We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

DB Pension lump sum

Daverok

Posts: 8 Forumite

I know this has been written many times before and yes, I have looked at previous posts but I am still not sure.

I am due to draw a DB pension worth £16009 per year and £49292 lump sum...OR.....£13749 per year and £91663 lump sum, both index linked.

I am married but the widow's pension is the same on both choices. I have no immediate need for a larger lump sum and consider myself to be in good health.

If I were to take the larger lump sum and invest it, what growth do you guess it would need to keep up with inflation?

I am due to draw a DB pension worth £16009 per year and £49292 lump sum...OR.....£13749 per year and £91663 lump sum, both index linked.

I am married but the widow's pension is the same on both choices. I have no immediate need for a larger lump sum and consider myself to be in good health.

If I were to take the larger lump sum and invest it, what growth do you guess it would need to keep up with inflation?

0

Comments

-

I assume the monthly payment increases every year? Making the higher monthly payment (lower lump sum) even more attractive.

My suggestion would be to take the lower lump sum. As you say you don’t need the money so you might as well convert it to a better income. Why invest when you don’t need to?0 -

I am investing elsewhere with other funds. I was curious at what rate would I need to achieve to keep up with, and hopefully gain using the extra £420000

-

The typical predicted outlook for a medium risk investment portfolio over the next 10 years is 2% above inflation .

But note the word PREDICTED .0 -

If I were to take the larger lump sum and invest it, what growth do you guess it would need to keep up with inflation?

The BofE is targeted at inflation of 2%.

If you were using this rate to assist in the comparison between the offers it would just wash out though as the 2% increase in invested money would be the same return as the 2% increase in the annual pension.

Albermale's projected number may be more helpful than "what will the inflation rate be".

0 -

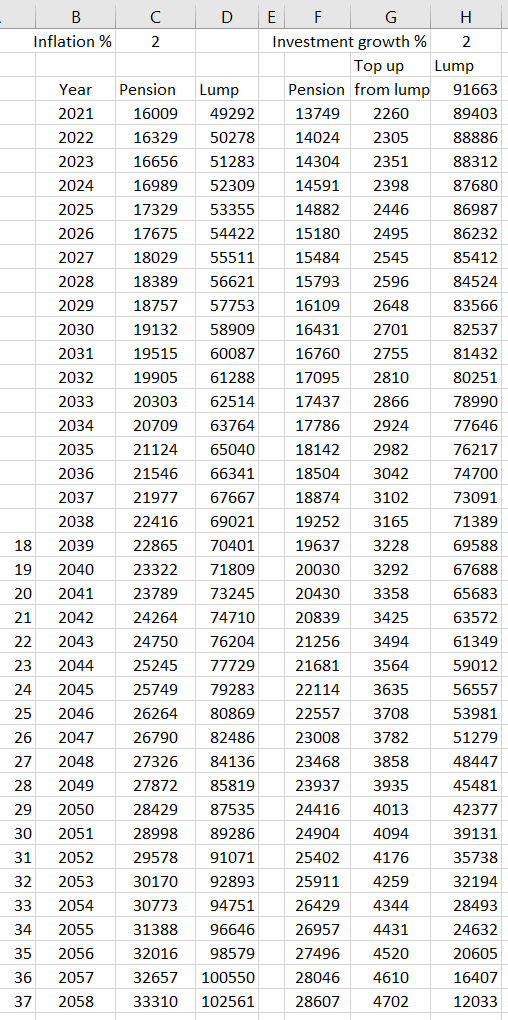

I knocked up a quick spreadsheet which might help you with your thinking. I have assumed 2% inflation every year.

Look at columns C and D. That's your larger pension, smaller lump, growing each year by 2%.Column F is the smaller pension and H is the larger pot. Each year I have taken enough out of the pot to top up the pension to equal the larger pension in column C. In this illustration, the pot (in either case) grows at 2%, just keeping pace with inflation. The bigger pot is ahead for the first 18 years - equal pension, larger pot. After Year 18, the pot is now smaller than it would have been if you took the small lump sum. Obviously the difference gets much bigger if you live to old age.0

Look at columns C and D. That's your larger pension, smaller lump, growing each year by 2%.Column F is the smaller pension and H is the larger pot. Each year I have taken enough out of the pot to top up the pension to equal the larger pension in column C. In this illustration, the pot (in either case) grows at 2%, just keeping pace with inflation. The bigger pot is ahead for the first 18 years - equal pension, larger pot. After Year 18, the pot is now smaller than it would have been if you took the small lump sum. Obviously the difference gets much bigger if you live to old age.0 -

2% growth is not much for a long term investment. If you were able to achieve 4% or 5% growth by investing the lump sum, you could stay ahead for several years more

At 4% growth, the larger lump sum is ahead until year 23. At 5% it wins up to year 31If you have a particular what-if? you would like to run, let me know1

At 4% growth, the larger lump sum is ahead until year 23. At 5% it wins up to year 31If you have a particular what-if? you would like to run, let me know1 -

Wow, thanks for all your help folks. IF inflation is 2% AND growth is 4% things would look rosy. That would take me to 80 and also leave money if I popped my cloggs inbetween.

OR equally I could just hope to live until I am 80, not worry about rampant inflation, poor investment growth, and then be in profit forever afterwards. Have I read this right?0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards