We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

State pension forecast check

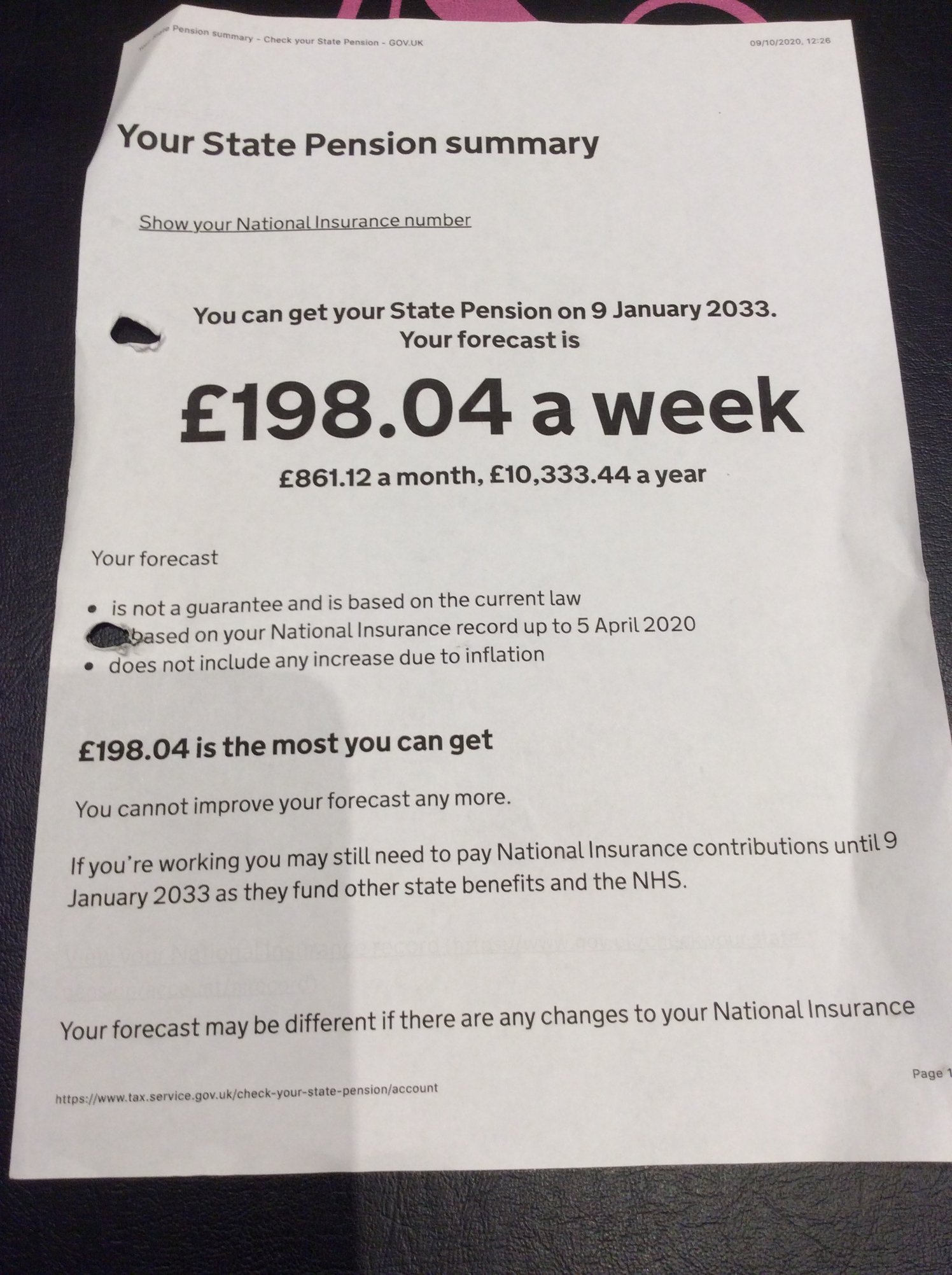

Good evening folks ,this is my wife’s pension forecast we have recently checked since she has turned 55 recently and we are wondering why it’s more than my forecast .Is this the additional state pension or another extra pension ?

Good evening folks ,this is my wife’s pension forecast we have recently checked since she has turned 55 recently and we are wondering why it’s more than my forecast .Is this the additional state pension or another extra pension ? She has worked for same company for 33 years and could not join final salary scheme until aged 33 .? Is this what she will definitely be entitled to . My forecast is £175 max (we are similar age) just curious as to the extra amount . Thanks for reading.

Comments

-

It will be her pre 2016 old scheme basic pension with the additional state pension. That amount has, apart from inflationary increases, been the same since April 2016. Does her forecast show a COPE amount ?Does your forecast show a COPE amount ?I suspect the main difference is the contracted out periods.1

-

So mine too says £175 max, I was under the impression that the COPE didn't affect the final number?molerat said:It will be her pre 2016 old scheme basic pension with the additional state pension. That amount has, apart from inflationary increases, been the same since April 2016. Does her forecast show a COPE amount ?Does your forecast show a COPE amount ?I suspect the main difference is the contracted out periods.

1 -

COPE was used to establish your starting amount in 2016.

It isn't used again after that.1 -

See

https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/210299/single-tier-valuation-contracting-out.pdf

The "rebate derived amount" is the COPE, used once only to calculate each person's "foundation (starting) amount" at 6/4/16.

The "starting amount" was the higher of

NI years/30 (max) x £119.30 + (Additional State Pension - Deduction for Contracting Out) Old Rules

(NI years/35 (max) x £155.65) - Contracted Out Pension Equivalent. New Rules1 -

molerat said:It will be her pre 2016 old scheme basic pension with the additional state pension. That amount has, apart from inflationary increases, been the same since April 2016. Does her forecast show a COPE amount ?Does your forecast show a COPE amount ?I suspect the main difference is the contracted out periods.

Thanks for info , no cope amount on her account . But mine does include a cope amount of £51-95.

I contracted out in 1988 till 2007 when I went self employed. I thought wife’s higher amount was because she didn’t join her final salary scheme till age 33 . Can she rely on this figure to plan ahead ?0 -

If no COPE amount then, according to her records, she has not been in a contracted out pension scheme so paying full NI in a reasonably paid job and accruing full S2P hence the higher pension amount. You were contracted out not paying full NI so not accruing S2P.

1 -

If no COPE amount then, according to her records, she has not been in a contracted out pension scheme

The OP seems to be intimating that his wife did join her firm's Final Salary Pension Scheme in around 1999 and presumably is still a member.

This Scheme was almost certainly contracted out up to 6/4/16?

Admittedly she wouldn't have a COD related to GMP (this ended 6/4/97) but it would be possible for her to have a "rebate derived amount" (COPE)?

9. For the period to 1997 this is straightforward as there will be a Contracted-out Deduction as per paragraph 6 (1) above. However, we also need to reflect that during the periods 1997-2002 and from 2002 onwards if someone had been contracted out they would be building the private pension equivalent of Additional Pension in the contracted-out scheme. So the Rebate Derived Amount is calculated as follows:

-

Contracted-out Deduction from 1978-97;

-

A new notional deduction in respect of being contracted out between1997

and 2002 - this value will be the amount of SERPS the person would have

had if they had been contracted in;

-

The deduction made from gross S2P in respect of being contracted out from

2002 to 2016.

0 -

-

As you say she joined /allowed into !!!!!! scheme in 1999 (aged 33 but that closed in 2011(deferred member) and is now in a money purchase scheme . In effect by not contracting out she has gained extra state pension ? Thanks for your help.xylophone said:If no COPE amount then, according to her records, she has not been in a contracted out pension schemeThe OP seems to be intimating that his wife did join her firm's Final Salary Pension Scheme in around 1999 and presumably is still a member.

This Scheme was almost certainly contracted out up to 6/4/16?

Admittedly she wouldn't have a COD related to GMP (this ended 6/4/97) but it would be possible for her to have a "rebate derived amount" (COPE)?

9. For the period to 1997 this is straightforward as there will be a Contracted-out Deduction as per paragraph 6 (1) above. However, we also need to reflect that during the periods 1997-2002 and from 2002 onwards if someone had been contracted out they would be building the private pension equivalent of Additional Pension in the contracted-out scheme. So the Rebate Derived Amount is calculated as follows:

-

Contracted-out Deduction from 1978-97;

-

A new notional deduction in respect of being contracted out between1997

and 2002 - this value will be the amount of SERPS the person would have

had if they had been contracted in;

-

The deduction made from gross S2P in respect of being contracted out from

2002 to 2016.

0 -

-

In effect by not contracting out she has gained extra state pension ? Thanks for your help.

She started work in 1988 but was not a member of her employer's pension scheme.

However, she would have been contracted in to the State Earnings Related Pension Scheme so accruing additional state pension over and above the Basic State Pension.

She joined the presumably contracted out FS Scheme in 1999 - by this time the GMP/COD system had ended but in order to remain contracted out (so that lower employer/ee NI contributions were made) the FS Scheme had to meet the Reference Scheme Test explained here

https://techzone.adviserzone.com/anon/public/pensions/Tech-guide-section-92b-rights

In 2002, SERPS (Additional State Pension) was replaced by State Second Pension (S2P) - as explained here,

it was possible for moderate earners to accrue some S2P Additional State Pension even though contracted out.

Therefore between 2002 and 2011 your wife may have been accruing some S2P.

In 2011, the FS Pension Scheme closed (presumably in favour of some sort of DC Scheme) in which case she would probably have been contracted back in to S2P and still accruing ASP.

No more ASP could accrue after April 6 2016.

Thus your wife's NSP starting amount in 2016 would have been the higher of

NI years/30 x £119.30 + (Additional State Pension - a notional COD). Old Rules

(NI years/35 x £155.65) - Contracted Out Pension Equivalent. New Rules

It would seem that at 6/4/16 her starting amount was higher under the old rules and was already more than a full NSP.

Was her FS Scheme contracted out?

Is no COPE shown on her forecast?

Let's take a person aged say 55 at 6/4/16 whose starting amount was say £180.65. He has a full NSP and an additional £30.

Although needing to pay NI up to his SPA, he will not increase his state pension by so doing.

His full NSP will revalue under (at the moment) the Triple Lock

while the £30 (his "protected payment") will revalue by CPI.

At SPA he receives his "starting amount" revalued as above.

1 -

If not in a contracted out scheme then yeas she will have gained additional pension.If she was in a contracted out final salary scheme there should be a COPE amount and also a reduction in her additional pension and so the current pension amount. She needs to check if that company scheme was contracted out because if she was these errors do not usually get picked up until claiming state pension when the whole record is checked which leads to a whole lot of pain.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.7K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards