We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Help to buy advice

Ybe

Posts: 459 Forumite

Generally with help to buy, is it better to take out the largest equity loan possible or is better to only take out the percentage you need as an equity loan and put the rest to mortgage?

The advantages I see of taking out the largest equity loan possible are that it’s 0% interest for 5 years, it’s an equity loan so if the market value of the property goes down (possible on an inflated new build), the equity loan lender will take part of the hit as the amount repayable will also go down.

The disadvantages I see is that if aiming to repay the equity loan 100% then it might be more difficult to do this (although this may be very difficult anyway with inflated new builds). Another is that if the property goes up in value and you sell, you’ll have less of a share of the equity.

0

Comments

-

When you redeem the HTB loan, they will take the figure the property is valued for at that time or what you sell for, whichever is highest, so be aware of that. If you're not selling and redeem after 5 years you'll still pay against the new valuation or what you paid if the property has decreased in value so the lender is protected. I would therefore only borrow what you absolutely have to to avoid giving away too much equity in the future.0

-

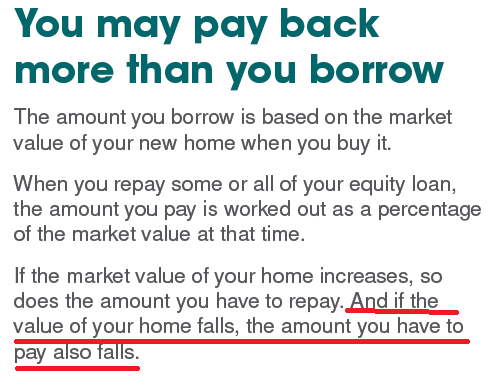

Louise_G_1983 said:When you redeem the HTB loan, they will take the figure the property is valued for at that time or what you sell for, whichever is highest, so be aware of that. If you're not selling and redeem after 5 years you'll still pay against the new valuation or what you paid if the property has decreased in value so the lender is protected. I would therefore only borrow what you absolutely have to to avoid giving away too much equity in the future.@louise_g_1983 That isn't correct afaik. If you're not selling, if the property has decreased in value, your equity loan amount also goes down in the same proportion.From the govt H2B equity loan guide -

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

2 -

Crunch the numbers.

There are 2 elements to the savings with H2B

up to 20% interest free

up to 75% at a lower rate than if you borrowed at higher LTV eg. H2B 75% is cheaper than 95% LTV without H2B

once you have the rate options you can run the 5year model and work out how much the house can go up before you are losing out using the same payment.

For a 75/95 scenario it was over 40% last time I looked but the 95% rates are creeping down

I think most lenders tend to have 75% H2B only some may have better rates if your LTV on the borrowed is a bit better can

You still need to have a clear exit plan for around the 5 year mark or be ready for the interest to start..

0 -

Apologies, Im sure those were the terms of my HTB scheme but I'm no expert.0

-

OP, personally I would take out max and it's 0% and also gives me a hedge against prices falling.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.7K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards