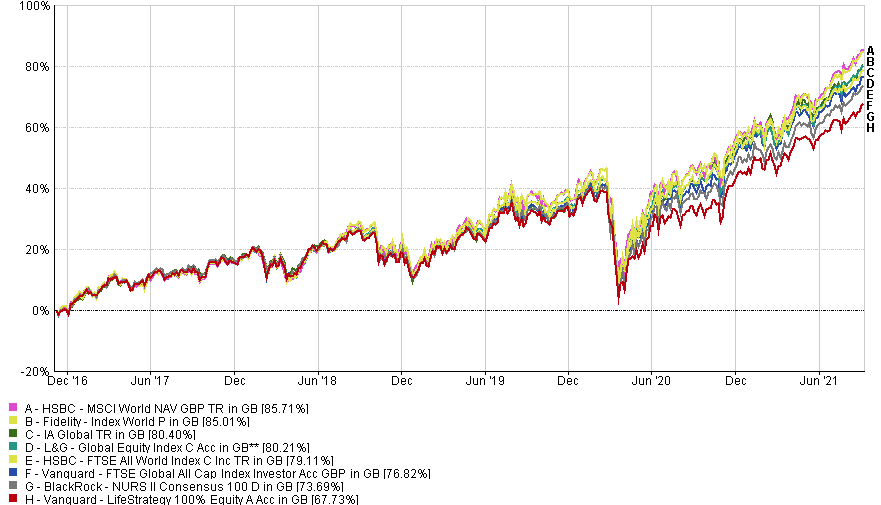

Firstly is it easy to see that it does behave like a global tracker.It's easy when you pick a global tracker and say it behaves like a global tracker. An apple tastes like an apple. A strawberry like a strawberry. Nothing to contest at all there.

However, VLS100 does not appear on your chart and it's not a tracker and the comments were about VLS100

So, here is a chart that does include VLS100, the sector average and the Vanguard global tracker.

Trackers tend to have mid-table consistency on a discrete basis but move up over time when looking at cumulative performance. VLS100 is not a tracker and behaves more like a typical mid-table managed fund that has a few years of outperformance and a few years underperforming but is generally around the sector average or below.

Why would you pick VLS100 over a global tracker?

And if you are going to pick a managed instead of a tracker, what makes you pick VLS100 over the other managed funds that exist?

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2 -

The “managed” reference is a red herring. Its not an actively managed fund. Its a set of globally diversified passive funds. One would pick VLS100 over a cap weighted global fund if he wants the same expected return but less volatility due to a small amount of hone bias. Conversely, one would pick a cap weighted global tracker if he does not care about a little extra volatility.1

-

That should work on paper but unfortunately the FTSE 100 is so international that currency movements cause it to be pretty volatile - more volatile than the world index. Then it is made up with a heavy proportion of more volatile sectors which also doesn't seem to help the overall plan of a home bias.Deleted_User said:The “managed” reference is a red herring. Its not an actively managed fund. Its a set of globally diversified passive funds. One would pick VLS100 over a cap weighted global fund if he wants the same expected return but less volatility due to a small amount of hone bias. Conversely, one would pick a cap weighted global tracker if he does not care about a little extra volatility.

I would like it to work, but it doesn't seem to.

Edit: that will teach me to check before writing but it does seem to make a reasonable difference to the volatility with the home bias.0 -

Something else to be aware of: the FTSE world tracker has fewer companies and 3.4% in APPL. VLS has 1.7% in APPL. Less vulnerable to major issues with the big tech in the US. And less exposed to their growth. Thats part of the reason for lower volatility the other being higher allocation to stocks priced in GBP.1

-

Corrected my schoolboy error with the wrong chart earlier, thanks @eskbankerI have never asserted nor suggested I would pick VLS100 over a global equity tracker. However reasons for that may include an investor seeking home bias and the diversification/volatility benefit therein (at least historically), global equity exposure while limiting currency risk etc.@dunstonh your first chart proves my point. As for the second, we all know VLS100 has underperformed more vanilla global trackers recently because of the home bias.To suggest VLS100 is a managed fund could mislead those who are seeking active global equity exposure. Fundamentally the idea behind it was A. a global equity tracker that B. upweights the UK and C. excludes small cap. Those are the two major differences between it and a pure/vanilla passive global total market approach. By that logic, no investment can be considered an index fund or passive because there will always be management decisions, imperfections in the holdings weights, trade timings, how far down the list of small cap stocks do you go to chase "completeness" etc. - and we're back to semantics.Pensioncraft has researched correlation between the FTSE 100 and sterling exchange rates and found none, he suggests it is a myth (

https://www.youtube.com/watch?v=TjbQuA5ibgA - I noticed this channel mentioned in posts by @albemarle and @MaxiRobriguez ).I can't find much in the way of historic global equity returns rebased to £, but to use the US as a proxy since it has dominated the world market since WWII, 1946-2020 inclusive S&P 500 total return annual standard deviation in USD = 16.8%, UK (FTSE 30 from 1946-1962, FTSE All-Share since) total return annualstandard deviation in GBP = 24.9%. However looking at the past 30 years, 1991-2020 inclusive, the S&P 500's was 17.0%, the UK's 15.1% (albeit with more muted returns at the end of that period). Not sure what this adds without including the exchange rate... Where would I find historic £-denominated returns data for a global equity index?1

https://www.youtube.com/watch?v=TjbQuA5ibgA - I noticed this channel mentioned in posts by @albemarle and @MaxiRobriguez ).I can't find much in the way of historic global equity returns rebased to £, but to use the US as a proxy since it has dominated the world market since WWII, 1946-2020 inclusive S&P 500 total return annual standard deviation in USD = 16.8%, UK (FTSE 30 from 1946-1962, FTSE All-Share since) total return annualstandard deviation in GBP = 24.9%. However looking at the past 30 years, 1991-2020 inclusive, the S&P 500's was 17.0%, the UK's 15.1% (albeit with more muted returns at the end of that period). Not sure what this adds without including the exchange rate... Where would I find historic £-denominated returns data for a global equity index?1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards