We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Cash in Stock ISA and put into SIPP?

older_and_no_wiser

Posts: 373 Forumite

I just had a eureka moment....or was it?

I think it would make sense for me to cash in my stock ISA and invest it in my SIPP. I'll get the 20% HMRC topup.

The stock ISA is valued at just over £30k. I will need to do this next financial year, as I will be hitting the maximum I'm allowed to contribute (£40k) this year with my regular contributions and extra ad-hoc payments I've already made

Assuming I don't need access to this money until I retire, is there any reason I shouldn't be doing this? Am I missing anything obvious? Is there any benefit (tax wise?) in having that ISA once I retire and need access to my savings/pension?

For info, I'm planning on retiring in around 5 years and going into flexi drawdown and keeping my SIPP invested into retirement. I have 2 SIPPs - one workplace which I'm contributing via salary sacrifice just over £800 a month. The other one is a personal SIPP which I'm contributing £400 a month to.

I think it would make sense for me to cash in my stock ISA and invest it in my SIPP. I'll get the 20% HMRC topup.

The stock ISA is valued at just over £30k. I will need to do this next financial year, as I will be hitting the maximum I'm allowed to contribute (£40k) this year with my regular contributions and extra ad-hoc payments I've already made

Assuming I don't need access to this money until I retire, is there any reason I shouldn't be doing this? Am I missing anything obvious? Is there any benefit (tax wise?) in having that ISA once I retire and need access to my savings/pension?

For info, I'm planning on retiring in around 5 years and going into flexi drawdown and keeping my SIPP invested into retirement. I have 2 SIPPs - one workplace which I'm contributing via salary sacrifice just over £800 a month. The other one is a personal SIPP which I'm contributing £400 a month to.

0

Comments

-

In "top up" terms it's 25%, not 20%.

Even if paying basic rate tax on the pension there is a 6.25% gain going via the pension.

Potential downside is loss of access to the money between now and when you hit 55. And if you do then take any taxable income (other than an annuity) you will limit yourself to contributing £4k/year.1 -

Thanks for that @Dazed_and_C0nfused

I'll be 53 next month and definitely won't need access to that money before 55. Hopefully retiring when I'm around 58 and may not need to dip into the SIPPs for a couple of years after that0 -

Not getting close to the Life Time Allowance (£1m plus)?0

-

Nope. - currently at £410k and now adding approx £16k a year gross.MX5huggy said:Not getting close to the Life Time Allowance (£1m plus)?0 -

Given your age and lack of need as well as you being at least a year older and no more than a year from being 55 before the last goes in that looks like a good plan.2

-

In hindsight we maybe should have done that, and ploughed more into pensions?

When we first started building up our ISAs, pension freedoms weren't a "thing" and so we were making provision for the years from 50 to 65.

Once access was available at 55, we should maybe have changed tack, and ploughed the max into pensions, to gain the uplift.

As it stands we have approx 35% of our retirement funds in S&S ISA's and 65% in DC Pensions. Excluding a cash float.

If we had moved money from ISA to pension, we would have gained on the way in, but lost on the way out. Is that a zero sum game?? - No, just realised that we would still have been 6.25% better off.

Oh well. Too late for us now, as we've both already finished work, so we're restricted to our £3600 per year gross contributions.How's it going, AKA, Nutwatch? - 12 month spends to date = 3.24% of current retirement "pot" (as at end December 2025)0 -

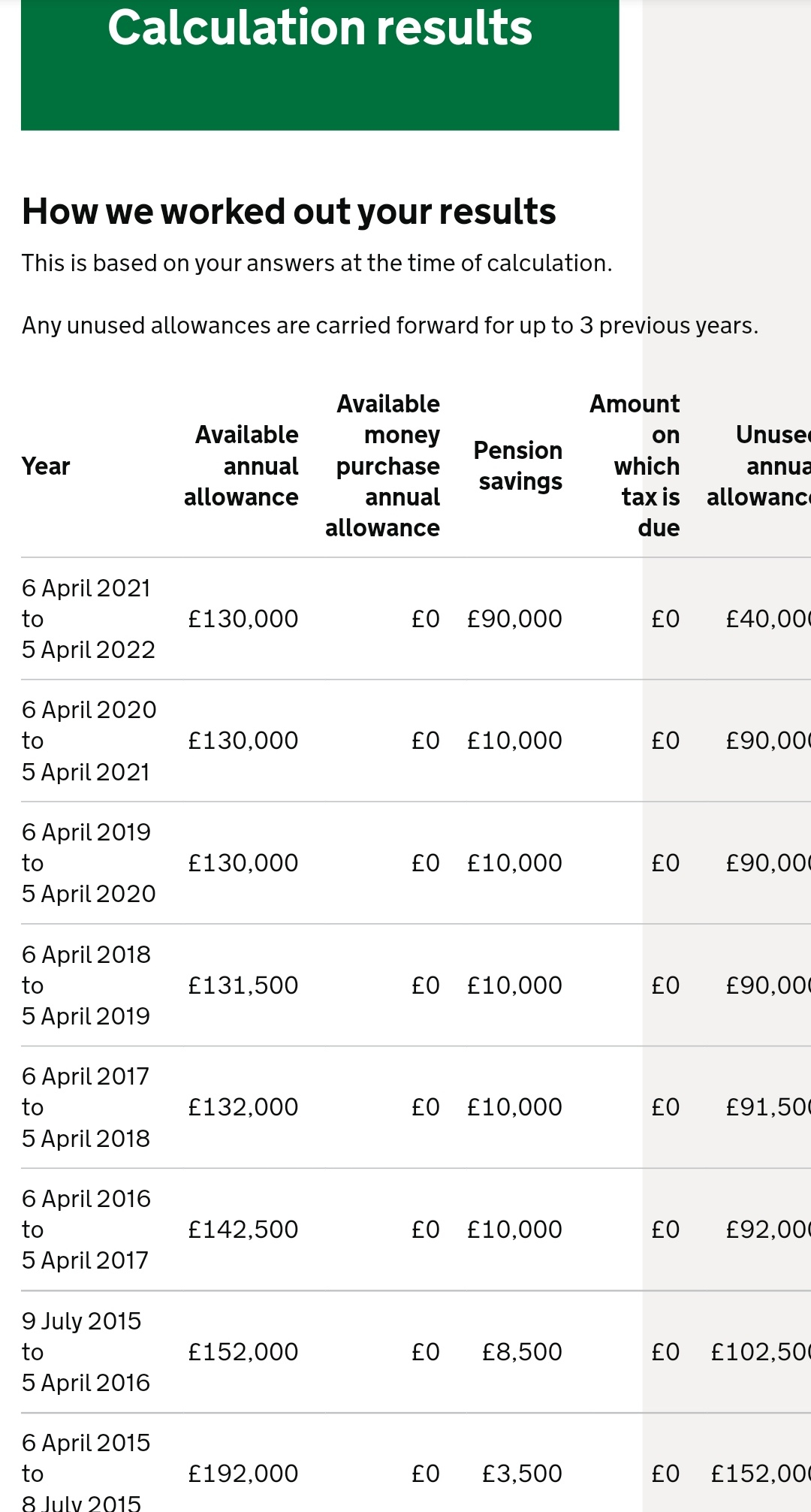

I mentioned I've hit my limit for pension savings this financial year. However, I have a backdated allowance. I'm on a £50k+ salary and until this year I've only been contributing around £9000 a year into my pensions. I've ramped it up this year as I've only just been enlightened regarding how pensions and investments actually work! I ran the figures through the HMRC calculator and it appears I can contribute more this year...

0 -

Obvious bit of missing information: how much do you earn?

You can't have more going in to your pension than you earn.

If you are significantly into the HR tax band, then you can possibly benefit from HR tax relief on your contribution.

If you are already getting £16,000 pa into your pension, then there's capacity to have an additional £24,000 pa.

How much you actually pay in each year might be something to plan, depending on how much of this (if any) might attract HR relief.

Another thing to consider might be if you were able to sal sac instead of making a net payment from your ISA.

This would be to increase your sal sac so that you were only taking home £12,500. You would then use the ISA money to make up your foregone monthly salary. In this manner, the sal sac would attract 32% relief, possibly more if your employer has matching and / or shares the saved ERs NI with you.

Yet another thing. Why are you paying into two SIPPs?

The company one will attract NI relief as well as tax relief, and may also attract further company matching and / or ERs NI.

The non company one will simply attract tax relief. If you are BR taxpayer, then one is getting 32% (+) relief and the other is 20%.

(If you are dissatisfied with the available fund selection in your company SIPP, then you may be able to make a partial transfer from it into your other SIPP.)1 -

Don't forget that even if you could afford to pay more i.e. from the ISA, you will still be constrained by your earnings.

This is useful article,

https://www.pruadviser.co.uk/knowledge-literature/knowledge-library/interaction-of-tax-relief-and-annual-allowance/0 -

This is exactly what I have been doing. I would not continue to contribute to the non workplace scheme (£400).older_and_no_wiser said:

For info, I'm planning on retiring in around 5 years and going into flexi drawdown and keeping my SIPP invested into retirement. I have 2 SIPPs - one workplace which I'm contributing via salary sacrifice just over £800 a month. The other one is a personal SIPP which I'm contributing £400 a month to.

Each year I sell £XXXXX investments from our ISASs and use this money to supplement increased workplace contributions via SS. Mine is a little nore complicated as my main scheme is a DB scheme but I pretty much manage to contribute sufficient to take me down to the NMW level (which you cannot sacrifice below).Personal Responsibility - Sad but True

Sometimes.... I am like a dog with a bone0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards