We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Whats considered a "good" employer pension? Me 5% employer 3%?

Comments

-

It's a great pension if it's a state sector school. If it's an independent school they might not use the TPS so you need to read the contract.robatwork said:

Sorry to jump in but I have a related query. A new teacher starting this year - what is the "finger in the air" figure for what their pension is worth similar to the NHS's 30%?dunstonh said:Overall, the NHS pension would cost around 30% of your salary to replicate. i.e. you would need to up that 5%+3% to around 30% to get a similar end pension. Plus, arrange a life assurance policy to replace the death in service. The NHS pension is not as good as it was but it is still in the gold standard category.

You may be able to transfer benefits from other pensions into the TPS, but if so, expect a time limit for allowing this.. Ask your union rep.There is no honour to be had in not knowing a thing that can be known - Danny Baker0 -

Minimum auto enrolment contributions here with nothing on the first £6k odd of salary. I don't mind too much as it is a charity so they do need to keep staff costs as small as possible. However I resent that they refuse to use salary sacrifice.0

-

They could save money by sacking their finance manager and replacing them with one that understands taxation and the obligation to act in the best interest of the charity's donors and donees. Not using salary sacrifice means they pay more in staff costs. They're negligent.WillowCat said:need to keep staff costs as small as possible.

they refuse to use salary sacrifice.

"Real knowledge is to know the extent of one's ignorance" - Confucius1 -

kinger101 said:They could save money by sacking their finance manager and replacing them with one that understands taxation and the obligation to act in the best interest of the charity's donors and donees. Not using salary sacrifice means they pay more in staff costs. They're negligent.Wildly overstating it. Salary sacrifice is more complicated to set up than a standard net pay arrangement, and the cost may not be worth the benefits in staff retention. Being a charity, most of their staff might be on minimum wage or close to it, and unable to use salary sacrifice to any great extent.Salary sacrifice may have unintended consequences (e.g. for mortgage affordability or income protection insurance) so everyone who pays into a pension in this way needs to be fully aware of them. It is more likely to be of benefit to relatively high earners, if the charity has any (as they're more likely to value it and less likely to be caught by unintended consequences) and by virtue of their high-earning status, the onus is on them to demand the salary sacrifice option as much as it is on the charity to offer it.3

-

My wife is the director responsible for HR / Payroll at a charity. The price from their payroll supplier to implement and run SS was greater than the potential NI saving.Malthusian said:kinger101 said:They could save money by sacking their finance manager and replacing them with one that understands taxation and the obligation to act in the best interest of the charity's donors and donees. Not using salary sacrifice means they pay more in staff costs. They're negligent.Wildly overstating it. Salary sacrifice is more complicated to set up than a standard net pay arrangement, and the cost may not be worth the benefits in staff retention. Being a charity, most of their staff might be on minimum wage or close to it, and unable to use salary sacrifice to any great extent.Salary sacrifice may have unintended consequences (e.g. for mortgage affordability or income protection insurance) so everyone who pays into a pension in this way needs to be fully aware of them. It is more likely to be of benefit to relatively high earners, if the charity has any (as they're more likely to value it and less likely to be caught by unintended consequences) and by virtue of their high-earning status, the onus is on them to demand the salary sacrifice option as much as it is on the charity to offer it.

Apparently it has also added to the furlough calculations nightmare at places that are using it, and is likely to cost those organisations money as only the standard Auto Enrolment 3% can be reclaimed from HMRC.2 -

Which "part" of the NHS scheme are you in?[Deleted User] said:Considering new job and its 5% me and 3% from employer. Is this considered good?

Also, and I know the NHS pension is way different - I contribute 9.6% to that at the moment in current job. How does this compare?

Also, if I did leave would my NHS pension be frozen?

(I know NHS WAS very good but they've chipped away at it over the years)0 -

I was wondering that too when people were saying they're paying 40 and 50% of their wages into their pension pot! At the end of the day your pension is a % of your wage, so if your wage is pretty low then pension's going to be low. Similarly when NHS staff got a 2% pay rise and people were singing and dancing in the streets.JustAnotherSaver said:Strange this. Wonder if most people on here are actually in decent paid jobs. Maybe. Maybe not.

I suspect most that come here have an interest in I vestments, saving, DIY money managing etc and maybe these people are generally not the bottom-line kind of people. Again, just wonderings, I could be wrong.

My workplace pension is bare minimum. They'd pay me zero if they could get away with it. Those I know are also paid the bare minimum. In fact I only know of 1 person really who is anything above minimum, the rest are minimum.

My social circle does not really involve people earning 30k, 40k, 50k etc. We are generally minimum wage earners or maybe slightly above but not much. Coincidence that our pensions are as little as possible? Maybe, maybe not.0 -

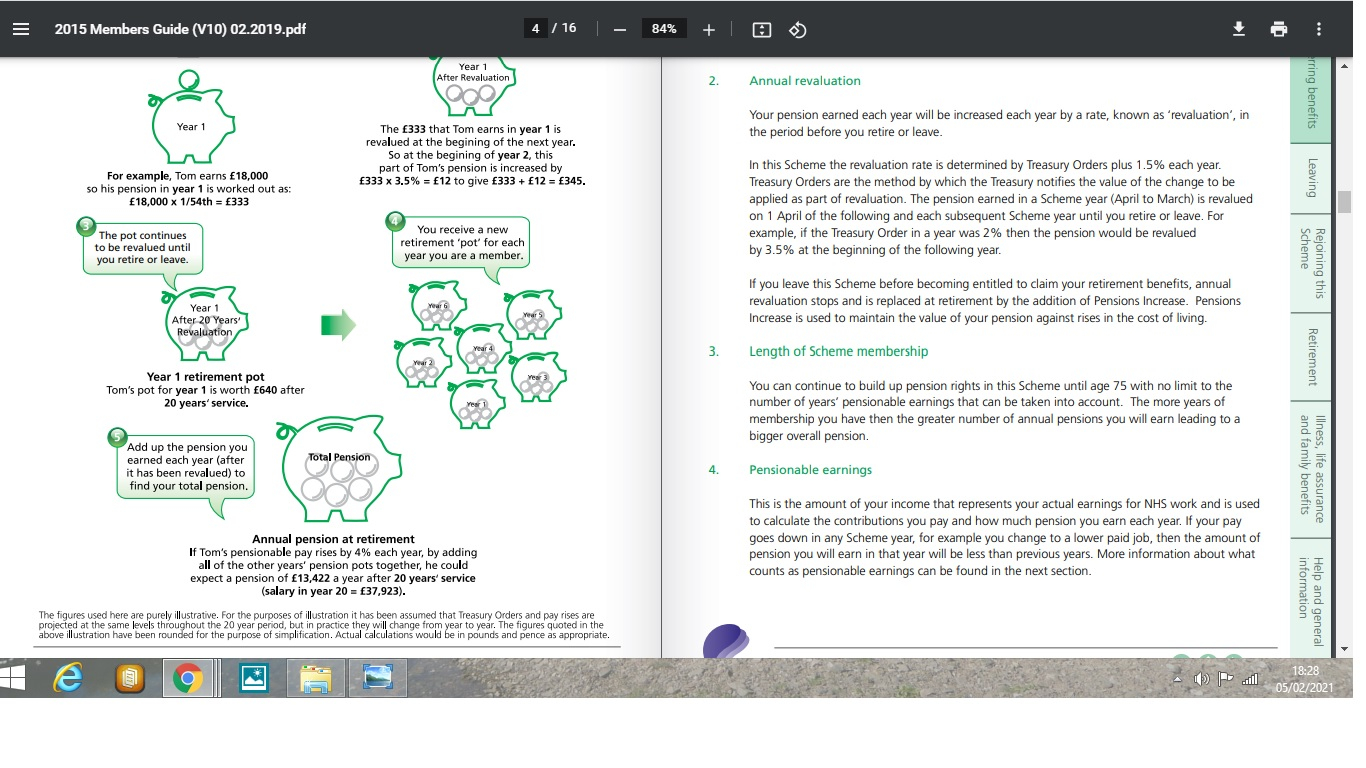

Just had a look at the 2015 NHS scheme and this infographic

Are they suggesting that Toms NHS salary will increase by 100% over 20 yrs? 0

0 -

whatsthenews said:Just had a look at the 2015 NHS scheme and this infographic

Are they suggesting that Toms NHS salary will increase by 100% over 20 yrs?They appear to be showing a hypothetical example in which salary escalates at 4% p/a over a 20 year period. Mathematically, that means the salary at the end of the period will be more than double the initial salary.Realistically, the increases will not be the same every year, with a mixture of bad years with very low pay award, average years of pay awards slightly above inflation and some very good years (promotions), but averaging out at 4% p/a seems a pretty normal example.0 -

The 2 % was the increase in the pay bands. Long overdue considering years of below-inflation increases. Many NHS staff are on a career path where they move up the banding system. A foundation year junior doctor would expect a much more rapid progression than that.whatsthenews said:Just had a look at the 2015 NHS scheme and this infographic

Are they suggesting that Toms NHS salary will increase by 100% over 20 yrs?"Real knowledge is to know the extent of one's ignorance" - Confucius0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards