We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Snowball or Avalanche - Opinions please

Comments

-

Likely loans does allow overpayments though, and would appear to have a representative Apr of 60%. Is there not a strong case for tackling this one first?2

-

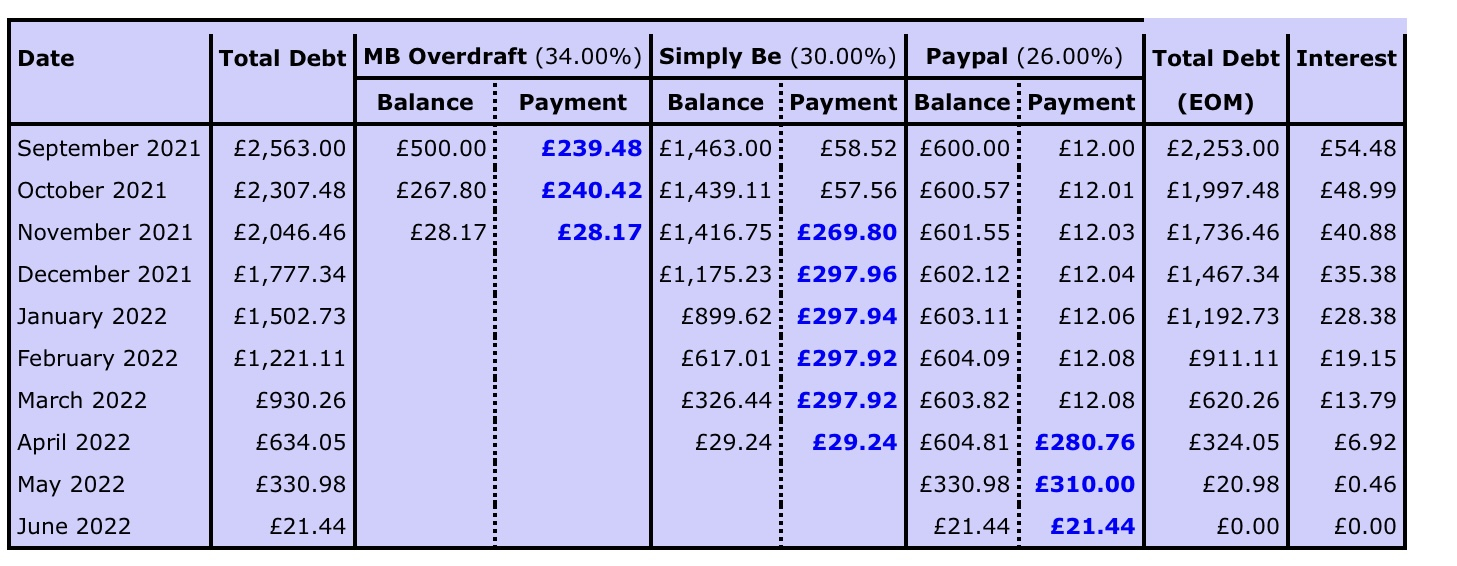

If you do a standing order for £15 a month to PP, it will bring the total down a little bit each month, and will also bring the date forwards to May next year, so you get another bit of motivationrigare11a said:Ok so after getting some new rates from SB and validating the min payment amount I have recalculated below also chucking an extra £10 pm at the payments. I will need to pay a bit more than minimum on PayPal else it will go over the arranged limit. But I think I am going for the avalanche

Thanks for all your inputs Credit card debt - NIL

Credit card debt - NIL

Home improvement secured loans 30,130/41,000 and 23,156/28,000 End 2027 and 2029

Mortgage 64,513/100,000 End Nov 2035

2022 all rolling into new mortgage + extra to finish house. 125,000 End 20362 -

TheAble said:Likely loans does allow overpayments though, and would appear to have a representative Apr of 60%. Is there not a strong case for tackling this one first?

I would have though that even when a loan has all the interest "pre loaded" onto your fixed monthly payments, any over-payment would bring down the total payable over the term of the loan. So yes, I think this option would need investigating further, especially if it has a higher APR than the others.

I can see where the confusion would lie though, as you don't have an ongoing "balance" as such, like you do with a CC, overdraft or Credit account.

How's it going, AKA, Nutwatch? - 12 month spends to date = 3.24% of current retirement "pot" (as at end December 2025)0 -

Thanks Susie I will do that for sure!SusieT said:

If you do a standing order for £15 a month to PP, it will bring the total down a little bit each month, and will also bring the date forwards to May next year, so you get another bit of motivationrigare11a said:Ok so after getting some new rates from SB and validating the min payment amount I have recalculated below also chucking an extra £10 pm at the payments. I will need to pay a bit more than minimum on PayPal else it will go over the arranged limit. But I think I am going for the avalanche

Thanks for all your inputs

Very (Shopping) £796.16 Paid in FULL as of 17/08/2021

Simply Be £1463 £1432 £1195.13 £801.02 £645.24 Paid in FULL 30/09/2021Likely Loans £2465.73 £2191.76 £1917.79 Paid in FULL May 2022

Overdraft £500 Paid in FULL Jan 2023

PayPal Credit £566.53 Paid in FULL Jan 2023

Total debt £5824.89 at the very start of DFW Journey.

Current debt £5,028.73 £4997.73 £4384.31 £3990.20 £3823.06 £2260.37 £1066.53 £0.00

Debt added since start of journey £9000 (borrowed from partner for car)

Current balance of £8550 £8150 Paid in Full June 2022

My debt free diary:

https://forums.moneysavingexpert.com/discussion/6291011/debit-free-diary-starting-august-2021-target-may-2022#latest1 -

Thanks Able and Shell, I will give them another call today and check. Last time I called the rep on the phone sounded a bit unsure and then stated that the balance is the balance whether I pay today or not. Maybe I will see if I can get someone a bit more savvy on the phoneSea_Shell said:TheAble said:Likely loans does allow overpayments though, and would appear to have a representative Apr of 60%. Is there not a strong case for tackling this one first?

I would have though that even when a loan has all the interest "pre loaded" onto your fixed monthly payments, any over-payment would bring down the total payable over the term of the loan. So yes, I think this option would need investigating further, especially if it has a higher APR than the others.

I can see where the confusion would lie though, as you don't have an ongoing "balance" as such, like you do with a CC, overdraft or Credit account.Very (Shopping) £796.16 Paid in FULL as of 17/08/2021

Simply Be £1463 £1432 £1195.13 £801.02 £645.24 Paid in FULL 30/09/2021Likely Loans £2465.73 £2191.76 £1917.79 Paid in FULL May 2022

Overdraft £500 Paid in FULL Jan 2023

PayPal Credit £566.53 Paid in FULL Jan 2023

Total debt £5824.89 at the very start of DFW Journey.

Current debt £5,028.73 £4997.73 £4384.31 £3990.20 £3823.06 £2260.37 £1066.53 £0.00

Debt added since start of journey £9000 (borrowed from partner for car)

Current balance of £8550 £8150 Paid in Full June 2022

My debt free diary:

https://forums.moneysavingexpert.com/discussion/6291011/debit-free-diary-starting-august-2021-target-may-2022#latest1 -

Good luck with your debt free journey, you seem really motivated and on the ball.

Personally, I would repay the overdraft first, save up an Emergency Fund and then snowball the debts It worked for me.

Can you transfer any of the debt to 0% cards even if it is just part of the amount?Just when I'm about to make ends meet, somebody moves the ends1 -

Thank you, I did think about 0% cards but I was recently declined finance application so don't think I would get approved for a card.thriftychick said:Good luck with your debt free journey, you seem really motivated and on the ball.

Personally, I would repay the overdraft first, save up an Emergency Fund and then snowball the debts It worked for me.

Can you transfer any of the debt to 0% cards even if it is just part of the amount?Very (Shopping) £796.16 Paid in FULL as of 17/08/2021

Simply Be £1463 £1432 £1195.13 £801.02 £645.24 Paid in FULL 30/09/2021Likely Loans £2465.73 £2191.76 £1917.79 Paid in FULL May 2022

Overdraft £500 Paid in FULL Jan 2023

PayPal Credit £566.53 Paid in FULL Jan 2023

Total debt £5824.89 at the very start of DFW Journey.

Current debt £5,028.73 £4997.73 £4384.31 £3990.20 £3823.06 £2260.37 £1066.53 £0.00

Debt added since start of journey £9000 (borrowed from partner for car)

Current balance of £8550 £8150 Paid in Full June 2022

My debt free diary:

https://forums.moneysavingexpert.com/discussion/6291011/debit-free-diary-starting-august-2021-target-may-2022#latest0 -

rigare11a said:

Thanks Able and Shell, I will give them another call today and check. Last time I called the rep on the phone sounded a bit unsure and then stated that the balance is the balance whether I pay today or not. Maybe I will see if I can get someone a bit more savvy on the phoneSea_Shell said:TheAble said:Likely loans does allow overpayments though, and would appear to have a representative Apr of 60%. Is there not a strong case for tackling this one first?

I would have though that even when a loan has all the interest "pre loaded" onto your fixed monthly payments, any over-payment would bring down the total payable over the term of the loan. So yes, I think this option would need investigating further, especially if it has a higher APR than the others.

I can see where the confusion would lie though, as you don't have an ongoing "balance" as such, like you do with a CC, overdraft or Credit account.

Do you have all the T& C's to hand?

That should detail any early redemption penalties or maximum payment without penalty, if any, and how interest/period would be recalculated.

Best to be armed with the information before you ring to "confirm" with them.How's it going, AKA, Nutwatch? - 12 month spends to date = 3.24% of current retirement "pot" (as at end December 2025)0 -

True - I think they send me a statement each year on email I will dig that out, I must have it somewhere in the depths of my emails.Very (Shopping) £796.16 Paid in FULL as of 17/08/2021

Simply Be £1463 £1432 £1195.13 £801.02 £645.24 Paid in FULL 30/09/2021Likely Loans £2465.73 £2191.76 £1917.79 Paid in FULL May 2022

Overdraft £500 Paid in FULL Jan 2023

PayPal Credit £566.53 Paid in FULL Jan 2023

Total debt £5824.89 at the very start of DFW Journey.

Current debt £5,028.73 £4997.73 £4384.31 £3990.20 £3823.06 £2260.37 £1066.53 £0.00

Debt added since start of journey £9000 (borrowed from partner for car)

Current balance of £8550 £8150 Paid in Full June 2022

My debt free diary:

https://forums.moneysavingexpert.com/discussion/6291011/debit-free-diary-starting-august-2021-target-may-2022#latest0 -

Different products/lenders have different ways at looking at debts and have their own credit scoring so does not mean you have no chance of a 0% balance transfer or money transfer card, you may want to check your eligibility on MSE's credit club to see, which does not leave permanent markers, also some banks do initial eligibility checks on their site (such as santander) without leaving a footprint first, so may be worth a look.rigare11a said:

Thank you, I did think about 0% cards but I was recently declined finance application so don't think I would get approved for a card.thriftychick said:Good luck with your debt free journey, you seem really motivated and on the ball.

Personally, I would repay the overdraft first, save up an Emergency Fund and then snowball the debts It worked for me.

Can you transfer any of the debt to 0% cards even if it is just part of the amount?MFW#105 - 2015 Overpaid £8095 / 2016 Overpaid £6983.24 / 2017 Overpaid £3583.12 / 2018 Overpaid £2583.12 / 2019 Overpaid £2583.12 / 2020 Overpaid £2583.12/ 2021 overpaid £1506.82 /2022 Overpaid £2975.28 / 2023 Overpaid £2677.30 / 2024 Overpaid £2173.61 Total OP since mortgage started in 2015 = £37,286.86 2025 MFW target £1700, payments to date at April 2025 - £1712.07..1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards