We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Want to become a Forum Ambassador? Visit the Community Noticeboard for details on how to apply

Help to buy equity loan

Runningmad

Posts: 79 Forumite

After speaking with a broker it looks like we could buy a house using the equity loan.

Looking for advice from anyone who has gone down this path. How do you propose to payback the loan? Or just pay the interest until you sell? The only worry I have with that is the increase in interest rate each year could end up being huge.

Would just like to get other view points as its such a big decision.

Thank you

Looking for advice from anyone who has gone down this path. How do you propose to payback the loan? Or just pay the interest until you sell? The only worry I have with that is the increase in interest rate each year could end up being huge.

Would just like to get other view points as its such a big decision.

Thank you

0

Comments

-

We have recently purchased a house using this scheme (few months ago). It’s not for everyone but for us it was the only way we could get on the ladder as it stood now. We aim to use remortgaging in the future to pay off at least some of the loan and the perhaps the rest a couple of years later. We did put in 10% deposit of our own as well though.Runningmad said:After speaking with a broker it looks like we could buy a house using the equity loan.

Looking for advice from anyone who has gone down this path. How do you propose to payback the loan? Or just pay the interest until you sell? The only worry I have with that is the increase in interest rate each year could end up being huge.

Would just like to get other view points as its such a big decision.

Thank you2 -

Just to add as well that our house we were in was being sold and didn’t want to move again as it was so wasteful chucking more money at rentals. Affordability wise we could get a bigger mortgage but didn’t have the huge deposit we needed at the time!0

-

Thank you. I will look into remortgage. It's so difficult, and I worry we have left it too late as we are in our 40s and prices are so high, for us this seems the only way. Thank you for replying.0

-

I assume the broker is providing advice on the equity loan and explaining it to you so what's your understanding on the equity loan interest? Its quite easy to get mixed up on how the interest is charged. Using the word 'huge' gives me the impression that it hasnt been explained to you properly.Runningmad said:After speaking with a broker it looks like we could buy a house using the equity loan.

The only worry I have with that is the increase in interest rate each year could end up being huge.

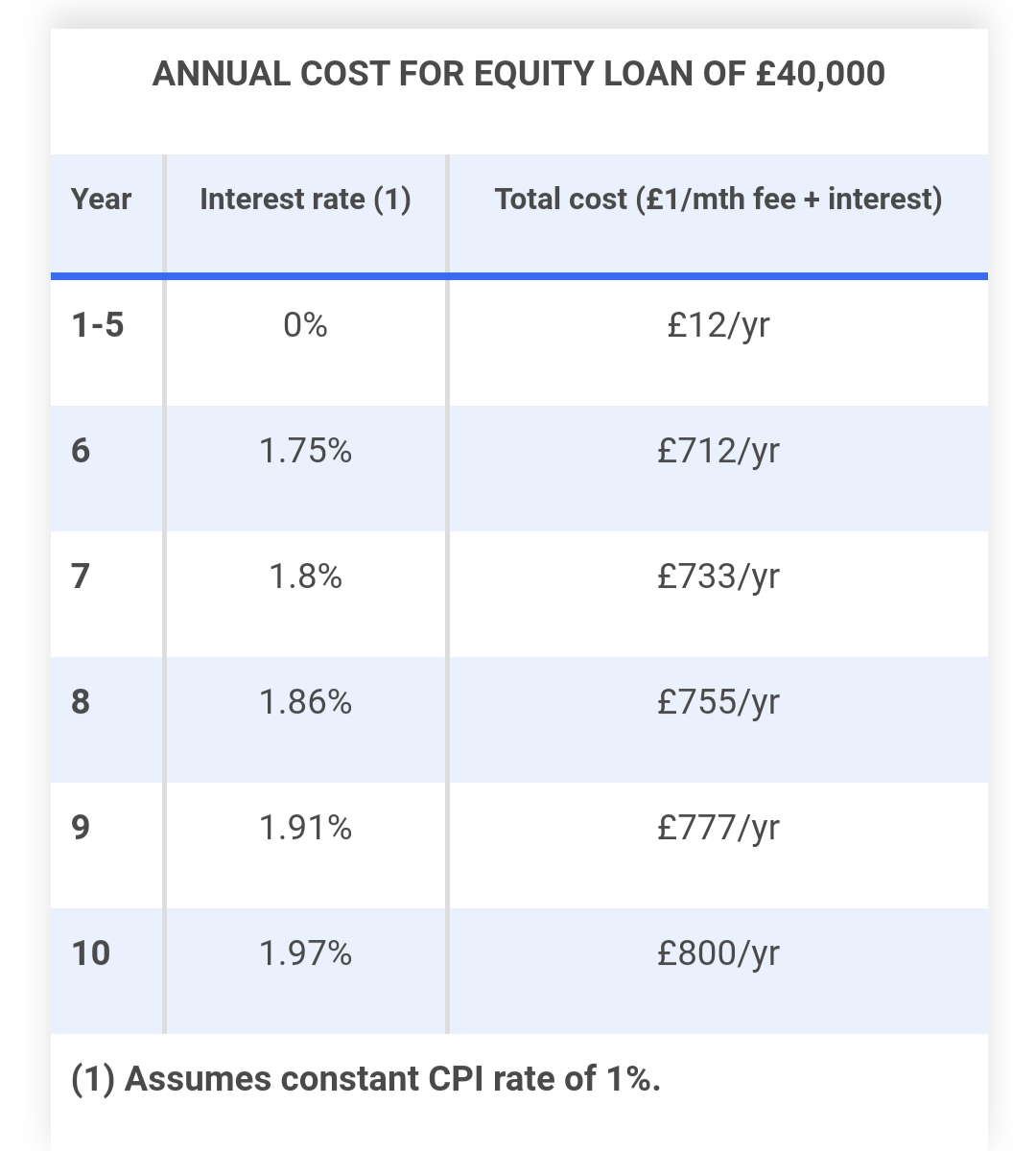

Using the standard examples, at year 10 the interest rate is still under 2%. Not what i'd call huge considering the alternative is a deal with a smaller deposit and rates above 3%.

1 -

Thank you for the reply. This is why I appreciate other points of view.

On the help to buy website it states the interest will go up each April at the CPI plus 2% that's why I was thinking after a period of time that could increase quite a lot? Thanks again.0 -

@runningmad It's CPI+2% OF the interest rate. So if the starting interest rate is 1.75% and CPI is 1%, that would mean a rise to 1.8025%.

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

3 -

Oh thank you for making that clear, I feel a bit stupid now I thought the 2% was of the loan not the CPI rate. That makes it much more affordable. Thank you0

-

Hi. We also got the scheme, basically we have 5% deposit, 10% HTB, and 85% mortgage. Really helpful as it’s the only way for us to get into the propery ladder. Also the stress of living in a flat for so many years and WFH with no outside space really pushed us to finally buy a house.We plan to pay the HTB in full on year 3. We are a bit worried that the value of the house might increase in the next few years so hope we can pay it soon in full. We don’t want to add it in the mortgage because as it is our monthly payment is already quite high and adding the HTB will definitely increase the LTV and interest so we will surely struggle paying it monthly. I hope everything goes to plan.0

-

I ran some numbers a while back and house value had to increase something like 40% in 5 years to be worse of with HTB rather than the alternative of a 95% mortgage.

Covid got rid of the 95% option for a while but they returning but not always a like for like as there are different restrictions on the property.

Effectively you are a comparing HTB rate on 75% against 95% rates on 95% for 5 years as a starting point.

(although most looking at 95% would probably only fix for 2-3 years as rates can be lower on retention or SVR and LTV might improve)

95% are popping up around 4% with H2B 75% around 2% say over ~25years

per £100k(it scales for higher values) paying the same as the 95% rate £500pm

after 5 years

95%amount rate payment owing £95,000.00 4.00% £500.00 £82,845.19

H2B 75%amount rate payment owing £75,000.00 2.00% £500.00 £51,357.24

To be worse off with H2B the £20k equity loan needs to now be ~£31k that's a 55% increase in value over the 5years

The20% interest free and 75% on a lower rate makes a significant difference to the costs

(Interest/£100k at start £317 V £125)

capital raising H2B

With a 55% increase would be against <60% LTV

With zero increase against ~72%LTV

The 95% option ~83% after 5 years

Where affordability is not the limit but deposit is H2B can still be a viable choice over the higher rate options.

The gap narrows if you have bigger deposits or take a 2y on 95% and get better rates after 2y

Where the £500pm/£100k is to much the H2B would be ~£277 which is a different choice, H2B or not buy

Whatever choice there needs to be an exit plan for the equity loan visibility of more money(income/lump) is still the better option

4 -

Wow thank you for your time and efforts, that was a lot of number crunching. Thank you

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.9K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.5K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards