We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Pension transfer to True potential

Comments

-

eric4395 said:Looking at how RL porfolio 3 and TP cautious has performed over the last 2 years shows RL port 3 having a +1.3% gain over 12 months and +8.0% over 24months

TP cautious has had a+ 3.69 gain over 12 months and 14.0% over 2 . years. So looking at these figures despite higher fees the tp option looks more favourable to me. Can anyone give me reasons as to why they would stay with RL.Here's one: Those performance figures give me no confidence that a favourable difference will persist in favour of TP cautious.'An inverse relationship generally exists between the measurement time horizon and the ability of top-performing funds to maintain their status. It is worth noting that no large-cap, mid-cap, or small-cap funds managed to remain in the top quartile at the end of the fiveyear measurement period. Furthermore, no mid-cap or small-cap funds were able to retain their status as of the end of the fourth period. This figure paints a negative picture regarding long-term persistence in mutual fund returns....Over the five-year measurement horizon, the results show a lack of persistence among nearly all the top-quartile fixed income categories, with a few exceptions.' There's a lot more detail there that is easy to read.'Good past performance seems to be, at best, a weak and unreliable predictor of future good performance over the medium to long term. About half the studies found no correlation at all between good past and good future performance. Where persistence was found, this was more frequently in the shorter-term, (one to two years) than in the longer term.

0 -

While TP continue to incentivise IFAs to move clients to them, then it is fair to conclude that any recommendation for such a move is more likely to be in the interests of the IFA than it is the client.I don't care about your first world problems; I have enough of my own!2

-

While TP continue to incentivise IFAs to move clients to them, then it is fair to conclude that any recommendation for such a move is more likely to be in the interests of the IFA than it is the client.IFA decisions should be without any outside influence. Not only in reality but also in perception.I don't see any numbers that you quoted ie TP 7, all I see is a choice of defensive, cautious or cautious +, balanced or balanced +, growth and aggressive.The numbers reflect versions. Possibly timescale weightings or product versions or variances within the same risk band or used for blending. They may use different ones for different distribution methods (e.g. robo, sales rep or IFA)

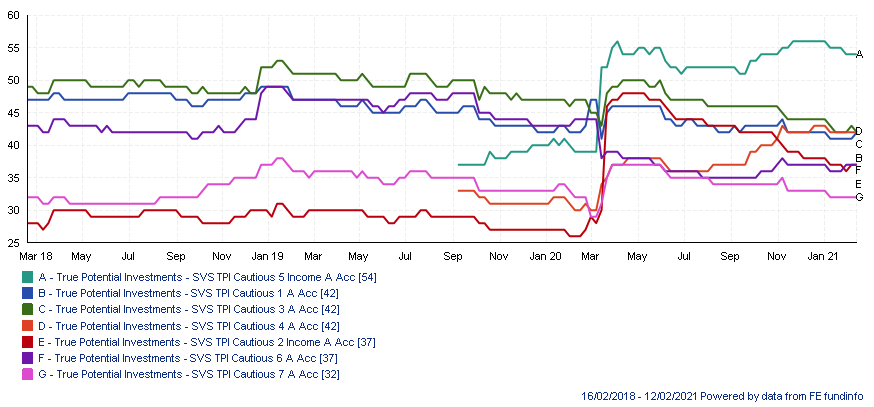

Here is the risk levels of all the TP funds with cautious in the name

On our 1-5 risk scale with a long term outlook, the lower ones fall in risk 1 (cautious). the middle ones in risk 2 (cautious to moderate) and the top one in risk 3 (moderate)

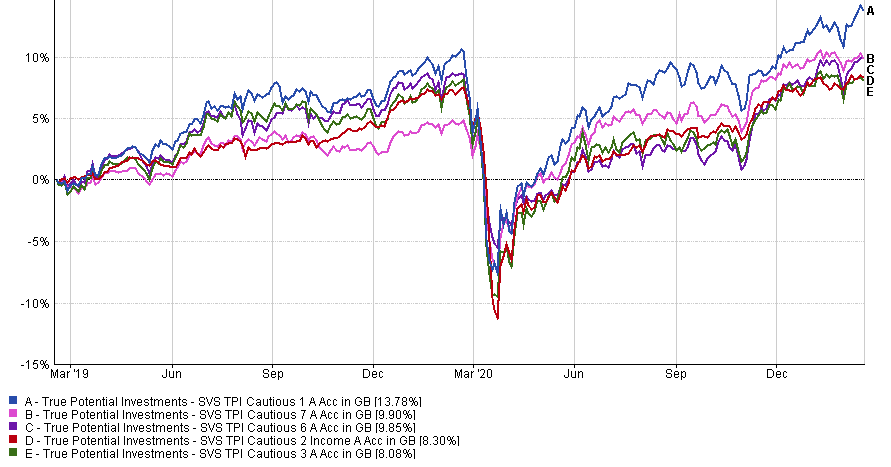

I think we can eliminate 4 & 5 as they have less than 2 years history and you mentioned 24 months returns. So, if we look at the rest you have the following performance over 2 years:

Your mention of 24 months giving 8% would suggest TP Cautious 3. (it was 7.98% using yesterdays figures). Cautious Income 2 is next closest to that but has a clear naming difference.

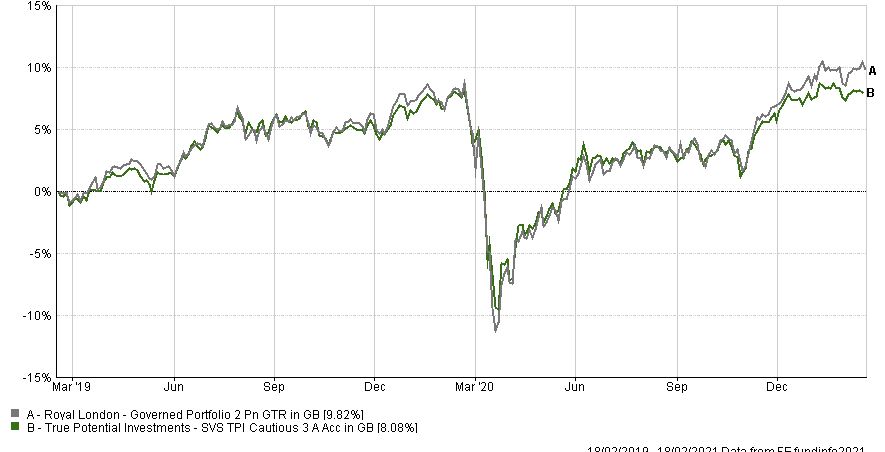

RL GP2 is in the same risk profile as TP cautious 3. So, here is the performance of the two over two years

Virtually identical. And for reference, if I go back to launch of TP cautious 3 in 2014, the lines are almost identical with RL pipping TP at 31.64% vs 29.80%.

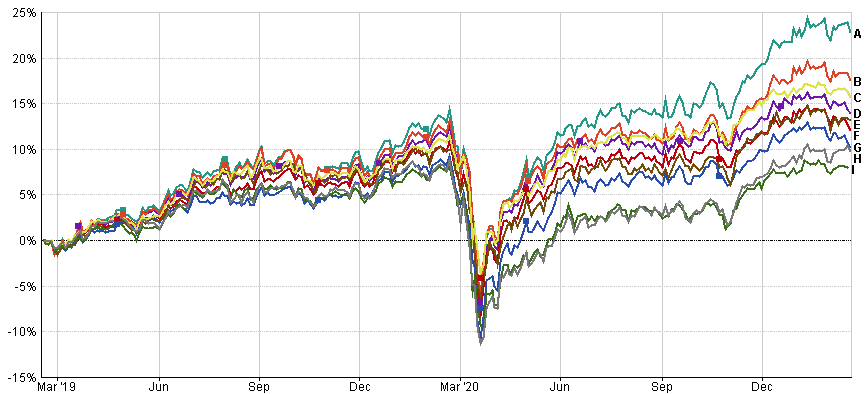

And below is the chart with the same green & grey (I&H) lines showing TP and RL vs a bunch of others with the same risk profile:

I could have filled that chart with loads more but the ones above include a cheapish wealth management option . An expensive wealth management option , a complicated wealth management option. A couple of cheap multi-asset funds, an ESG portfolio and model portfolio of single sector funds.

I have stuck to the 24 month period only because you mentioned it.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

Thanks for taking the time to answer my query dunstonhdunstonh said:While TP continue to incentivise IFAs to move clients to them, then it is fair to conclude that any recommendation for such a move is more likely to be in the interests of the IFA than it is the client.IFA decisions should be without any outside influence. Not only in reality but also in perception.I don't see any numbers that you quoted ie TP 7, all I see is a choice of defensive, cautious or cautious +, balanced or balanced +, growth and aggressive.The numbers reflect versions. Possibly timescale weightings or product versions or variances within the same risk band or used for blending.

Here is the risk levels of all the TP funds with cautious in the name

On our 1-5 risk scale with a long term outlook, the lower ones fall in risk 1 (cautious). the middle ones in risk 2 (cautious to moderate) and the top one in risk 3 (moderate)

I think we can eliminate 4 & 5 as they have less than 2 years history and you mentioned 24 months returns. So, if we look at the rest you have the following performance over 2 years:

Your mention of 24 months giving 8% would suggest TP Cautious 3. (it was 7.98% using yesterdays figures). Cautious Income 2 is next closest to that but has a clear naming difference.

RL GP2 is in the same risk profile as TP cautious 3. So, here is the performance of the two over two years

Virtually identical. And for reference, if I go back to launch of TP cautious 3 in 2014, the lines are almost identical with RL pipping TP at 31.64% vs 29.80%.

And below is the chart with the same green & grey (I&H) lines showing TP and RL vs a bunch of others with the same risk profile:

I could have filled that chart with loads more but the ones above include a cheapish wealth management option . An expensive wealth management option , a complicated wealth management option. A couple of cheap multi-asset funds, an ESG portfolio and model portfolio of single sector funds.

I have stuck to the 24 month period only because you mentioned it.

It would be a straight transfer over to RL governed portfolio 3 from RL1 portfolio with no extra fees involved they would stay as they are 0.4% to RL and 0.5% to my IFA.

As far as if I was interested in a TP portfolio I have to fill out a link provided by my IFA from TP which basically asks you questions to my own personnel risk assessment and then recommends whether you should go into cautious growth etc, after the questions. So in theory I suppose I could end up in the wrong reccomended portfolio if my answers were uncertain. I am not getting a reccomendation from my IFA but if I did it would incur extra fees above the standard 0.5% that he is charging then I would still have my 0.4% platform and 0.8% approx depending on what porfolio I ended up in with TP.

What TP porfolio do you think is off the same approximate risk as RL3, ( I thought cautious) both of are going to be with less % equity funds involved which is higher in the RL portfolio 1 fund I am in at the moment and hopefully a steadier return or loss as the case may be as I move towards retirement. Or do you think I should just stay with RL rather than move to TP as the safer option although I do realise that neither would be your preferred option going by your answer. However I am going to keep my advisor and choose one or the other. Also what is the danger or chance that I am taking if I choose TP surely if the markets are favourable over the next few years then I would be making a reasonable profit the same as any other pension governed fund. ( ps I am 66 year old to give you an idea of the timescale involved its not as if I am retiring early or young)

0 -

As far as if I was interested in a TP portfolio I have to fill out a link provided by my IFA from TP which basically asks you questions to my own personnel risk assessment and then recommends whether you should go into cautious growth etc, after the questions. So in theory I suppose I could end up in the wrong reccomended portfolio if my answers were uncertain.Risk profilers are not reliable enough to be used by themselves by advisers. The adviser has further questioning and context that needs to be carried out as well as looking at conflicting answers. The Q&A on the risk profilers is the basis for a conversation that leads to the risk profile being selected.What TP porfolio do you think is off the same approximate risk as RL3, ( I thought cautious) both of are going to be with less % equity funds involvedRL GP3 has the same risk band as TP Defensive (all numbers as whilst there are differences, they fall within the same band). Performance varies:

It is worth noting that RL's returns assume a 1% AMC. They do not take into account the discount or the mutual bonus you get each year. TP does not include the platform charge.Or do you think I should just stay with RL rather than move to TP as the safer option although I do realise that neither would be your preferred option going by your answer.I cannot answer that as I cannot be seen to give advice as the FCA treat forum posts the same as any other medium. However, you are right that neither would be my preferred option. I will say that when an adviser is looking at an existing plan and considering moving it, there should be something that clearly makes the new plan "better" or more suitable than the existing one. RL being the existing one has lower charges and better returns on comparable cautious investing and not dissimilar returns on defensive investing. For me personally, I am not seeing the better/more suitable benchmark being met.I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1

It is worth noting that RL's returns assume a 1% AMC. They do not take into account the discount or the mutual bonus you get each year. TP does not include the platform charge.Or do you think I should just stay with RL rather than move to TP as the safer option although I do realise that neither would be your preferred option going by your answer.I cannot answer that as I cannot be seen to give advice as the FCA treat forum posts the same as any other medium. However, you are right that neither would be my preferred option. I will say that when an adviser is looking at an existing plan and considering moving it, there should be something that clearly makes the new plan "better" or more suitable than the existing one. RL being the existing one has lower charges and better returns on comparable cautious investing and not dissimilar returns on defensive investing. For me personally, I am not seeing the better/more suitable benchmark being met.I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.8K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards