We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Has anyone gotten a mortgage with a transfer deed

Comments

-

Fingers crossed 🤞

You should check this with your solicitor though. The HSBC conveyancing handbook says this, hope this is outdated or something -

0 -

Really don’t know because when I call and tell them the seller has owned for less than 6 months they said it’s ok but don’t know for sure. Solicitor said will raise once mortgage is offered. Are there any banks that issue mortgage can deposit 25%lonibra said:Fingers crossed 🤞

You should check this with your solicitor though. The HSBC conveyancing handbook says this, hope this is outdated or something -0 -

Won't it be too late by then if the solicitor waits for a mortgage offer, checks and it can't proceed? Your solicitor should be able to look up the HSBC solicitor handbook and check now so you can get plan B in place.

I don't know what banks sorry, I just rely on my MB. I have only once bought a property (BTL) on auction and used a bridge mortgage and later remortgaged to normal one. Anything else was too risky because I only had 4 weeks (I think) to complete or I lose 20k. I think I needed something around 30% deposit.0 -

Thanks I Will email and call my solicit to check the solicitor’s handbook. What was bridge morrgage like will look into this option in case, how long did you have to wait to transition from bridge mortgage to normal mortgage? I was given 6 weeks but 10 days has already gone.lonibra said:Won't it be too late by then if the solicitor waits for a mortgage offer, checks and it can't proceed? Your solicitor should be able to look up the HSBC solicitor handbook and check now so you can get plan B in place.

I don't know what banks sorry, I just rely on my MB. I have only once bought a property (BTL) on auction and used a bridge mortgage and later remortgaged to normal one. Anything else was too risky because I only had 4 weeks (I think) to complete or I lose 20k. I think I needed something around 30% deposit.0 -

From what I remember it took about 2-3 weeks from the auction to completion. But my MB had everything ready to go before I started bidding.

After completion, some banks will not remortgage within 6 months of purchase but my MB found a cheap one that does and I think I did it after I had a tenant installed so about 2 months.1 -

Going through all the lender's criteria and it appears Virign lend on such but will need to call them tomorow as i do not know how much the seller purchased the property for.

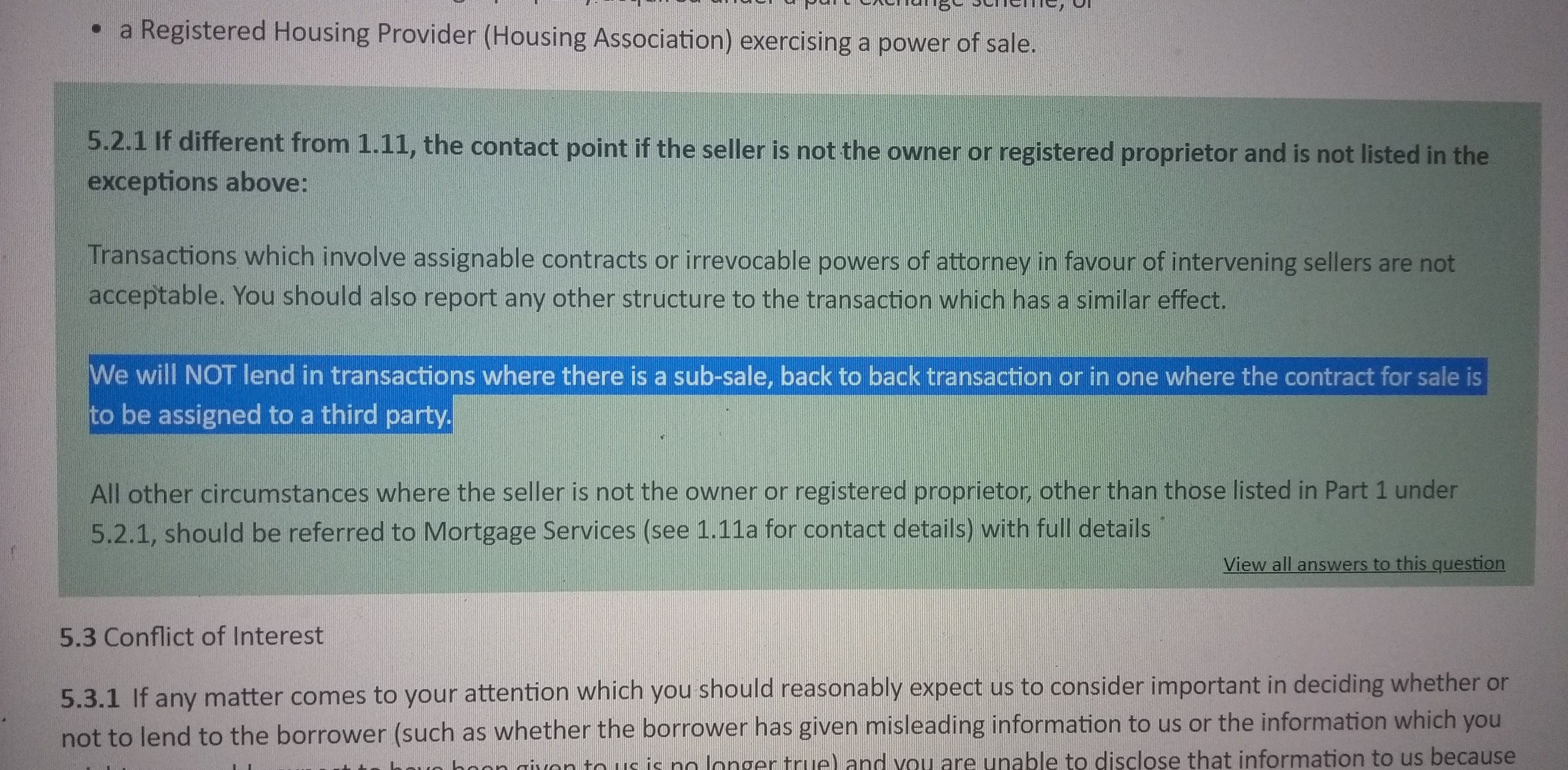

Sub-sales and Back to Back TransactionshideA Back to Back transaction takes place when a customer purchases/exchanges on a property then attempts to take out a mortgage based on an enhanced market value within six months of the original purchase/exchange. Virgin Money Policy in these cases is to lend against the lower of either the original purchase price or valuation.

A sub-sale takes place when a customer is purchasing a new build property from a third party (not the builder) and is paying a premium price but the third party is purchasing from the builder at a lower price or in a Stamp Duty Land Tax (SDLT) / Land and Buildings Transaction Tax (LBTT) mitigation scheme. Our policy for sub-sales is to lend on the lower of the purchase price or property valuation in the original transaction until a minimum of six months from completion and as such, the third party must be noted at the Land Registry as the registered owner for a sub-sale to proceed.

A Back to Back purchase occurs where a customer is purchasing from a third party who has purchased the property within the last 6 months at a discounted/lower price. We will only lend on the lower of the purchase price or property valuation in the original transaction unless significant improvement has been carried out to the property.

0 -

At present i do not know the price seller bought for. The transfer deed will have the information on the price seller bought for, i have informed my solicitor to request transfer deed. Last communication was that the seller's solicitor have sent the draft contract. They did state that "unless significant improvement has been carried out to the property." the house was previously 2 bedrooms, now 3 and bathroom got renovated. I will call the bank up tomorrow morning to get more information. When i bidded on the property i was not aware the vendor has owned the property for less than 6 months. I have savings and can get family to chip in but wont want so much cash tied into 1 property. Hopefully 25-30% max will be required and in the future 2+ years can remortgage and release equity.user1977 said:

Do your sums work if the lender is using the "original" price rather than the one you've bought at?london21 said:"Our policy for sub-sales is to lend on the lower of the purchase price or property valuation in the original transaction"

0 -

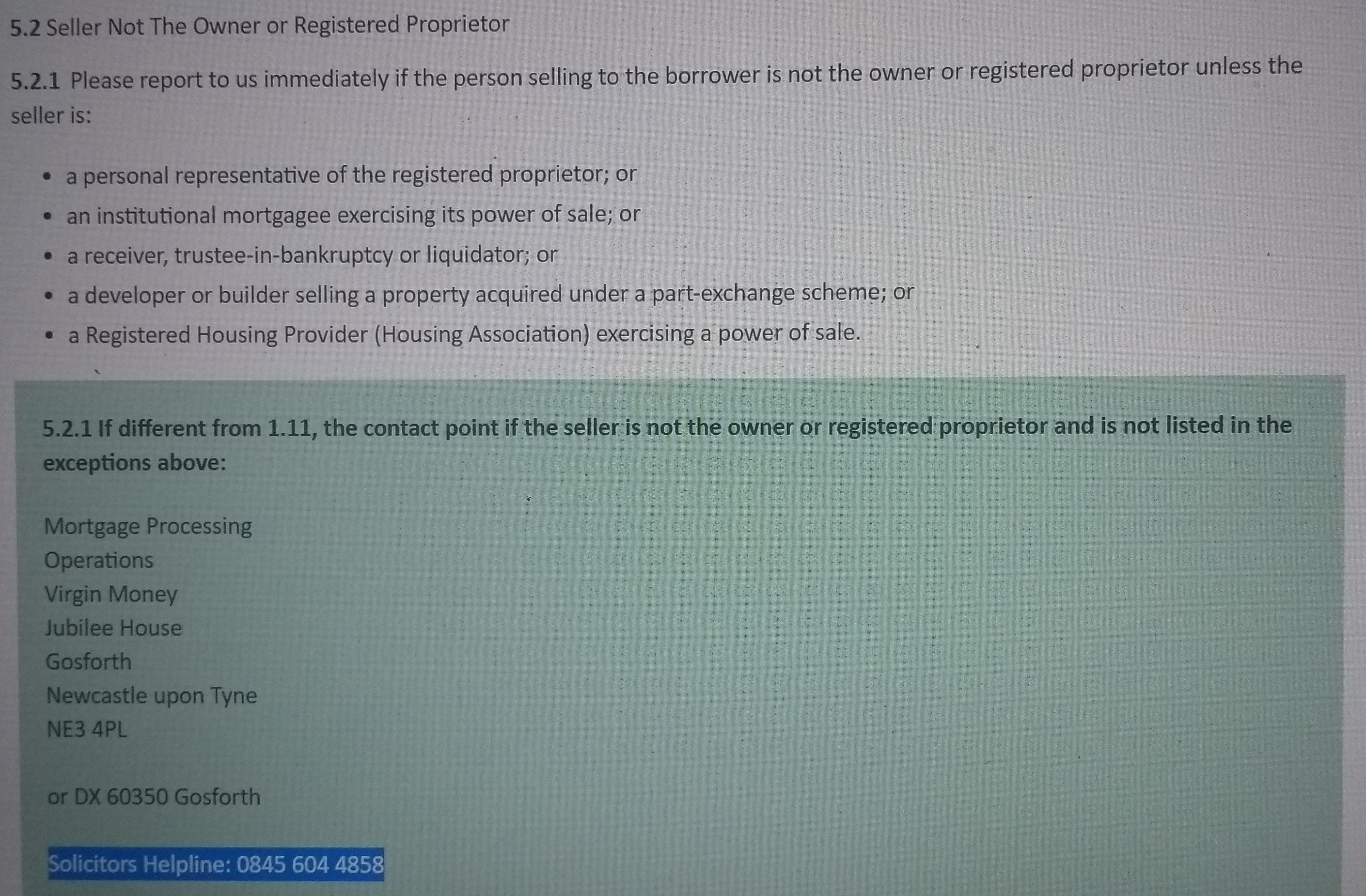

OP, Virgin's conveyancing handbook lists a few exceptions for sub-sales, do any of them apply to your purchase?

Also it lists a helpline for solicitors. You could save a wasted application by getting him to call and confirm that it's ok with Virgin before you apply. Otherwise you have the risk of finding out a few weeks into the process.

1 -

That's a helpline for solicitors dealing with current cases - I don't think they'll welcome theoretical enquiries from solicitors about mortgage offers which aren't even applications yet (or that the solicitor will welcome the prospect of hanging on the phone to a call centre to find out).lonibra said:Also it lists a helpline for solicitors. You could save a wasted application by getting him to call and confirm that it's ok with Virgin before you apply. Otherwise you have the risk of finding out a few weeks into the process.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.9K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards