We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Retirement Planner - Importance of Inflation?

Comments

-

1) If you work entirely in 2020 £s when you compare the outcome with the plan in say 10 years time the expense figures wont be meaningful at all to you. You will be thinking in 2030 £s. I dont see you thinking in old £s makes tracking easier. After all your expenditure now is in always in todays £s.snookered1 said:Why add inflation into your projection at all?, it just makes the numbers look big and impressive, and you may end up kidding yourself as to how well you are doing, as the numbers may look great, but what will be the price of a pint of milk in 10 years ?") and general living costs.

and general living costs.

In my opinion it confuses you as to if you really are on track, as you know what life costs you in todays money and for me that's the easiest and best way of working out if I'm on track.

What I do is take my assumed headline investment growth for example say 6% with investments (I'm always conservative), and subtract an assumed inflation rate from it e.g. 2.5%, (-1% for cash in the bank) so your pound invested in todays money is showing a projected real growth above inflation of for example 3.5% but the cash in the bank is actually shrinking, I plumb that into my spreadsheet and use as a reference annual fund real growth and compound this growth in my projections over a number of years, and tweak the "todays" amounts monthly.

2) you say you will plan for an inflation rate of 2.5%, subtracting that figure from your gross returns. What happens in a years time when the returns above inflation havent been 2.5% and you want to review progress? WIll you recalculate what the returns above inflation were assuming the actual inflation rate?

3) When looking at historical data for a new investment you will find it very difficult to compare your desired return above inflation with the data available.

In my view, if you are using the plan as the basis for ongoing financial management 9it is much easier to work in actual £s0 -

Me too. I am using 3% per year after costs as that's in line with my investment strategy. I also can flex the assumptions to model different potential scenarios.GSP said:

3% a year.AlanP_2 said:OK, so what are you forecasting for that over an extended period?

I am modelling cash flow so see no point in modelling growth after inflation for my investments.1 -

I chose 3% growth as being reasonable without trying to be too extravagant. I see some growth figures and think they are just too cautious. No harm being cautious, but I would prefer to spend the money if it was there.OldMusicGuy said:

Me too. I am using 3% per year after costs as that's in line with my investment strategy. I also can flex the assumptions to model different potential scenarios.GSP said:

3% a year.AlanP_2 said:OK, so what are you forecasting for that over an extended period?

I am modelling cash flow so see no point in modelling growth after inflation for my investments.

Inflation is just a small part of spending that can be reviewed every five years or so.0 -

Just wondering, is there a chance you could even be complicating things?snookered1 said:Why add inflation into your projection at all?, it just makes the numbers look big and impressive, and you may end up kidding yourself as to how well you are doing, as the numbers may look great, but what will be the price of a pint of milk in 10 years ? and general living costs.

In my opinion it confuses you as to if you really are on track, as you know what life costs you in todays money and for me that's the easiest and best way of working out if I'm on track.

What I do is take my assumed headline investment growth for example say 6% with investments (I'm always conservative), and subtract an assumed inflation rate from it e.g. 2.5%, (-1% for cash in the bank) so your pound invested in todays money is showing a projected real growth above inflation of for example 3.5% but the cash in the bank is actually shrinking, I plumb that into my spreadsheet and use as a reference annual fund real growth and compound this growth in my projections over a number of years, and tweak the "todays" amounts monthly.

0 -

Some of my largest investments because I let the horses run when they are doing well, are in the Baillie Gifford funds and investment trusts, e.g. Scottish mortgage, Pacific Horizon, Managed fund, American fund etc over the last circa 5-10 years all have done very well and consistently far exceeded my expectations, the dud's have shrunk or been disposed of, also if you look at the average S&P return you'll see its headline return is 10% before costs and inflation are factored in, the FTSE 100 has a headline of about 8%, even the funds invested through my works pension (which by nature of it being a works pension will never be adventurous), are averaging 8%, so yes I think my 6% is conservative, before costs and inflation are factored in hence projecting as 3.5% growth, I work on this because whilst my investments done very well in recent years , there will be times where the market or the funds/investment trusts themselves don't perform.eskbanker said:

What are you invested in if you consider 6% investment growth to be conservative?snookered1 said:What I do is take my assumed headline investment growth for example say 6% with investments (I'm always conservative)....

0 -

Linton,Linton said:

1) If you work entirely in 2020 £s when you compare the outcome with the plan in say 10 years time the expense figures wont be meaningful at all to you. You will be thinking in 2030 £s. I dont see you thinking in old £s makes tracking easier. After all your expenditure now is in always in todays £s.snookered1 said:Why add inflation into your projection at all?, it just makes the numbers look big and impressive, and you may end up kidding yourself as to how well you are doing, as the numbers may look great, but what will be the price of a pint of milk in 10 years ? and general living costs.

In my opinion it confuses you as to if you really are on track, as you know what life costs you in todays money and for me that's the easiest and best way of working out if I'm on track.

What I do is take my assumed headline investment growth for example say 6% with investments (I'm always conservative), and subtract an assumed inflation rate from it e.g. 2.5%, (-1% for cash in the bank) so your pound invested in todays money is showing a projected real growth above inflation of for example 3.5% but the cash in the bank is actually shrinking, I plumb that into my spreadsheet and use as a reference annual fund real growth and compound this growth in my projections over a number of years, and tweak the "todays" amounts monthly.

2) you say you will plan for an inflation rate of 2.5%, subtracting that figure from your gross returns. What happens in a years time when the returns above inflation havent been 2.5% and you want to review progress? WIll you recalculate what the returns above inflation were assuming the actual inflation rate?

3) When looking at historical data for a new investment you will find it very difficult to compare your desired return above inflation with the data available.

In my view, if you are using the plan as the basis for ongoing financial management 9it is much easier to work in actual £s

1, My spreadsheet is to help me project if I'll have and attain my desired standard of living factoring in growth in now x years when I retire, it takes into account my current finances, plus projected payments into my works pension, SIPP and ISA , plus my current expenses, the key thing is that I update the spreadsheet with todays real valuations on a monthly basis, so if I get a pay rise and my works pension goes up, or a bill goes up its entered, so its not a static sheet, more a dynamic projection that looks at todays reality, and assumes modest growth for the future from that point, without inflation factored in I archive past data points annually for reference, so in dec I spend 5 mins entering the state of my finances, and any bills that have gone up/down and the spreadsheet projects the future.

2, then I'll be up or down, like all projections its a projection, the key bit is the investment return over inflation not the inflation or return. e.g 10% inflation and13.5% return is just the same for the future as 2.5% inflation and 6% return they both give you a real growth of 3.5%

3, I dont need to.0 -

Fair enough - I'm not proposing to get bogged down in a numbers game and it's obviously your prerogative to use a figure you're happy with, but over the last ten years, most of which have been a sustained bull run, the FTSE 100 (with dividends reinvested) has averaged 3.9%, although the S&P 500 has undoubtedly been a better index to track over that timeframe. Are you basing your expectations on averaged historical performance over a certain number of years or something more scientific?snookered1 said:

Some of my largest investments because I let the horses run when they are doing well, are in the Baillie Gifford funds and investment trusts, e.g. Scottish mortgage, Pacific Horizon, Managed fund, American fund etc over the last circa 5-10 years all have done very well and consistently far exceeded my expectations, the dud's have shrunk or been disposed of, also if you look at the average S&P return you'll see its headline return is 10% before costs and inflation are factored in, the FTSE 100 has a headline of about 8%, even the funds invested through my works pension (which by nature of it being a works pension will never be adventurous), are averaging 8%, so yes I think my 6% is conservative, before costs and inflation are factored in hence projecting as 3.5% growth, I work on this because whilst my investments done very well in recent years , there will be times where the market or the funds/investment trusts themselves don't perform.eskbanker said:

What are you invested in if you consider 6% investment growth to be conservative?snookered1 said:What I do is take my assumed headline investment growth for example say 6% with investments (I'm always conservative)....0 -

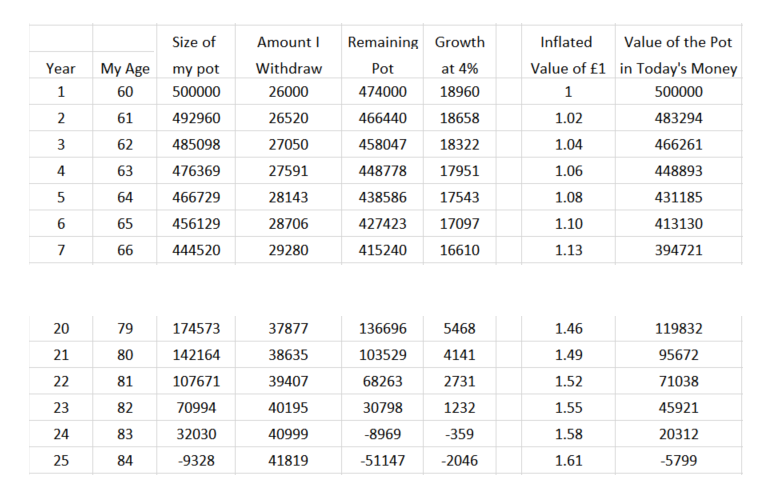

I reckon this is as easy as I can make it. Mythical portfolio 1/2 million, withdrawing 26k per year, growing 2% per year with inflation. Pot growing at 4%.

This would be a pretty bad plan as it runs out of money at age 83, but it should illustrate how simply we can calculate what actually might happen

This would be a pretty bad plan as it runs out of money at age 83, but it should illustrate how simply we can calculate what actually might happen

1 -

Adding just a little complexity, we can keep track of infaltion, and produce a value of the pot for those who want to visualise it in today's terms.

0

0 -

Finally, I've added in a pension. 10k per year, from age 67, growing at 2.5%. It would be easy to add multiple columns for several different pensions, paid at different ages or growth rates.

Things now work out much better for our friend. With just the aid of a state pension, his pot now lasts until he is 96 years old.1

Things now work out much better for our friend. With just the aid of a state pension, his pot now lasts until he is 96 years old.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.9K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards