We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

USS - General discussion

Comments

-

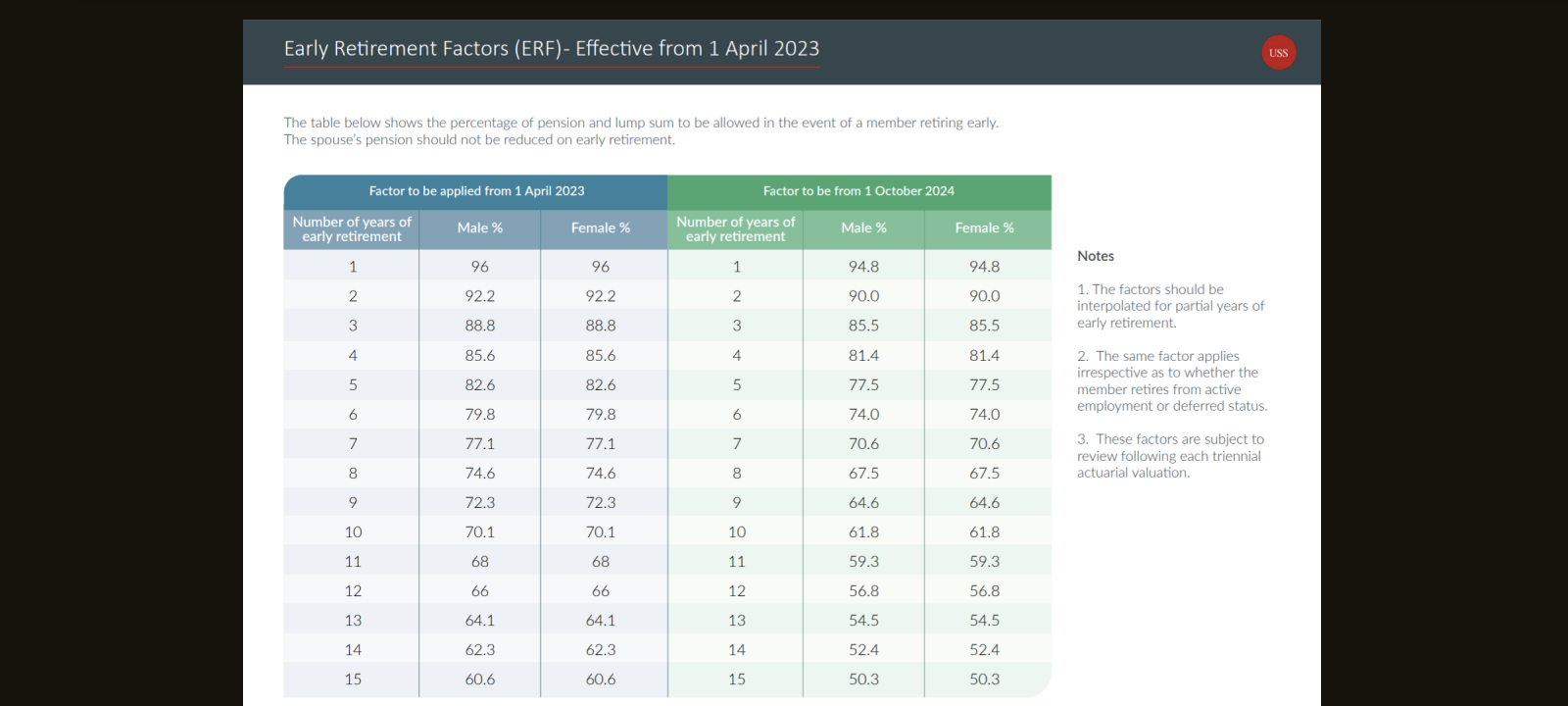

Update on my USS complaint re me only taking pension in Feb 24 as USS advised ERFs changing from April 24, which as we now know is October 24.

i have had a response and they provided a quote showing what I would have got if I had taken pension from April 24.

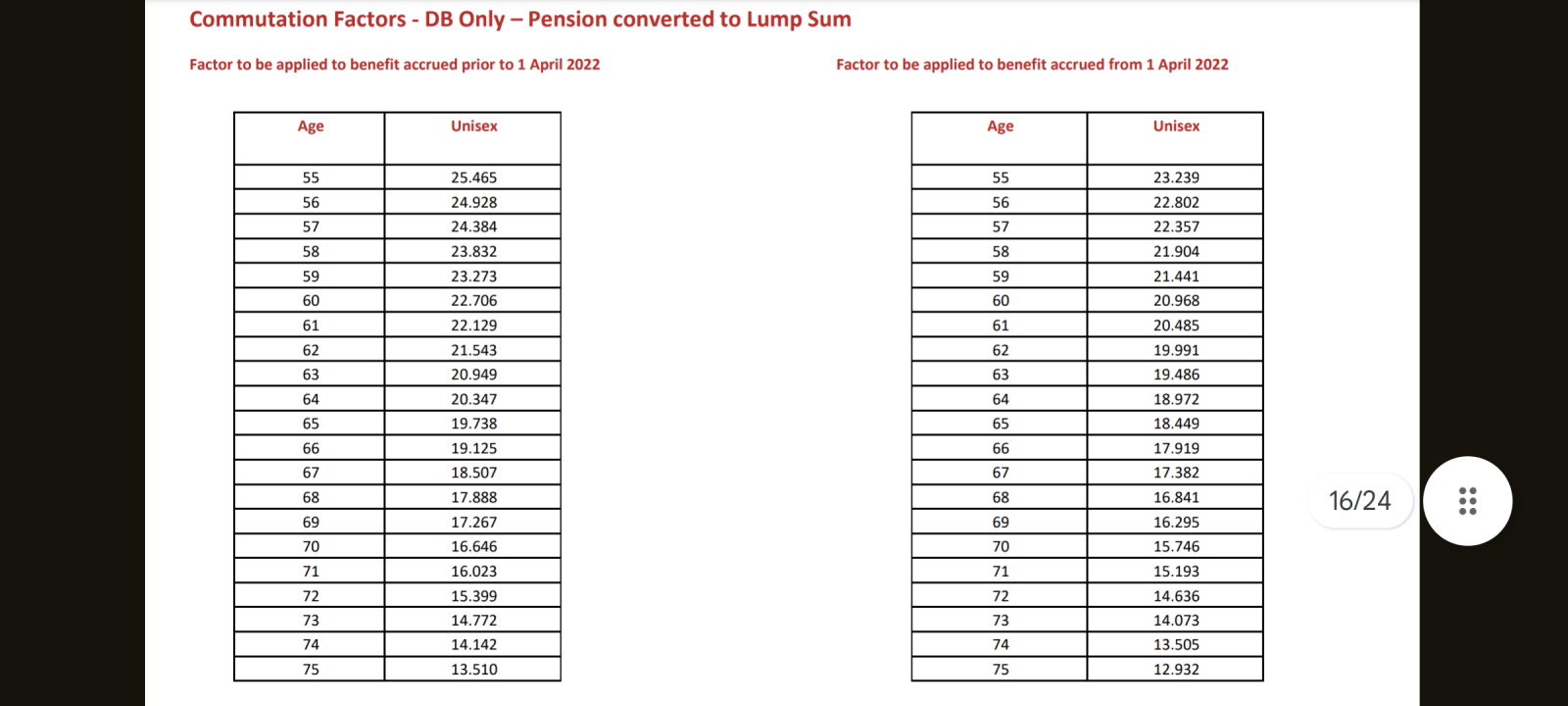

Turns out that although the ERF reduction isn’t taken place until October 24 they have unbeknown to me (and I think most on here) reduced the commutation rates from April 24.When I compared my Feb 24 and new April 24 quote as i have taken the max free lump sum I was after all better taking it in Feb 24 as the new commutation rates would have reduced my pension further from. April 24,

For me taking it at 57 the commutation rate has changed from 23.8306 to 18.9478.

So not only have they reduced the ERFs from October 24 they have also reduced the commutation rates from April 24.Money SPENDING Expert0 -

Thanks bluenose1 that’s a significant factor and a double whammy. It doesn’t get better at all!1 -

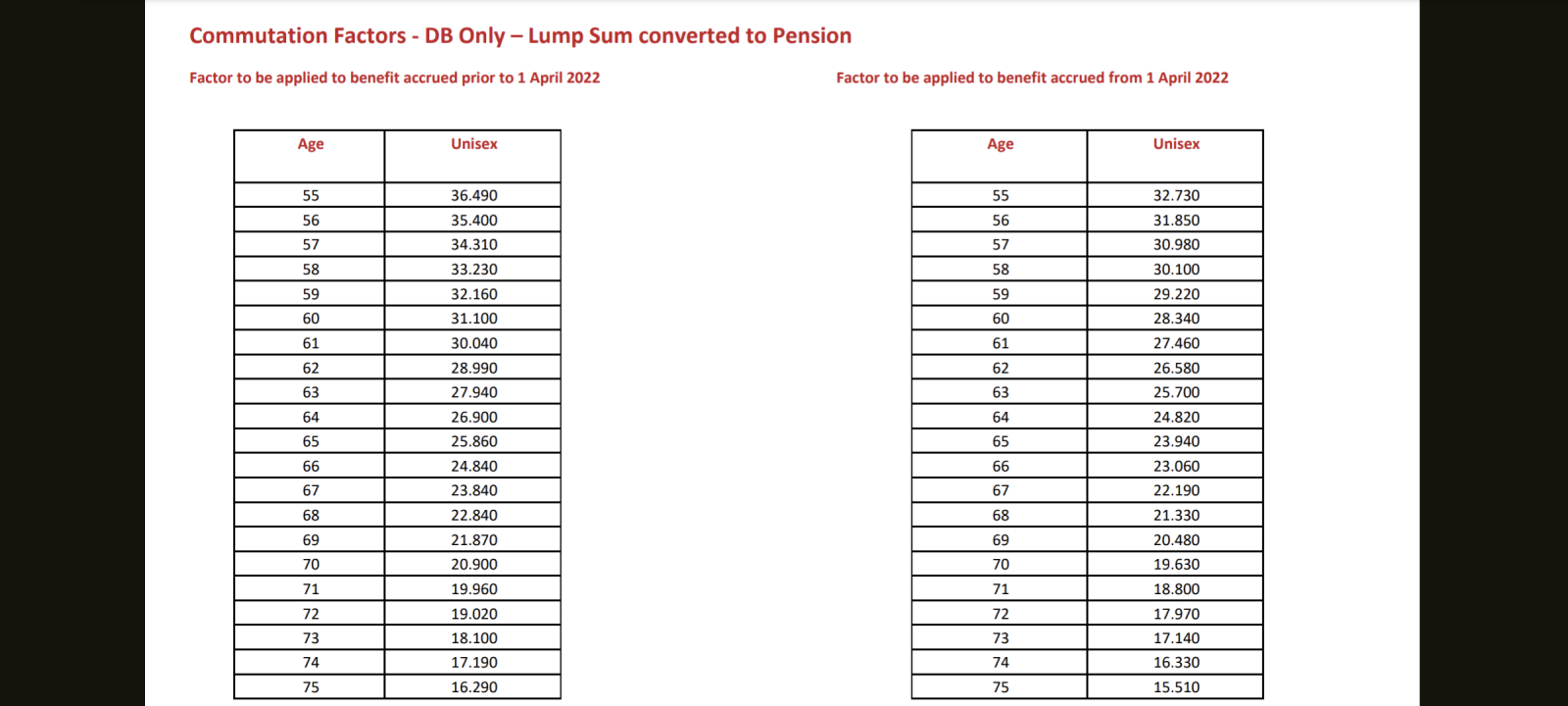

I thought that they left the commutation revisions with an April change because they were generally more beneficial for retirees? I'd have to check (I have a vague memory of posting a calculation?), but I thought the commutation factors for converting TFLS to additional pension improved, i.e. it cost you less TFLS to buy pension than for the previous factors.0

-

I commutated some of my pension into an increased tax free lump sum and that has reduced quite a bit from April 24.MPLMPL said:I thought that they left the commutation revisions with an April change because they were generally more beneficial for retirees? I'd have to check (I have a vague memory of posting a calculation?), but I thought the commutation factors for converting TFLS to additional pension improved, i.e. it cost you less TFLS to buy pension than for the previous factors.

Not sure about converting TFLS to pension being improved, hopefully so for those who want to do that.

Money SPENDING Expert0 -

IIRC, the new reverse commutation factors were more favourable but not the commutation factors.MPLMPL said:I thought that they left the commutation revisions with an April change because they were generally more beneficial for retirees? I'd have to check (I have a vague memory of posting a calculation?), but I thought the commutation factors for converting TFLS to additional pension improved, i.e. it cost you less TFLS to buy pension than for the previous factors.1 -

That seems to be the case comparing the past IFA guides I have copies of.NickBFS said:IIRC, the new reverse commutation factors were more favourable but not the commutation factors.

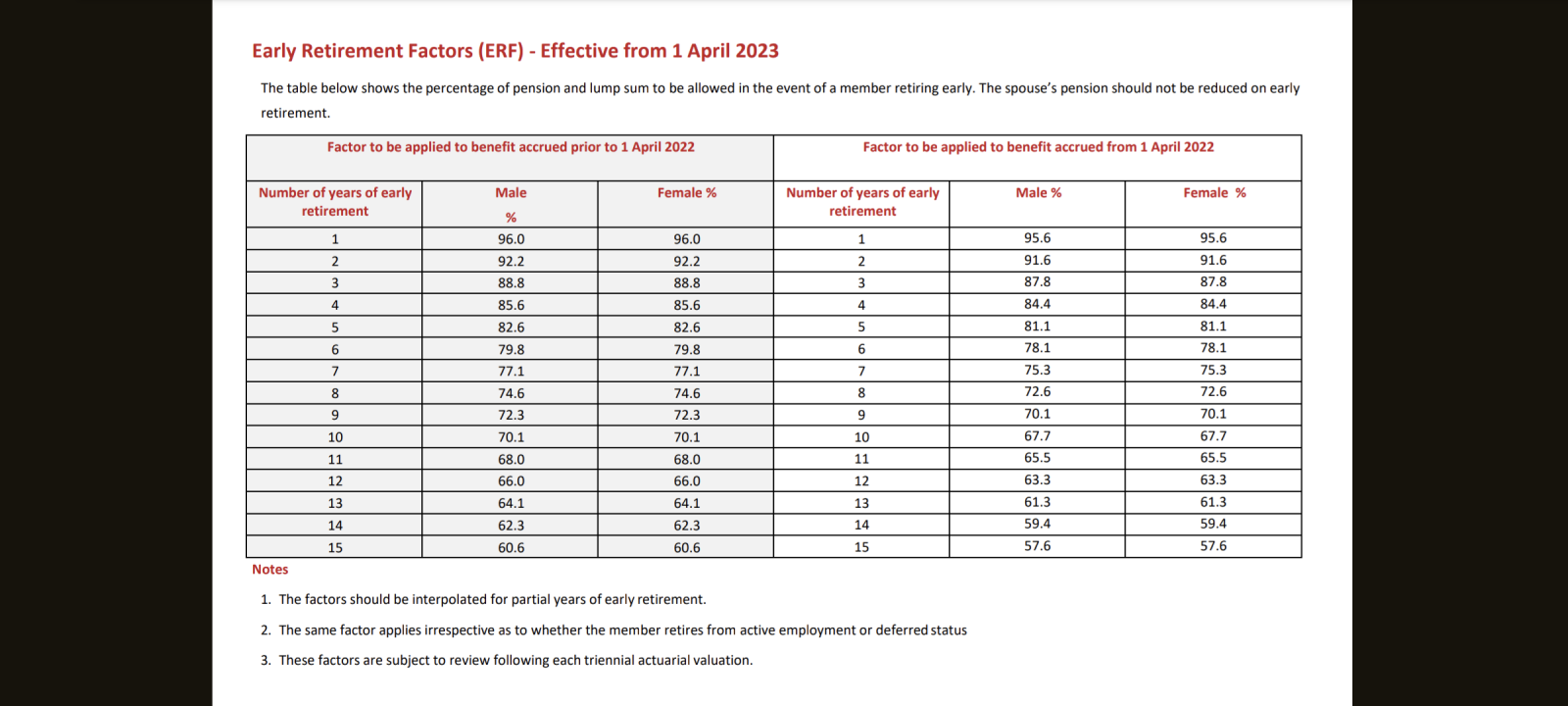

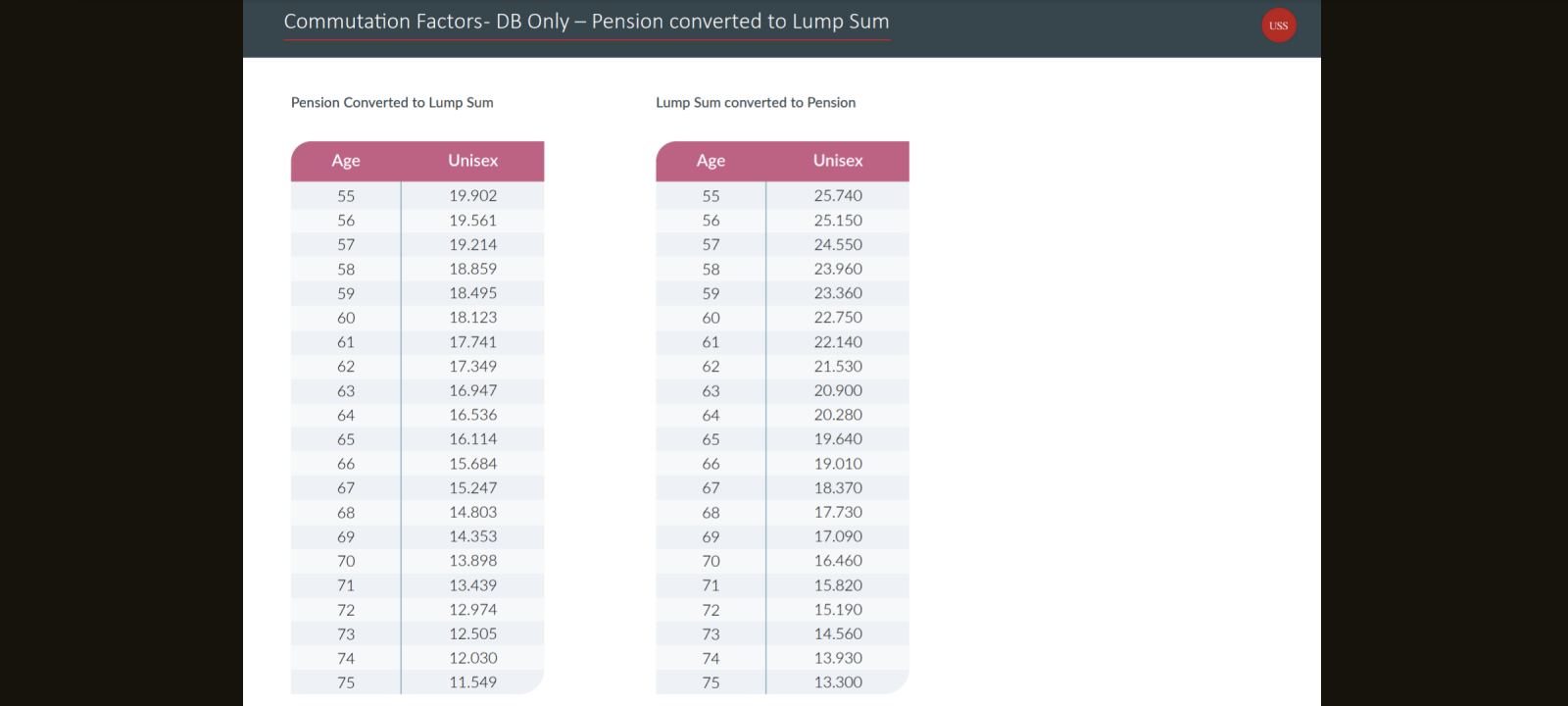

Screenshots below if useful. Old tables first from guide I downloaded in mid March, new ones from the new guide I first downloaded on 4 April, which is the one currently downloadable.

The new guide (and webpage) rewrites history somewhat as they compare the 1 Oct 2024 changes to a single 1 April 2023 factor, when there were actually different factors for years pre and post 1 April 2022, although they compare the more favourable one of the two, making the reduction in October look worse. @bluenose1 did they use the split commutation factors, or just one?

1 -

I have noticed that the retirement income builder has now been updated to include up to 31/03/2024. Does anyone know if this includes the £215 uplift, or is this still to be added? I seem to remember someone saying that the uplift would not be added until 1st June.0

-

I thought that the uplift was in April, which should mean that it would not be included at the 31/3/24 cut-off point?0

-

If you look at the amount that was added it's quite a bit over what was meant to be the accrual limit for RB benefits for a single year. That makes me suspect that it includes the uplift... though USS often make these updates, get them wrong in some way, then reverse them so.... who knows.

edit: It's less than £215 more though I think, unless the previous year has been adjusted for inflation?0 -

That's what I thought Dave. It seems too high, but not high enough to include the uplift?1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 248K Work, Benefits & Business

- 605.2K Mortgages, Homes & Bills

- 178.9K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards