We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Mortgage advice with ex

lizS78

Posts: 9 Forumite

Hope this isn’t too complicated.

The story so far.. initially looking at getting loft conversion for £25,000 and would give ex £40,000 but now decided on kitchen extension which I would need more money for. So plan to give ex £20,000 instead which he is happy with but he is entitled to £50,000 at current market value. Had financial settlement made 5years ago when divorced with the agreement that ex would get 33% when I sell. He has remained in mortgage till now.

As I’m not selling how do I sort out giving him lump sum now and leave rest till I can afford it? Do I just leave it and not give him anything as I’m not thinking about selling for long time.

Any advice would be appreciated or point in right direction would be helpful

thanks

thanks

0

Comments

-

https://forums.moneysavingexpert.com/discussion/6167395/mortgage-advice#latest

Settle the debt to the ex, release him from the mortgage and then think about extending and whatever else.Mortgage started 2020, aiming to clear 31/12/2029.0 -

Thanks for advice but I need more living space and if I give him all the money I won’t be able to afford it for years to come.0

-

lizS78 said:Any advice would be appreciated or point in right direction would be helpful

thanksI'm not sure anyone can give you advice on this as it really is a matter between the two of you...We might assume for example that when the financial settlement was struck it envisaged you needing to sell at some point in the future as the family grew to obtain something larger, it probably didn't envisage you deciding not to sell for many years but extend the house to avoid triggering the settlement clause...On the other-hand your ex may be entirely happy and have no expectation of receiving any money any time soon so he is happy to consent to the works you plan to do on the house and to remain on the mortgage...Does your ex still pay any part of the mortgage?

0 -

And by that time the kids would have flown the nest and you won't need the extra space.

Delaying paying your ex means that 33% could be a lot more in £ than it currently is because of it being extended or having a loft conversion.

However it seems like somehow you want to do everything to your house and give a little to your ex, still owing him quite a bit. You will need something drawn up to show what percentage you've repaid him, to avoid any arguments down the line. Revert back to your solicitor.Mortgage started 2020, aiming to clear 31/12/2029.1 -

He does pay the mortgage at moment but will take it on on my own. I am unable to move as house prices are unaffordable where I live for anything bigger.I understand that he will make more money if he waits. I was thinking that if he is coming off the mortgage then I would get house valued now then get solicitor to draw up agreement with that in mind which ever way we go.I would like to give him some money as he is struggling and he has paid towards house for 10 years.0

-

How are you proposing to fund the works to the house?0

-

Remortgage with additional money being lent.Thrugelmir said:How are you proposing to fund the works to the house?0 -

It is difficult to offer suggestions without more information.You mentioned that the financial settlement gave him 33% of the house when it is sold. Did that settlement include any provisions for maintenance payments or mortgage payments or perhaps both?Was there no limit on how long you could remain in the property without selling, such as when the youngest child was over 18?Can you meet the affordability requirements of your lender for the new increased mortgage without your ex being on the mortgage and is your income to support that mortgage entirely earned or does it require continued maintenance or other payments from your ex?There is probably a path through this that makes sense but it is hard to see where it is without more information as for example there could be a way to reduce the 33% of the house he is owed if there was a reduction in other payments he makes to you if you no longer need them...0

-

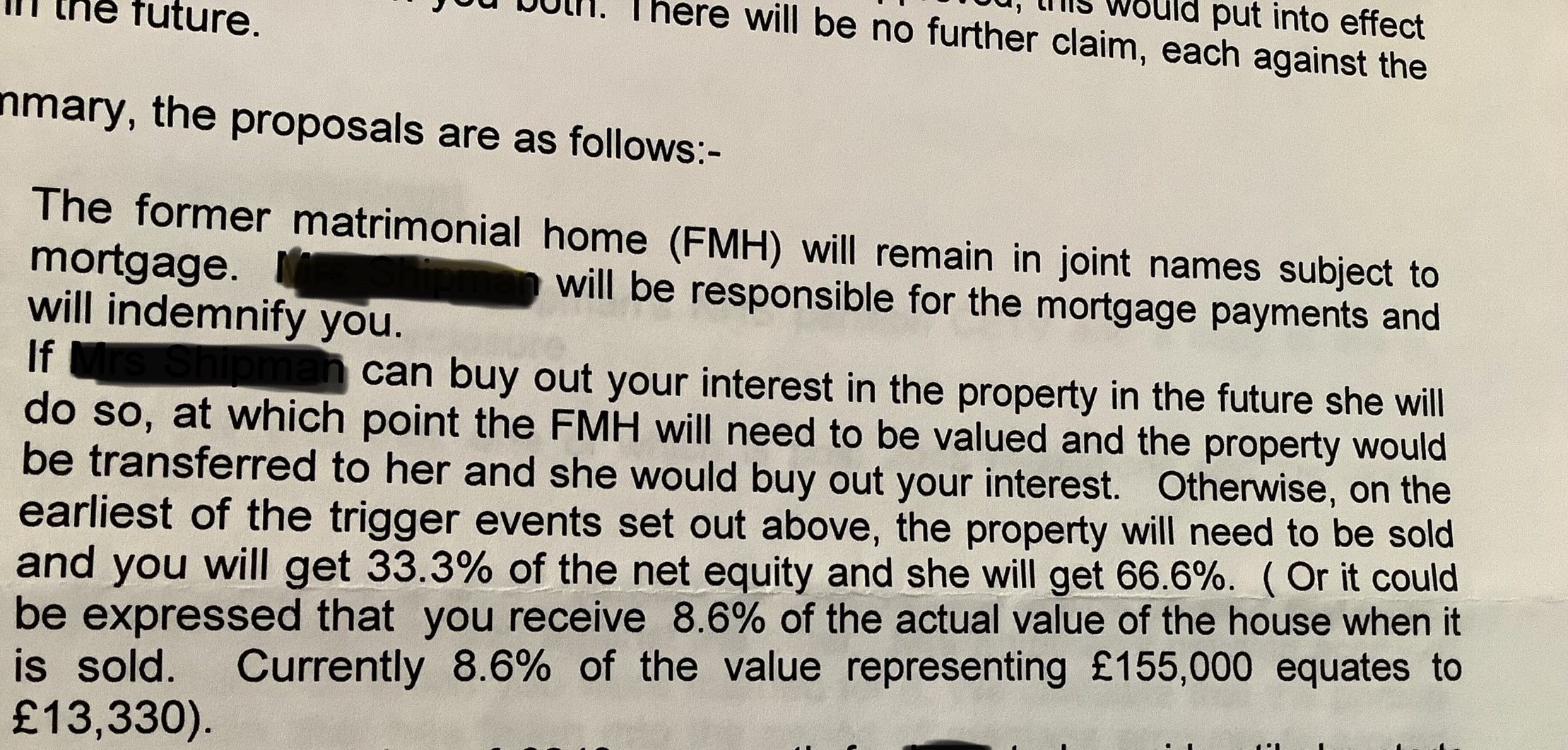

The settlement stated that ex would continue to support maintenance each month and until kids turn 18. Same for house, if I can buy him out, youngest turns 18 or I cohabit with someone else.

copy of settlement

the new mortgage will be done on my salary but I believe it has taken into account that I get maintenance, W have had joint mortgage with him paying £400 a month towards mortgage and kids.Hope that answers you.0 -

Thanks, that does make a few things clearer.Aren't you now in the position where as per the terms in the photo, you are able to buy him out, so you should do so?I know you would rather spend the money on extending the house but the terms you listed don't envisage that they simply say that if you can buy him out you will do so...I can't see how you could increase the mortgage as you plan to do without being obliged to pay him off and release him from the mortgage.Also, are you sure he is entitled to £50,000?What valuation are you using for the house, it would have to be over £580k for his share to be around £50k based on the numbers you showed above?

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.9K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.5K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards