We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

How to complain about poor DB lump sum commutation factor / inequality?

Comments

-

itsmeagain said:You may be right, but there's no mention of the HMRC rules causing the inequality here.... https://www.jameshambro.com/insight/comment/tax-free-lump-sum/You seem quite taken by this blog post, published on its own website by a company looking to sell its services that include managing transferred out formally DB pensions...The HMRC limit (or rather one of them) is 25% of the individual's remaining lifetime allowance (this goes for a PCLS taken from both DC and DB schemes). The lifetime allowance for a DB pension is 20 times the annual pension, plus any lump sum taken. So for someone with a big DB pension, a poor commutation rate is not necessarily a bad thing as it enables tax free cash while undercutting would would be an LTA charge at the same time (e.g. a retiring local authority chief exec - 12/1 in itself is rubbish, but using it means the total pension + lump sum gets valued less for LTA purposes).

1 -

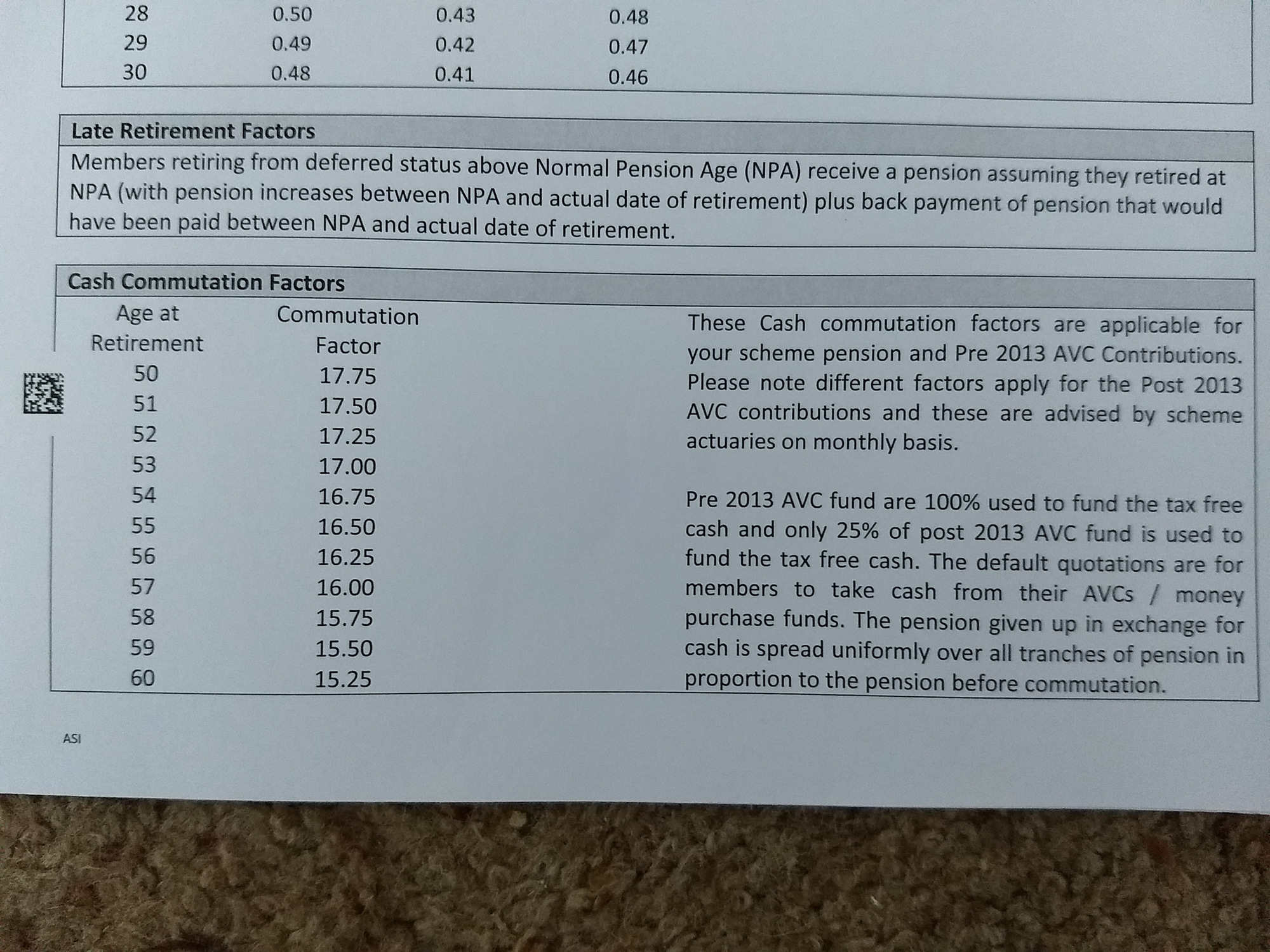

Earlier I said that my factor was 13 but I was wrong. The actual figure is 16.5 and the lump sum offered is £132k in exchange for £8kPA reduction in my pension. 16.5 x £8k = £132k. Secret table attached!Silvertabby said:Apples and oranges. The HMRC 25% maximum tax free cash in respect of DB schemes is calculated thus:20 x annual pension plus 1 x any automatic lump sum x 25% (before applying the commutation factor).However, this doesn't tally with the figure you quoted - a pension of £27,809. Is there any automatic (pre commutation) lump sum? If so, what is it?

1 -

itsmeagain said:

Earlier I said that my factor was 13 but I was wrong. The actual figure is 16.5 and the lump sum offered is £132k in exchange for £8kPA reduction in my pension. 16.5 x £8k = £132k. Secret table attached!Silvertabby said:Apples and oranges. The HMRC 25% maximum tax free cash in respect of DB schemes is calculated thus:20 x annual pension plus 1 x any automatic lump sum x 25% (before applying the commutation factor).However, this doesn't tally with the figure you quoted - a pension of £27,809. Is there any automatic (pre commutation) lump sum? If so, what is it?16.5 is better than 13 - but's it's still not good if you take your benefits from 55 and then live to 90.Option 1Pension of £27,809, no lump sum.35 x £27,809 = £973,315 (Plus 35 years of index linking starting from £27,809)Option 2Pension of £19.899 plus lump sum of £132K35 x £19,899 plus 1 x £132,00 = £848,465 (plus 35 years of index linking starting from £19,899)

1 -

Your point about the spouse pension when I die is very good. It's the same figure whichever option I take so that liability is the same in both cases.Brynsam said:

See Silvertabby's answer, but also note they aren't getting rid of 1/4 of their liability. For example, any spouse's pension is normally based on the pre-commutation pension (i.e. as if you'd taken no tax free cash at all), so they'd still be on the hook for that, whether or not you take a tax free lump sum. Add on the fact that they still have the 'uncertainty factor' of keeping any part of your benefits in the scheme, and the not-very-understandable starts to make a bit more sense - but as already said, commutation is often not 'good value' for members.itsmeagain said:

Thanks Brynsam. This maybe over simplified, but if they are prepared to pay me £1m to get rid of 4/4 of their liability (full transfer), then why aren't they prepared to pay close to £0.25m to get rid of 1/4 of their liability (lump sum)?Brynsam said:Commutation factors are notoriously poor value in many schemes - something which has come under the spotlight when people nearing their scheme's Normal Retirement Age compare a transfer value with the tax free lump sum if they commute part of their pension. Some schemes have been addressing this disparity by improving commutation factors, others have taken the view that members don't have to commute if they don't want to and intend to take no action. You're asking a very sensible question.

If you transfer out with a £1m transfer and then immediately take a lump sum, it could indeed be £250K. If you then tried to buy a comparable annuity (i.e. a pension on the same terms as the index-linked benefits offered by your DB scheme), you won't get anything like the same level of pension. (Yes, I know you could go into drawdown, but I'm trying to give you a simple way to understand the apparent anomaly.)0 -

I agree but there are also taxation differences between the 2 options, although I still think option 1 is better, hence why I say that the lump sum option appears poor value.Silvertabby said:16.5 is better than 13 - but's it's still not good if you take your benefits from 55 and then live to 90.Option 1Pension of £27,809, no lump sum.35 x £27,809 = £973,315 (Plus 35 years of index linking starting from £27,809)Option 2Pension of £19.899 plus lump sum of £132K35 x £19,899 plus 1 x £132,00 = £848,465 (plus 35 years of index linking starting from £19,899)0 -

Just because you CAN do something, doesnt meant you Should do something. The devil is in the detail.itsmeagain said:

Not sure if we're on the same subject here. Ever since I joined the scheme, the members have been able to take a lump sum. This is a copy/paste of the relevant section in my company DB pension guide...NottinghamKnight said:The answer is to take the pension when it makes sense for you to do so according to your personal circumstances. Your employment contract states they will pay a set amount per year, you were never promised a lump sum and if the offer they have provided is poor then don't take it. This is all a consequence of the wider financial landscape, transfers out from db schemes (db pensions are of course rare as hens teeth now in the private sector) would rarely have been considered until a few years ago.TAKING A TAX-FREE CASH SUMYou will have the option to give up some of your pensionin exchange for a one-off lump sum that is not taxable.You can take up to a quarter of the value of your pensionas a tax-free cash sum, but you can decide to take lessthan that or none at all. If you’ve paid AVCs, this mayaffect the amount of tax-free cash you take. Click herefor more information.THINKING ABOUT RETIREMENTThis section has some information about yourretirement options and how your benefits are paid.You will receive all the information you need wellbefore you are due to retire.You will have the chance to choose the amount of tax-free cash sum you want to take,when you retire. If you take a tax-free cash sum, your monthly pension will be lower,depending on how much cash you decide to take and how old you are when you retire.

The commutation rate as said by someone abve says it is a good deal. I havent checked the figures myself, but that is your job. Things to help are, what other savings and investments do you have outside of pensions? What does your spouse/partner have? What debts do you have?

In general, if you have cash savings for emergencies and some investments outside of you DB pension it may make sense to not take any TFLS.0 -

I think that's a typo - NOT a good deal!atush said:

The commutation rate as said by someone abve says it is a good deal. I havent checked the figures myself, but that is your job. Things to help are, what other savings and investments do you have outside of pensions? What does your spouse/partner have? What debts do you have?0 -

Thanks Brynsam. I think that the convo had diverged a little off topic anyway - I was wanting to know if there was anyone policing the management of DB schemes that I could complain to wrt poor commutation factors, bearing in mind that they have recently been advised to improve ERF's so that members are treated fairly, independent of how they take their pension?0

-

No, though you can contact the trustees but their interest will be opposite to that which you imply. Commutation factors are defined by the scheme and just need to be clear and justifiable. The recent near zero interest rate policy has had an impact on transfer values which has turned people's heads, historic factors of high teens or low twenties now look poor. The scheme has a duty to be sustainable to all members and comply with their stated aims which is to pay an agreed amount at a set age.itsmeagain said:Thanks Brynsam. I think that the convo had diverged a little off topic anyway - I was wanting to know if there was anyone policing the management of DB schemes that I could complain to wrt poor commutation factors, bearing in mind that they have recently been advised to improve ERF's so that members are treated fairly, independent of how they take their pension?1 -

The table below shows memberships of the largest 4 public service pension schemes, as well as memberships of schemes covered by the Purple Book - these are private sector DB schemes.

The 4 largest public sector schemes have a combined membership of 12.7 million. These members all have commutation rates of 12:1.So you should be very happy with your commutation rate - it is well above average

The 4 largest public sector schemes have a combined membership of 12.7 million. These members all have commutation rates of 12:1.So you should be very happy with your commutation rate - it is well above average") 2

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards