We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Know nothing about pensions - advice appreciated

Comments

-

Anyone who deals with pension investments deals with a lot of money, whether its in the early or late phases.No they don't. The average pension pot in the UK is around £19,000.You need a lot to retire and you won’t get there if you follow bad investment advice on day one.However, research has found that pensions from people that used advisers are higher than those that do not. Now that will be the result of many things but one key thing found was that too many people without an adviser put a too-small contribution to their retirement and tick the box as job done. Advisers do manage to get most to pay in greater figures.Advice on investment strategies from someone who does not really understand investment returns or stats behind various projections and strategies is worthless.The qualifications cover investment strategies and methodology. However, for the vast majority of consumers, it plays no part in their personal financial planning.Far better to read a short book by someone who is educated and does understand fundamentals and then follow recommendations.Recommendations that would not be based on the individual, their situation and needs and almost certainly beyond their capability of understanding or willingness to understand. A complete waste of time for the majority. A bit of a side reading for those that are interested in knowing more.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.3 -

However, research has found that pensions from people that used advisers are higher than those that do not.

Research has found that people who use the advice of Rolls Royce auto sales experts have higher pensions than those who do not. Its a ridiculous argument. Financial advisors target people with lots of money. For a good reason.

1 -

Diplodicus said:

I agree with Mordko. The proximity of "Be wary of people on the internet trying to put bad ideas into your head" following Mordko's reasonable suggestion kind of sums up the reaction awaiting any post that doesn't conform to the board's pro IFA narrative.Deleted_User said:

That’s completely false. I never said that. Your memory is failing you. It was a discussion in the context of investing. Of course some people had their retirement savings affected. Those who sold at the bottom would have suffered quite badly.Canuck01 said:Dunstonh - don't expect Mordko to say 'sorry I was wrong', I had a long boring discussion where I was told that the 2008 crash was a minor blip, no one's retirement savings affected at all, strangely including the ten million people in the US who lost their homes. Good luck talking some sense into him.I will have said it was a minor blip in terms of long term market performance over an average persons retirement saving period. Felt bad at the time but the markets recovered quickly and then some. A balanced portfolio recovered within a year. Nothing compared to crashes in the 70s or 30s.Many people in the US who lost their homes often walked out of their mortgages because they were under water and it was way too easy to do. They basically got rid of debt and improved their overall financial position. And happily own houses today.Others should never have been given mortgages in the first place. They didn’t really have these houses to lose.It was stressful for many people, but keep in mind that “about 10 million people” is a fraction of 1 percent of US population.It's not really that the board has a "pro IFA narrative", the majority of posters appear to be "DIY"* investors, which is why they're here. It's just that when vested interests are challenged in any context they tend to provoke a strong defensive reaction from those who stand to gain financially by convincing people of their side of the argument.Whereas there's no financial incentive for "DIY" investors to get involved in yet another tedious debate about the need for IFAs, and end up in the usual aggressive flame war so they don't bother, usually.*"DIY" in this context simply meaning those who don't use an adviser, a commonly used but misleading term, as investing eg in a multi-asset fund like VLS as many people do is hardly "DIY". That's a bit like buying a ready meal and heating it in a microwave and calling that "cooking".2 -

Avoiding the IFA debate that has infected the thread , I will try and answer the above !ClaireLR said:Thank you all for your help and advice.

I had a call this morning with the IFA. He has explained to me about annuities and draw down (spoke to him before I'd managed to get back onto this thread). He's explained about nominating each other and our children for the pension to go to, and about the tax we would pay when drawing out lump sums and/or taking an amount per month. I spoke to him about the SW pension I have and he is going to write to them to see if I would lose any benefits by transferring that money to a different pension provider. I haven't asked yet about charges as he is going to come back to me re the SW pension first and then take it from there.

One thing I'm wondering is, is it just a case of finding the pension with the best rate? How do they find a "good" pension?

Firstly a pension is just an administrative entity that deals with contributions, withdrawals, taxation etc .

What is more important is the investments within the pension .

If you have Investment X in Pension A and Investment X in Pension B it will perform exactly the same .

So in simple terms you judge a pension provider on how easy the website is to use/customer service , the range of investments on offer and the charges .

Judging/picking what investments to have within the pension is a bit more of a challenge for new investors, but not rocket science.

Your IFA will probably suggest a pension provider they prefer to use, and then an investment portfolio that will suit you .

If you agree an ongoing annual % charge they will sort it all out for you .

If you just pay a one off charge they will tell you what to do and then you have to go and do it yourself.

1 -

The old fashioned way that may return sometime when interest rates are higher was for you to take 25% of the value of the pension pot as a tax free lump sum and the adviser would then use research to find the highest income for your money, perhaps contacting them directly to see if they would increase their offer. In this case the 75% was then all spent at once to buy an annuity that provided an ongoing taxable income.ClaireLR said:

One thing I'm wondering is, is it just a case of finding the pension with the best rate? How do they find a "good" pension?

The more usual way today is to use income drawdown, which means leaving the money invested and taking a sustainable amount of income from it, which doesn't have to be the same each year but can be arranged to pay more when you're younger, perhaps to bridge the years until state pension age by paying the equivalent of the state pension immediately and on top some regular income that will continue from now until, probably, death.

If you're anywhere close to state pension age, deferring claiming your state pension beats annuity buying to get extra guaranteed and inflation linked income hands down, if health is reasonably normal.

Sometimes some annuity buying is appropriate, say if there's an absolute minimum income need and the sate pension plus any deferring won't provide that, and the person doesn't want to accept that the investments alone can do the job of providing the extra.

In all cases and IFA is expected - and required by their regulator - to properly understand your financial assets and objectives so they can come up with a plan to address those.

It's vital that if asked about risk tolerance you don't simply say high or low or pick a number between one and ten. You are more likely to have a tolerance to certain levels of income change and a tolerance to certain levels of investment ups and downs (a 20% drop in a bad year before eventual recovery is typical for common retirement investment combinations but more or less can be arranged) so that a proper mixture of approaches can be used. Say that you want to be paid the equivalent of the state pension on top until you reach state pension age if needed. You should also say if and how important inheritance is for you and whether you want it to be only money left over from investments when you die or if you want to set some aside solely for that purpose. It's fairly easy to be channeled into an appropriate choice if you aren't asked and explicit about things like income variation and inheritance objectives.

As people get older they can become less willing to deal with investments and also as they get older, the income paid for a certain amount of spend on an annuity goes up. Eventually, perhaps in the late 70s, an annuity can become a better buy than staying invested, at least for money that isn't destined for an inheritance (normal annuities leave nothing for that, but there are types which do). It also completely removes any investment uncertainty in your income and ensures that the income will last however long you live, even if you set a new record. Say if this seems interesting to you.

The better the job you do of explaining what variation of income and what ups and downs of investments you can handle, the better job the adviser can do in coming up with a plan that truly meets your needs.

The adviser is checking for the benefits of the current plan because their pricing may differ if there is a need to transfer out of a plan with protected benefits. It's also possible that they wouldn't want the business if that turns out to be so. Nothing to do on that but wait and see what they say.1 -

Thank you so much for taking the time to write that all out for me, some very useful information there. I will re read it tomorrow as I've got brain ache at the moment (kids still off school!) so I know it hasn't all sunk in!jamesd said:

The old fashioned way that may return sometime when interest rates are higher was for you to take 25% of the value of the pension pot as a tax free lump sum and the adviser would then use research to find the highest income for your money, perhaps contacting them directly to see if they would increase their offer. In this case the 75% was then all spent at once to buy an annuity that provided an ongoing taxable income.ClaireLR said:

One thing I'm wondering is, is it just a case of finding the pension with the best rate? How do they find a "good" pension?

The more usual way today is to use income drawdown, which means leaving the money invested and taking a sustainable amount of income from it, which doesn't have to be the same each year but can be arranged to pay more when you're younger, perhaps to bridge the years until state pension age by paying the equivalent of the state pension immediately and on top some regular income that will continue from now until, probably, death.

If you're anywhere close to state pension age, deferring claiming your state pension beats annuity buying to get extra guaranteed and inflation linked income hands down, if health is reasonably normal.

Sometimes some annuity buying is appropriate, say if there's an absolute minimum income need and the sate pension plus any deferring won't provide that, and the person doesn't want to accept that the investments alone can do the job of providing the extra.

In all cases and IFA is expected - and required by their regulator - to properly understand your financial assets and objectives so they can come up with a plan to address those.

It's vital that if asked about risk tolerance you don't simply say high or low or pick a number between one and ten. You are more likely to have a tolerance to certain levels of income change and a tolerance to certain levels of investment ups and downs (a 20% drop in a bad year before eventual recovery is typical for common retirement investment combinations but more or less can be arranged) so that a proper mixture of approaches can be used. Say that you want to be paid the equivalent of the state pension on top until you reach state pension age if needed. You should also say if and how important inheritance is for you and whether you want it to be only money left over from investments when you die or if you want to set some aside solely for that purpose. It's fairly easy to be channeled into an appropriate choice if you aren't asked and explicit about things like income variation and inheritance objectives.

As people get older they can become less willing to deal with investments and also as they get older, the income paid for a certain amount of spend on an annuity goes up. Eventually, perhaps in the late 70s, an annuity can become a better buy than staying invested, at least for money that isn't destined for an inheritance (normal annuities leave nothing for that, but there are types which do). It also completely removes any investment uncertainty in your income and ensures that the income will last however long you live, even if you set a new record. Say if this seems interesting to you.

The better the job you do of explaining what variation of income and what ups and downs of investments you can handle, the better job the adviser can do in coming up with a plan that truly meets your needs.

The adviser is checking for the benefits of the current plan because their pricing may differ if there is a need to transfer out of a plan with protected benefits. It's also possible that they wouldn't want the business if that turns out to be so. Nothing to do on that but wait and see what they say.Sometimes you have to go throughthe rain to get to therainbow0 -

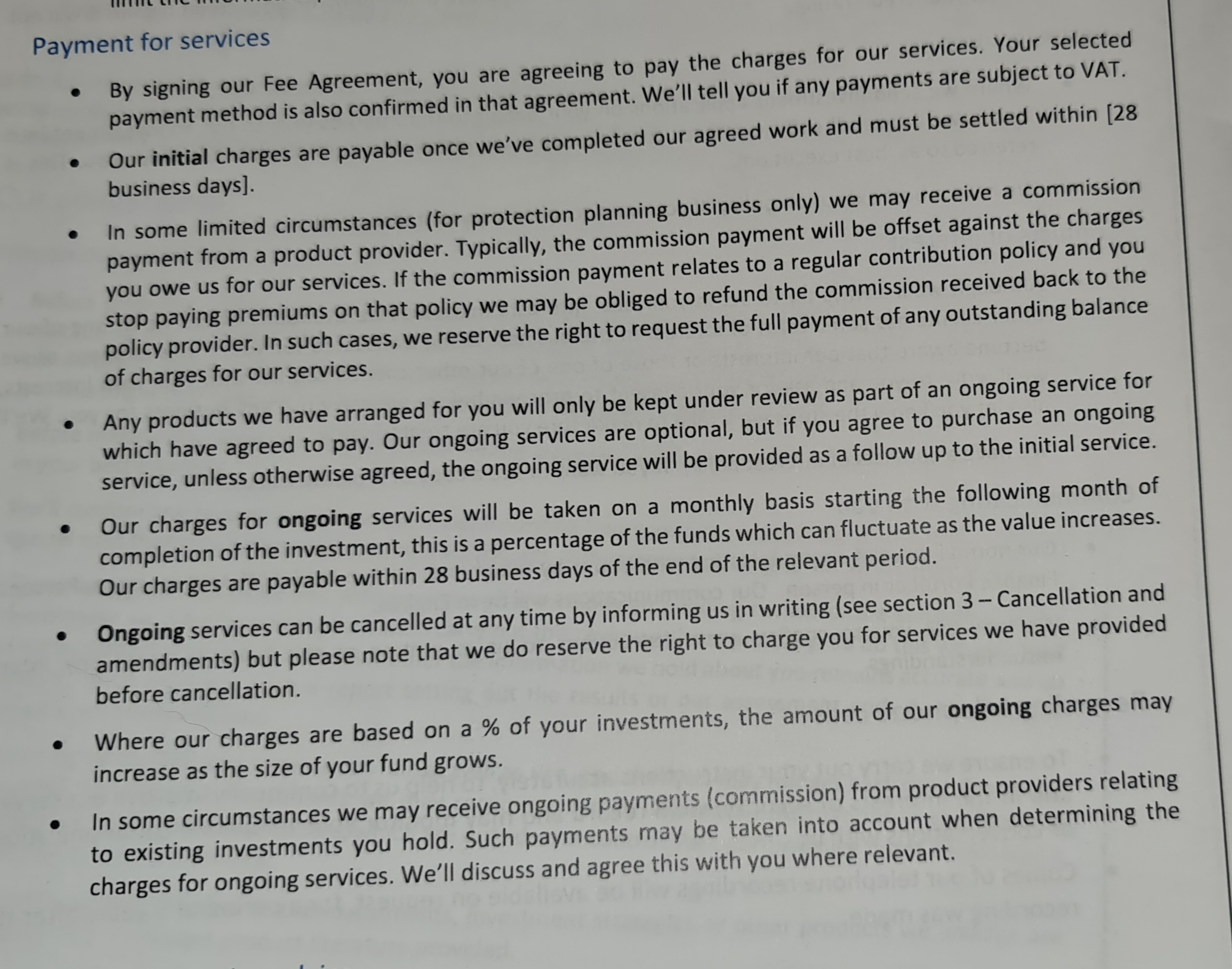

Does this throw up anything to be wary of? All I've signed so far is a letter of authority for them to approach Scottish Widows and a form consenting to them processing sensitive data. So no fees agreed as yet.

Sometimes you have to go throughthe rain to get to therainbow0 -

Does this throw up anything to be wary of?No LOAs are required to get the information from the existing provider. The image you linked to is not an LOA but a page from their terms of business. TOB is normally issued at the outset. Some firms get you to sign their terms of business. Whilst others give it to you unsigned and you only become committed to the fee once the personalised fee agreement is signed.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards